The intention of the below graphs are not to be used to say "my price should be X based on this graph". These prices are derived from an FOB price point average. The intent is to show major global price movement trends. Your values will likely have significant basis difference (similar to your local grain price being different than the traded market price).

This graph is labeled as MT in USD currency.

I am still worried that the global supply situation will outweigh buyers trepidation. Demand appears to be much slower this year than recent years past...and that is no shock. With farmers struggling with lower grain prices, it makes sense that buying delays will become more the norm. However, our overall N demand for fertilizer 2025 (July 1, 2024 - June 30, 2025) remains relatively unchanged to last year...and supplies haven't improved. EU continues to operate at approximately 75% of normal. Trinidad has been struggling with production rates due to gas issues. Then we have to take into account "normal" nitrogen production issues. Each by itself may not seem such a big deal, but when combined it becomes concerning. Then we have to figure out global urea outlook which continues to lean bullish.

Based on all of the above, I still lean toward higher prices coming. I think if grain prices were better, we would already be seeing them. The delayed demand is causing prices to stall, but eventually spring preparations need to be made and when that happens, sellers will be ready.

EU production remains at 75% of normal, cutting global supplies

It's the story that keeps on giving, Clark...

Another month and another lack of change from the EU region. Natural gas values remain decently higher than what has been considered historically "normal" for the region. Russia supplies dried up following the argument surrounding the Nordstream 2 pipeline and then Russia's invasion of Ukraine. Dutch TTF values as a result went from single digits to a high of $103MMbtu and now back into the $11 - $13 range (depending on the day). Fortunately, production rates have improved significantly from where they were when natural gas prices topped out. Unfortunately, rates are still 75% with little to no signs of improving short term.

So what does that actually mean?

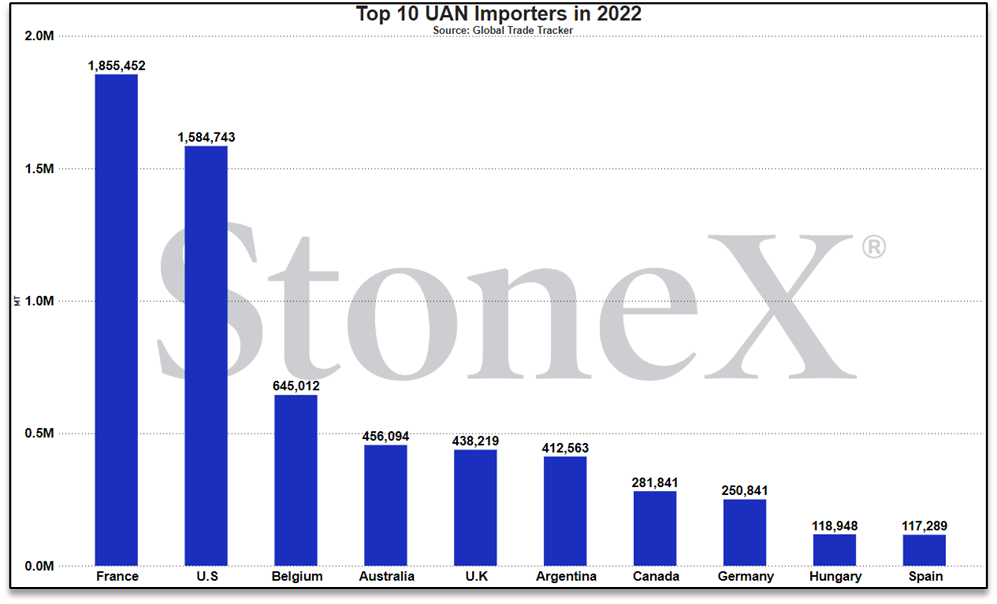

When we look at the whole of Europe (west/central/east), they would normally produce around 9M tons of UAN. 25% of that is around 2.25M tons that is "missing". Globally, there is around 33M tons produced so that 2.25M is a significant number (even more significant with Trinidad hiccups...). This shortfall in production has caused Europe to become an unnatural buyer and as a result, has gifted manufacturers in places like Trinidad and North America new demand that help alleviate unsold inventories when their domestic buyers are not interested.

