Nasdaq and S&P 500 Lead Risk Swoon but Bull Trend Intact Without a Tangible Thematic Threat

By: John Kicklighter, Head of Market Research

There was a distinct ‘risk aversion’ shift in the global macro markets this past week lead by the US benchmark. However, the technical foundations of the bull trends remain intact with little event risk, disengaged systemic themes and seasonal expectations factoring in.

Talking Points:

Risk trends have wavered this past week, but not enough to undermine robust bullish trends like that seen on the S&P 500

Between a short-term pullback and long-term complacency, strong event risk and active themes will offer critical direction – but we lack for both

Top event risk is extremely light from the docket; but macro traders should watch for US business confidence, key Chinese earnings and China October data prints

Risk Appetite Wavers but Dominant Trends Remain

Risk appetite in the global capital markets took an unfamiliar dive this past week. While we have experienced brief corrections over the past six months, the general course for speculative sentiment since the reversal of the Liberation Day reciprocal tariffs back in April has remained on a firmly bullish setting. And, the past four months has seen fear in the form of implied and realized volatility all but drain away. It is the quiet backdrop that makes the reversal from benchmarks like the Nasdaq 100 experienced seem so loaded and dangerous.

The 3.1% retreat on the week from the - until recently - favored tech index was the sharpest since March. As symbolic as that particular retreat may be, it is important to recognize the breadth of the bearish shift in risk appetite. Global indices, emerging market assets, high yield fixed income, crypto and sentiment-oriented commodities all pulled back from their ebullient highs. For those who monitor for - much less seek out - volatility, it is easy to appreciate how such a shift can spur anticipation of a larger trend reversal.

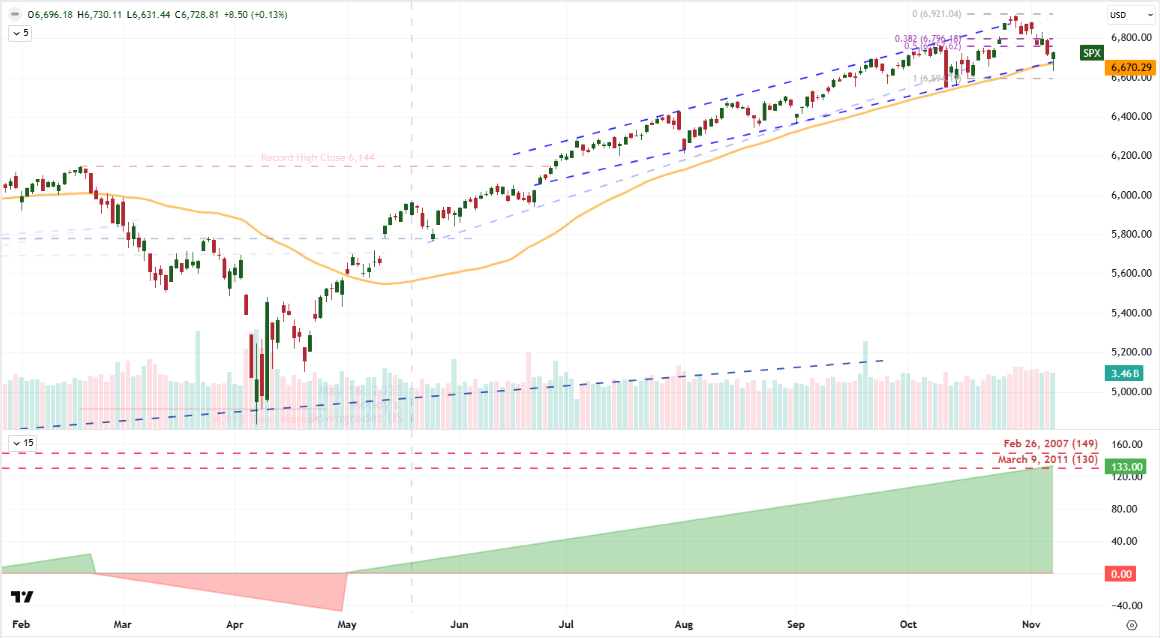

S&P 500 with 50-Day Moving Average and Consecutive Days Above/Below (Daily)

Source: TradingView.com, Standard & Poor’s

A Week Barren of Major Event Risk

Yet, even if there is a fundamental argument to be made for markets climbing to over-indulgent heights, there is no certainty that a trip has to turn into a larger and progressive slide. Pullbacks in larger trends are natural and a breather from successive record highs does not truly reflect a serious rush to the exits by thematically overleveraged market participants. Volatility is certainly a common ingredient to the beginnings of a bearish trend reversal but some of the other critical criteria seem to be absent. Notably, there is leading fundamental theme to concentrate the market's focus.

