Morning Ferrous Markets

Market Overview

The global steel and iron ore markets are currently shaped by a mix of economic policies, supply-demand balances, and geopolitical influences. This summary examines the recent trends in the Singapore iron ore market, driven by China's economic measures and strong demand; the Turkish steel scrap market, characterized by stable prices amidst cautious buying; and the US HRC market, where futures prices reflect mixed sentiments with cautious optimism in the near term and bearish positions among managed money participants. Each of these markets provides a unique perspective on the broader steel and iron ore industry dynamics.

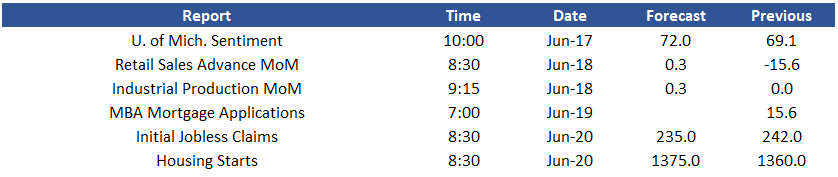

Upcoming Data Releases

![]()

![]()

![]()

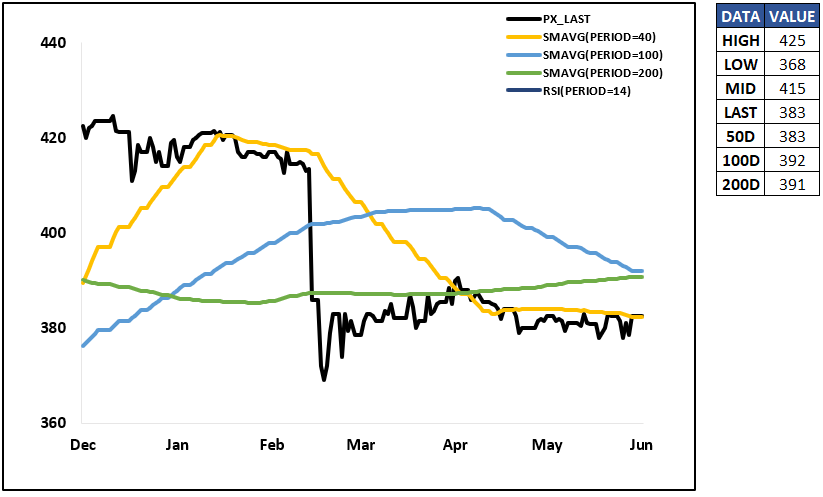

North American (US) HRC Steel Market

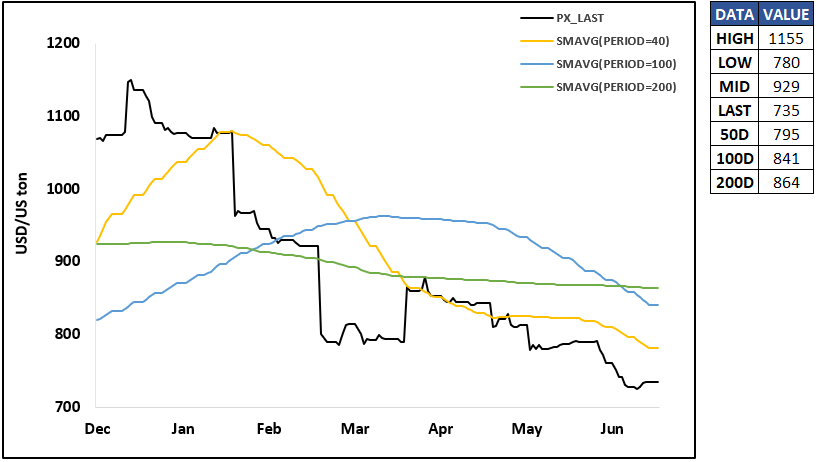

The US Hot-Rolled Coil (HRC) market has experienced significant price fluctuations. Recent prices ranged from $717.00 in July 2024 to $865.00 in April and May 2025. Notably, March 2025 contracts rose by 1.18% to $855.00 per ton, marking today's most significant increase. However, managed long positions in US HRC have decreased considerably, indicating bearish sentiment among traders, with a net managed position of -4,067 contracts as of June 11, 2024. Despite these fluctuations, overall open interest (OI) has increased from the previous week, suggesting growing market participation. This rise in OI indicates that while traders remain cautious, there is still substantial interest and potential for volatility in the market. The data suggests that although the market faces downward pressure, there are signs of resilience and potential recovery depending on broader economic factors and demand trends.