There is little hope of values returning to normal near term. Remember that the Nordstream pipeline was destroyed/attacked. At least for a section of that pipe, sea water has been inside and is likely eating the metal and making it useless going forward. While repairs can be made, that isn't expected as Russia continues its invasion of Ukraine. Just seems as though this will be a story that I can copy/paste for the next several editions...

What does this means for farmers?

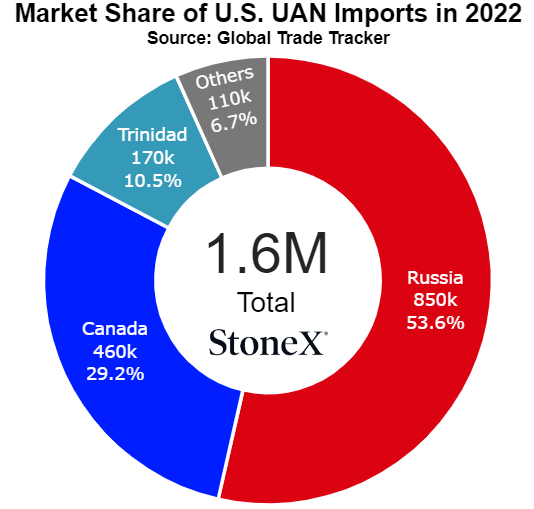

Not only does the EU situation lower global supplies, it also raises global demand as they have to look to replace those tons. The EU has been an unnatural buyer of UAN which has created additional competition around the world. More competition in an arena with less supply typically causes prices to rise. Global buyers are put into a bad situation.

Trinidad production curtails due to tight gas supplies

Speaking of production issues...Trinidad.

For a little while, Trinidad has struggled with insufficient natural gas supplies. This has seen some of their sectors, including nitrogen production, curtail until supplies improved. Fortunately, earlier this year, the government approved the development of previously untouched territorial waters/supplies. Very quickly we saw partnerships and investments made to build out this new territory. This should help Trinidad to rebuild their natural gas supplies to solid levels that should keep industrial demand steady...eventually, but not today. That development will take time.

Today, the struggle continues and in the last month, we have continued to see and hear nitrogen production problems. Worsened production rates lowered available UAN for export and as a result, we have seen U.S. manufacturers enjoying the benefit as they backfill the void.

Hopefully these issues will be fewer in the immediate future and almost non-existent in the further future but today, it is a story that is very real and has very real world implications.

What does this means for farmers?

Fortunately, this is not the double edged sword that the EU situation is. Trinidad having production issues only affects global supplies...but it still affects global supplies in a world that is already more tightly supplied.

...sorry, using "supplies" 3 times in a sentence seems too much!!

On the bright side, I do not think the Trinidad situation will spiral out of control and into a story of "they are completely offline long term". These curtailments happen there and with new natural gas development in the process, these stories should become fewer and farer between. For the short term, we do still need to track as it adds fuel to the fire.

Will Russian UAN production shift more to urea?

The global markets are struggling with tighter supplies of both urea and UAN. From my perspective, both are about to move into a sellers paradise...but which is worse?

In the urea world, it is bad. Chinese exports do not exist. Egypt continues to have hiccups. The EU region continues at 75% operating rates. Brazil is offline. The UAN side is bad, but doesn't seem as bad. As mentioned with urea, production rates are around 75% of normal and Trinidad has had some short-term issues.

So now look at it from Russia's POV.

For UAN, you are very reliant on the U.S. continuing to be willing to accept your shipments and you know that domestic U.S. manufacturers would love nothing more than for the government to block you. It almost has a "living on borrowed time" feel. However, if they can shift more production to urea, it feels much tighter and there are a LOT more buyers around the world that are friendly.

So why continue to try and shove a square block into a round hole...I'm not sure which nation is which but just go with it!!!!