Trade wars have faded to the background with multi-month delays for negotiations and legal challenges bring played out. Growth concerns and monetary policy speculation have leveled out through cycle balances and a lack of data. Meanwhile, the technical backdrop offers up foundations for larger bullish channel backing like the S&P 500's extending a multi-month trend channel and 133 day spree above its 50 day moving average - the longest such climb in 14 years. Add to that lack of theme and catalyst a deeply rooted complacency borne out of seasonal norms around this period and inertia is likely much more difficult to overcome.

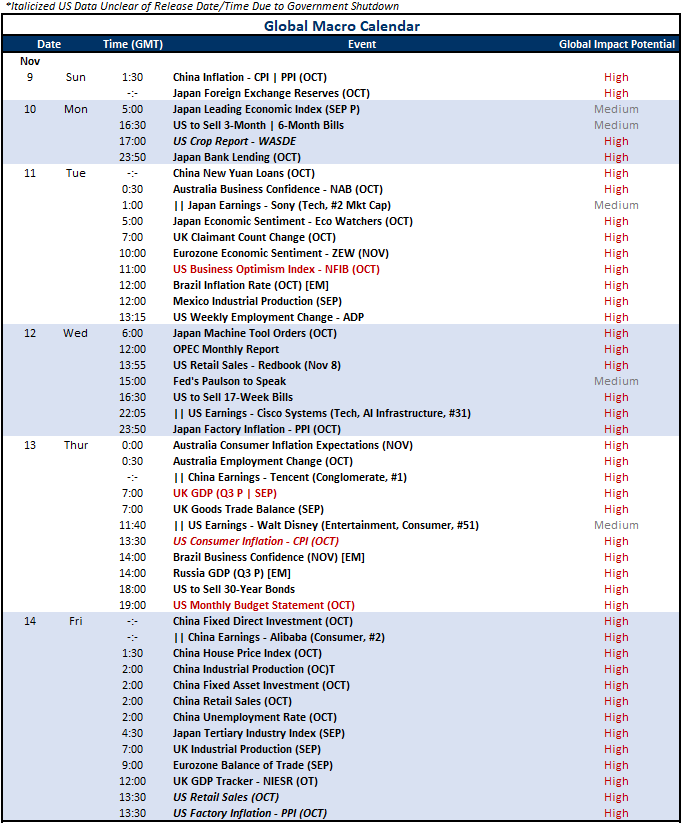

Calendar of Top Global Macro Event Risk

Source: John Kicklighter

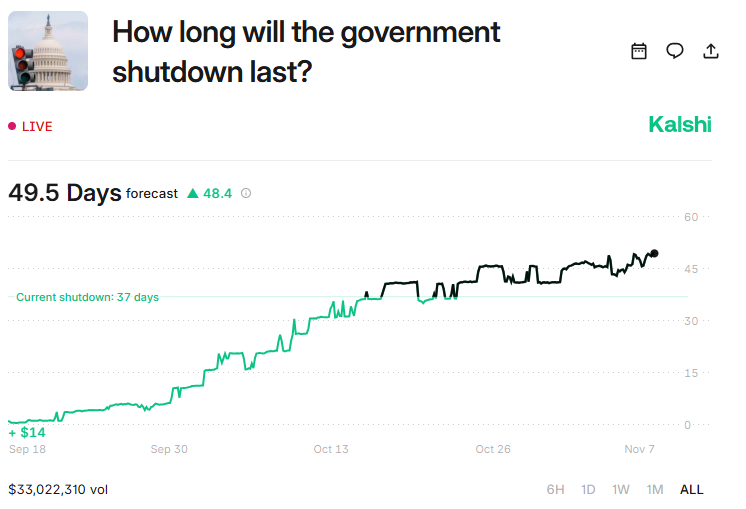

One particular outlier consideration to consider with the limited scheduled fundamental calendar is the ongoing US government shutdown. As of Friday, the government – an engine of output for the world’s largest economy – had been shuttered a record-setting 37 days. Betting markets are actively pricing in the probabilities for when the government will reopen – with a 48-day forecast currently the prevailing timeline from Kalshi. Thus far, the extension of the closure – and its detrimental economic implications – have exerted a measured impact on sentiment.

That said, a resolution could readily spark a sense of risk appetite recover which would conform to the larger trend. This is a significant fundamental consideration with a skewed impact table and almost-inevitable resolution (over time). The ultimate variable seems the timing of the eventual relief and what the technical backdrop looks like when it crosses the wires.