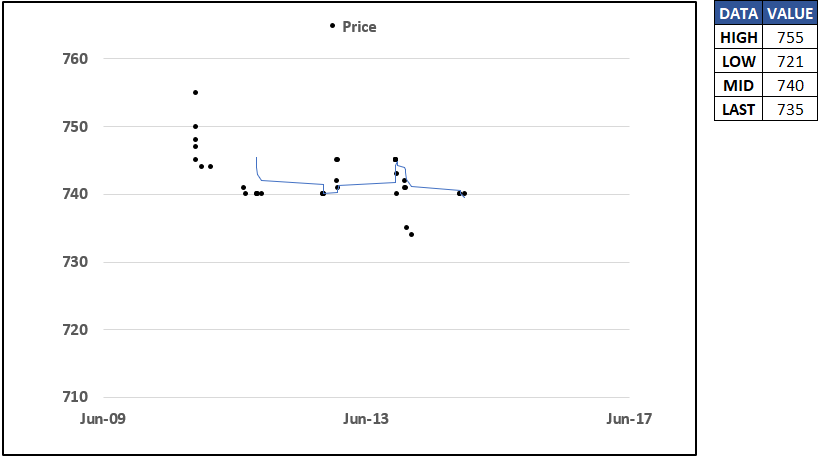

HRC Front Month 3 Day Trend

StoneX & Bloomberg

HRC Front Month 6 Month Price Trend

StoneX & Bloomberg

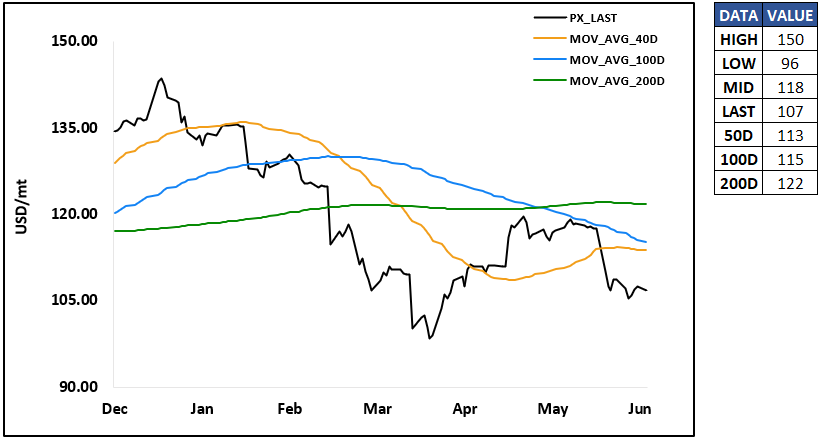

Chinese Steel & Iron Ore Markets

Chinese iron ore futures have been supported by better steel demand and high production levels. On June 14, iron ore futures on the Dalian Commodity Exchange (DCE) rose by RMB 10.5/t ($1.5/t). The China Iron and Steel Association (CISA) reported that daily crude steel output of its member mills reached a one-year high of 2.25 million tons in early June, a 3.3% increase from late May. Despite higher inventories, production increased as margins improved due to lower raw material prices. The BF average capacity utilization rate at 247 steel mills rose to 89.53%, a seven-month high, contributing to higher pig iron output. Nevertheless, net non-commercial positions in Chinese iron ore futures decreased to -4,948 contracts, reflecting a bearish outlook despite recent price support from improved demand and production. This highlights the complexities and challenges within the Chinese iron ore market, where production and demand dynamics are closely interlinked, and market sentiment remains cautious amid fluctuating economic conditions.

SGX Iron Ore CFR China (62%) Futures

StoneX & Bloomberg

European Steel and Steel Scrap Markets

The Turkish steel scrap market has exhibited mixed performance recently. Turkish scrap prices varied, with figures such as $382.50 in June 2024 and $395.00 for February 2025 contracts, which saw the largest price increase of 2.33%. Conversely, busheling scrap experienced notable price drops, with September 2024 contracts falling by 2.3% to $415.00 per ton. Net commercial positions for Turkish steel scrap remain relatively stable at 4,982 contracts. However, the market sentiment remains cautious due to variable demand and inventory levels. Additionally, Turkish rebar prices have shown increases, with prices such as $577.50 in June 2024 and $602.00 in January 2025. Despite the mixed performance, the Turkish steel scrap market continues to navigate through fluctuating demand and economic uncertainties, reflecting the broader challenges faced by the EU Turkish steel scrap sector amid changing market conditions and production dynamics.

Turkish Scrap 1st Month Futures

StoneX & Bloomberg

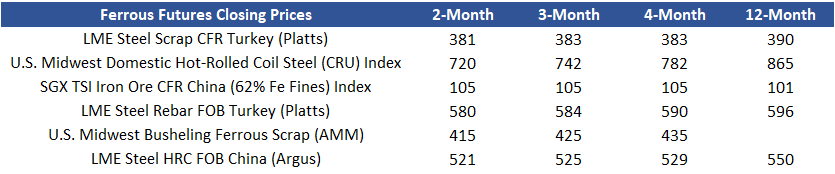

Current Prices