I cannot speak intelligently about Russia's ability to sway urea/UAN production back and forth but if I were them and I had the opportunity, I might be leaning a little harder on urea today...

What does this mean for farmers?

Again, if this is possible and a route that they decide to follow, even LESS supply is available.

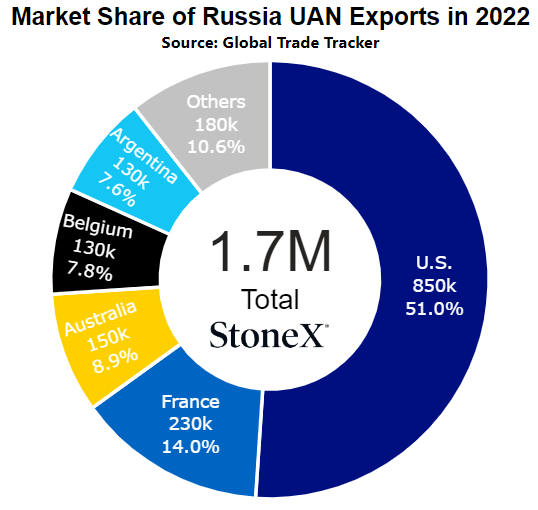

Russia has actually been one of the bright fertilizer stories of the last couple years. Their export rates of most products have helped to shore up supplies/offset production and export issues.

If they shift more to urea, that will certain help alleviate some of the problems with that market...but will cause more problems for UAN. More problems means higher prices in this case.