Betting Markets Forecast for US Government Shutdown Duration (Hourly)

Source: Kalshi.com

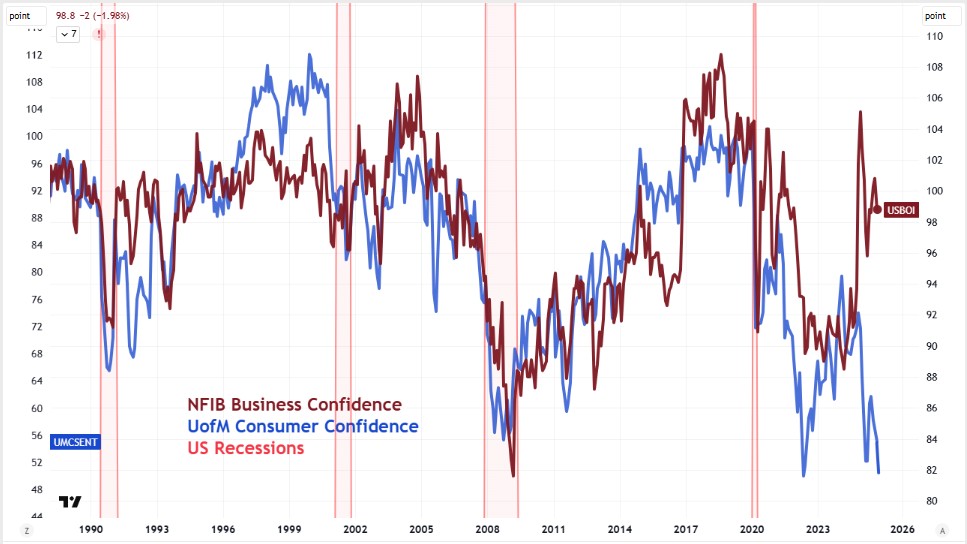

How is US Business Confidence as the Consumer Outlook Collapses?

With the US government shut for more than a month, we have been sorely lacking for reliable economic updates from the world’s largest economy. There is no telling what the most recent update on consumer inflation, retail sales or nonfarm payrolls would have meant for systemic themes from the world’s largest economy; but the attention these readings would have garnered has to go somewhere. That shift is finding areas of strain such as the private sentiment surveys. While there are some moderate readings such as regional Federal Reserve sentiment measures, the more bombastic will inevitably draw more financial headlines.

This past week’s University of Michigan consumer confidence update is just such a lightning rod. The second lowest headline reading on record caters to a deteriorating market sentiment. That is the environment in which we should evaluate subsequent, systemic confidence readings such as the NFIB’s business confidence report. With the American consumer clearly unnerved and the ISM surveys reflecting economic struggle, there is a backdrop of struggle in which this report will wade.

US NFIB Business and UofM Consumer Confidence (Monthly)

Source: TradingView.com, NFIB, University of Michigan

Chinese Earnings Given Insight on Chinese Capital Markets

As the macro calendar clears out, there is still some activity expected from the corporate earnings side of things. The US has a few notables like Cisco and Walt Disney, but these are of substantially lower systemic market influence. Sure these tickers’ earnings will speak to AI (via infrastructure) and consumer health, but these are not themes so on tenterhooks that such financial headlines can readily be considered systemically capable. That said, our focus should not just be on the US corporate landscape. There are a number of countries from which top national companies will be reporting their period updates. From China – the second largest economy – we are due a few very notable updates.

Alibaba is expected to report at the end of the week and there is arguably no Chinese company that better reflects consumer demand from the country that is supposedly attempting to shift its dependency from foreign to domestic demand. Yet, as economic significant as BABA’s earnings are, Tencent’s weight is arguably top tier. The largest company in China by market cap, this conglomerate is easily more aligned to the overall economic health of the economy. That is not to say if the data disappoints that the economic picture will collapse, but it would sow significant doubt…

Chart of Tencent Overlaid with Shanghai Composite (Daily)

Source: TradingView.com, Shanghai Stock Exchange

Chinese Economic Data and the Large Grain of Salt

Speaking of China, the interest this week is more than just on the corporate reporting. The macro docket will offer more than its fair share of data to give insight on the country’s health – if global investors took the data at face value. Ultimately, Western market participants take China’s economic updates with a bolder of salt; but there really is no alternative to these official releases when it comes to evaluating the trajectory of this important player. Earlier in the week, we have inflation (CPI and PPI) as well as new lending figures due for October. These are very important economic updates, but they are not well known for stirring market reaction.