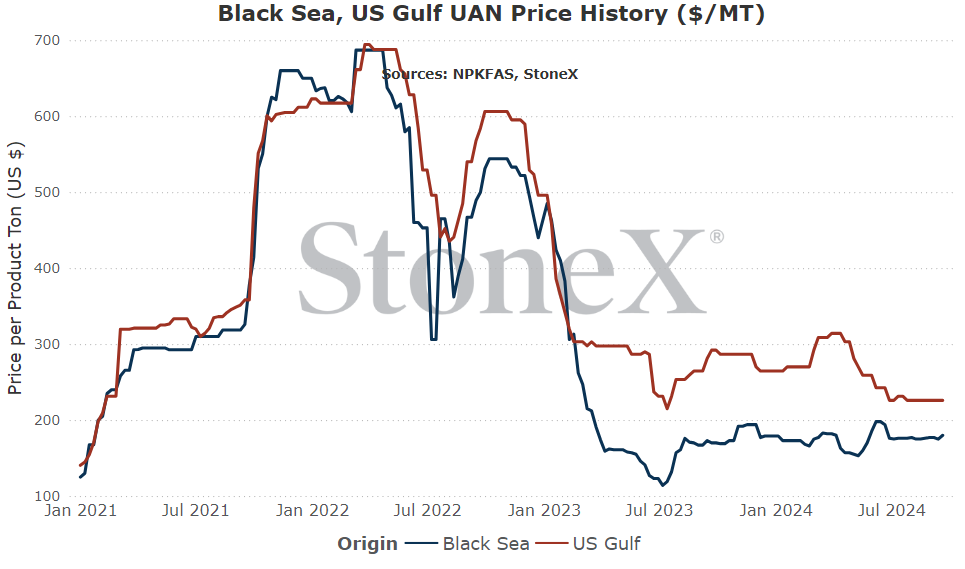

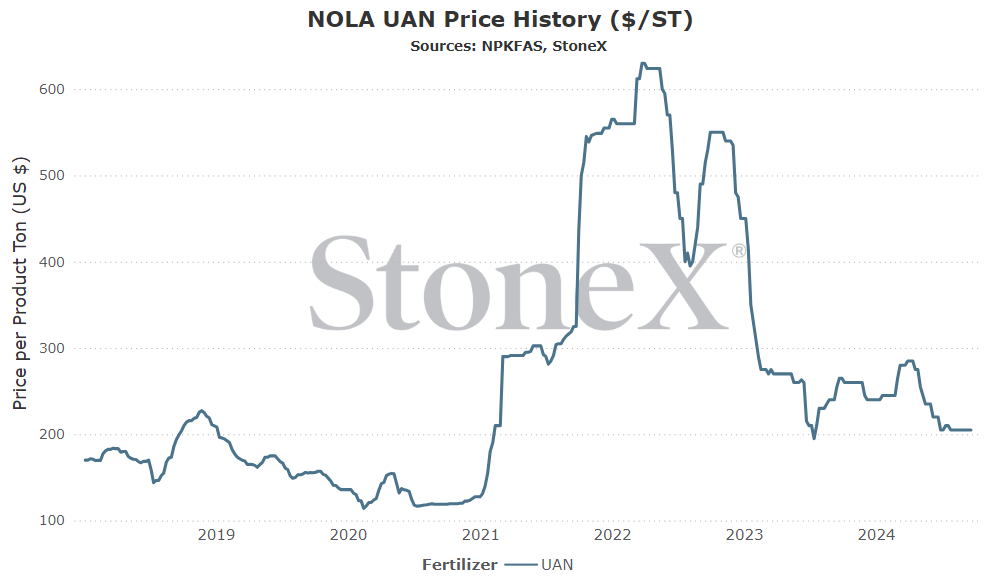

NOLA/New Orleans, Louisiana

Number 2 global importer in 2022

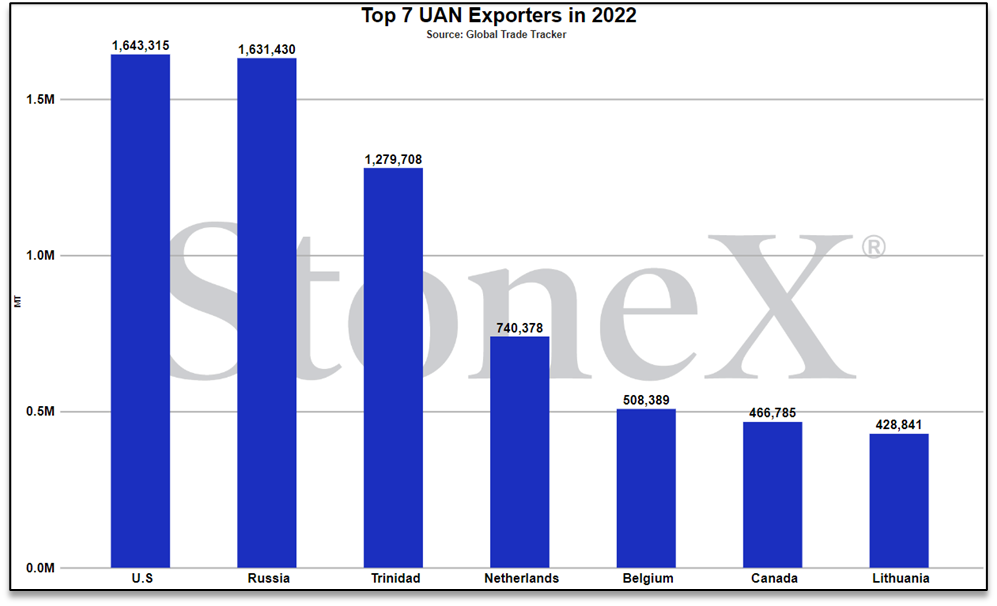

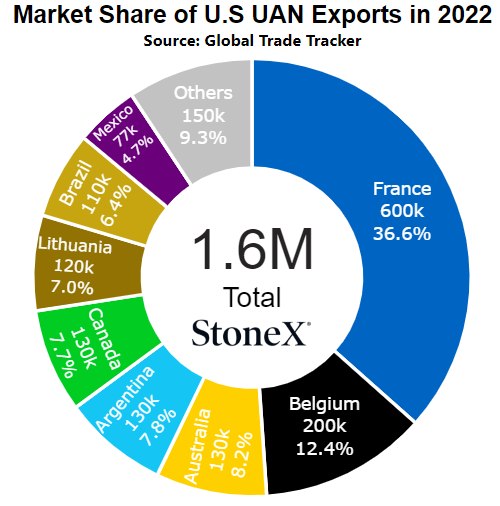

Number 1 global exporter in 2022

Price comparisons

Vs 30 days ago - unchanged vs last month

Vs 90 days ago - -7% or approximately $15 lower

Vs 6 months ago - -28% or approximately $80 lower

Vs 1 year ago - -23% or approximately $60 lower

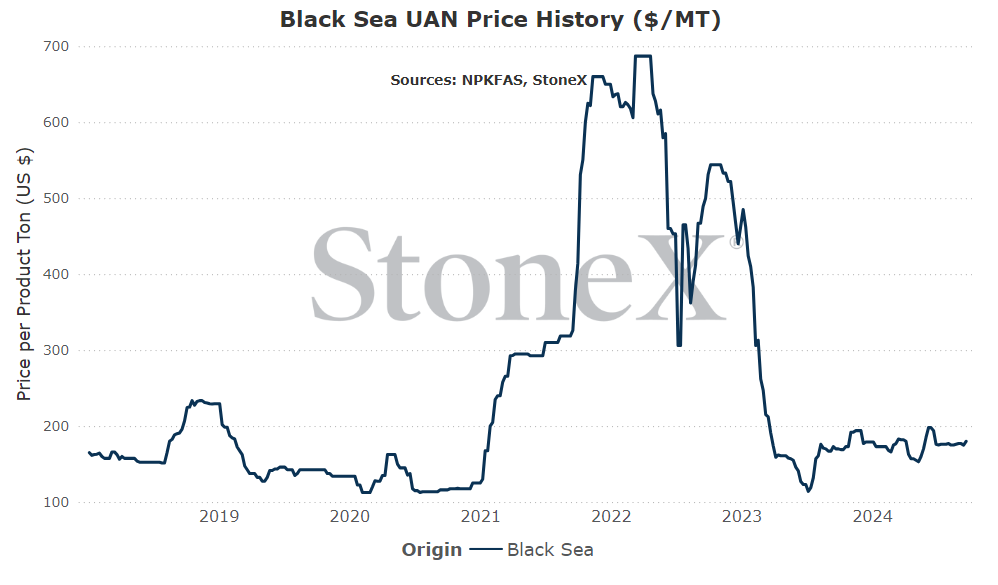

Black Sea (Russia)

Number 2 global exporter in 2021

Price comparisons:

Vs 30 days ago - 2% or approximately $4 higher

Vs 90 days ago - -7% or approximately $14 lower

Vs 6 months ago - -1% or approximately $2 lower

Vs 1 year ago - 6% or approximately $11 higher

- Further cuts to EU production rates – with west/central Europe still at an approximate 75% operating rate, that equates to roughly 2M tons per year of UAN not being produced. Unfortunately, that rate has not improved for a while. Fortunately, it has not gotten worse. Unfortunately, it can certainly get worse. Europe has had a couple very mild winters back to back which helped to lower natural gas values. If they make up and have a very harsh winter, we could certainly see gas values rise...and production rates of UAN fall.

- Trinidad production issues continue – on the plus side, Trinidad has approved the development of new natural gas waters in its territory. Unfortunately, it will take time to develop the production. Until then, I'm afraid Trinidad nitrogen production curtailments could be a fairly common story. Every week they scale back/shut down are tons of UAN lost in an already tightly supplied global market.

- U.S. imposes import duties on Russia (copied from N.A. version as it also affects Australia) – this still remains very low on my probability list...but it looms large on the impact list. If we were to see the U.S. start taking steps to limit or ban Russian imports of UAN, we would no doubt see domestic values rally very quickly. Russian imports have helped to offset U.S. exports and keep our values relatively stable. I want to believe D.C. wouldn't even think of doing this to N.A. farmers...

- Buyers/farmers continue to drag their feet (copied from N.A. version) – farm economics for 2024 remain poor. Farm economic forecasts for 2025 remain poor. Spring application remains a long way away. While there are certainly things to fear in terms of UAN prices going higher, buyers largely do not care today and are opting to wait to purchase. This is causing the market to stall. This happens long enough and manufacturers may need to start changing their approach to move product.

- EU/Trinidad production returns to normal – this doesn't seem likely but given how important they are on the bullish side, it is worth remembering on the bearish side. If we were to see either/both return to full production form, that would be a boost to global supplies which should lean on values.

- Substantial shift in 2025 acreage mix that hurts N demand – today, we are holding steady on our 2025 acreage mix which means our overall N demand remains steady/slightly higher than last year...but that isn't guaranteed. Markets change all the time and we are a very long way away from spring planting. Intentions can change and if they change away from nitrogen needing crops, we could see price pressure on UAN.

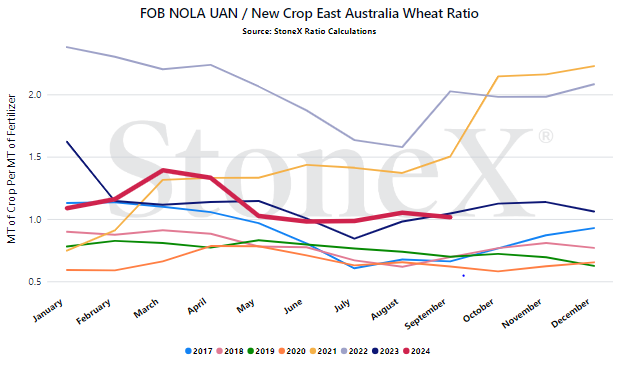

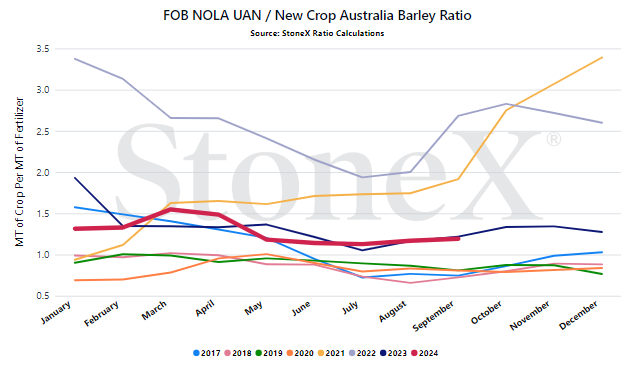

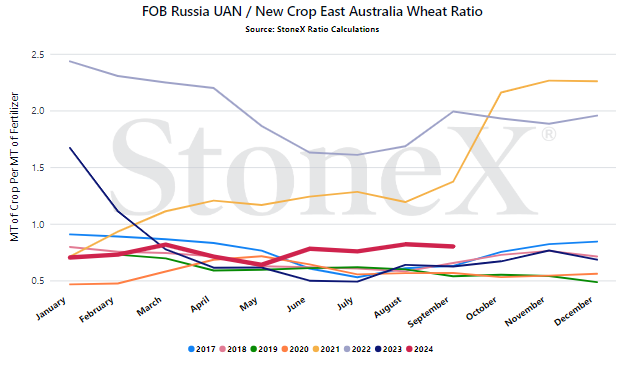

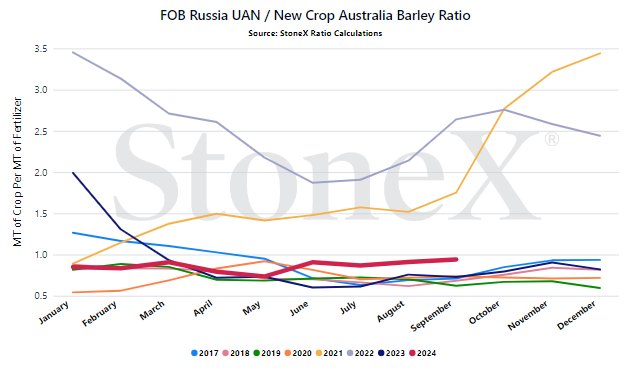

We believe that only looking at the flat price of either grains or fertilizer can be misleading:

-

Only selling grain can hurt you if fertilizer prices rise substantially

-

Only buying fertilizer can hurt you if grain prices fall

We look at the ratio "value" to get a better indication of where we are or how many bushels of X does it take to pay for 1 ton of fertilizer.