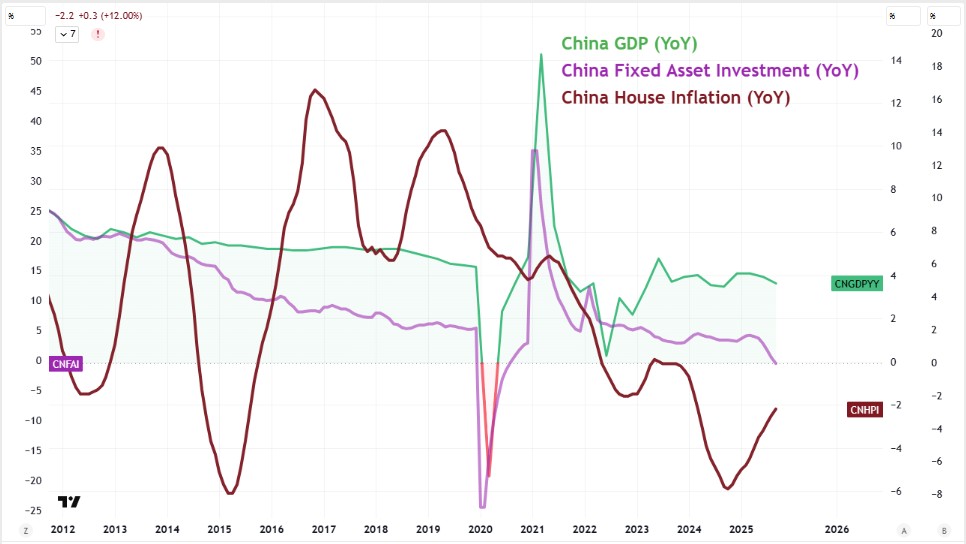

At the end of the week, we navigate into deeper waters with a run of data for the same month covering fixed direct investment, housing inflation, industrial production, retail sales and employment. While the Chinese government has attempted to shift the economy towards domestic dependencies, the temporary drives of cheap lending and foreign appetite remain far more important for the country’s growth. Prioritize appropriately.

China GDP, Fixed Asset Investment and House Prices Year-Over-Year (Monthly)

Source: TradingView.com, China National Bureau of Statistics

-- Written by John Kicklighter, Global Head of Content

The subsidiaries of StoneX Group Inc. provide financial products and services, including, but not limited to, physical commodities, securities, clearing, global payments, risk management, asset management, foreign exchange, and exchange-traded and over-the-counter derivatives. These financial products and services are offered in accordance with the applicable laws in the jurisdictions in which they are provided and are subject to specific terms, conditions, and restrictions contained in the terms of business applicable to each such offering. Not all products and services are available in all countries. The products and services offered by the StoneX Group of companies involve risk of loss and may not be suitable for all investors. Full Disclaimer.

This content is not intended for residents of any particular country, and the information herein is not advice nor a recommendation to trade nor does it constitute an offer or solicitation to buy or sell any financial product or service, by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Please refer to the Regulatory Disclosure section for entity-specific disclosures.

No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc. The information herein is provided for informational purposes only. This information is provided on an ‘as-is’ basis and may contain statements and opinions of the StoneX Group of companies as well as excerpts and/or information from public sources and third parties and no warranty, whether express or implied, is given as to its completeness or accuracy. Each company within the StoneX Group of companies (on its own behalf and on behalf of its directors, employees and agents) disclaims any and all liability as well as any third-party claim that may arise from the accuracy and/or completeness of the information detailed herein, as well as the use of or reliance on this information by the recipient, any member of its group or any third party.

Currencies

The subsidiaries of StoneX Group Inc. provide financial products and services, including, but not limited to, physical commodities, securities, clearing, global payments, risk management, asset management, foreign exchange, and exchange-traded and over-the-counter derivatives. These financial products and services are offered in accordance with the applicable laws in the jurisdictions in which they are provided and are subject to specific terms, conditions, and restrictions contained in the terms of business applicable to each such offering. Not all products and services are available in all countries. The products and services offered by the StoneX Group of companies involve risk of loss and may not be suitable for all investors. Full Disclaimer. This content is not intended for residents of any particular country, and the information herein is not advice nor a recommendation to trade nor does it constitute an offer or solicitation to buy or sell any financial product or service, by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Please refer to the Regulatory Disclosure section for entity-specific disclosures. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc. The information herein is provided for informational purposes only. This information is provided on an ‘as-is’ basis and may contain statements and opinions of the StoneX Group of companies as well as excerpts and/or information from public sources and third parties and no warranty, whether express or implied, is given as to its completeness or accuracy. Each company within the StoneX Group of companies (on its own behalf and on behalf of its directors, employees and agents) disclaims any and all liability as well as any third-party claim that may arise from the accuracy and/or completeness of the information detailed herein, as well as the use of or reliance on this information by the recipient, any member of its group or any third party.

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bi-lateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve; our financials and record of accomplishment are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform, to “boots on the ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.