Would you rather:

-

Spend 100 bushels to pay for 1 ton of UAN

-

Spend 60 bushels to pay for 1 ton of UAN

When we compare the current ratio value against recent years, we start to see if we are high or low.

YOUR VALUES MAY LOOK DIFFERENT

This graph looks at the NOLA UAN price vs the flat grain price. There are no logistics on either product. Your location will look different due to fertilizer logistical costs, grain basis, etc.

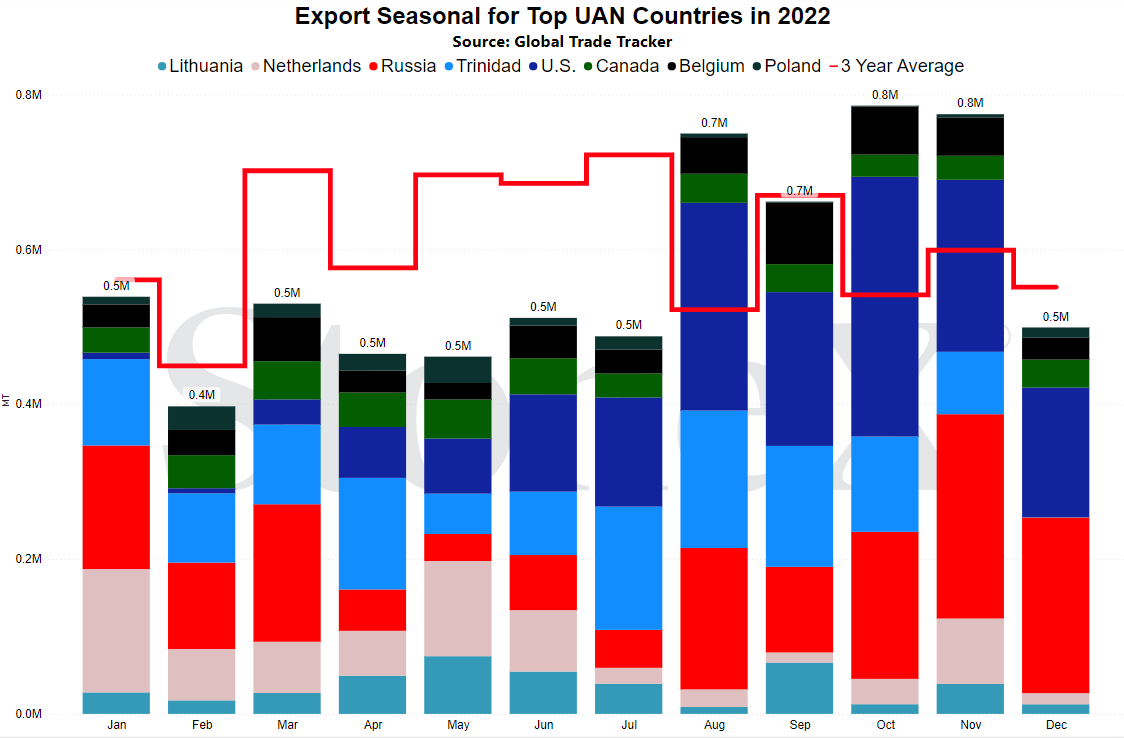

- EU/Trinidad production rates - when compared to urea and NH3, the global UAN market is significantly smaller...which means that production hiccups are felt that much worse. The EU region is unchanged with production rates at 75% of normal due to high natural gas values. That has removed 2+M tons of production from the world. Recent Trinidad production curtailments due to tight natural gas supplies highlights how quickly another major player can be lost. Fortunately, global UAN values continue to be following in urea's footsteps but a couple more issues like this and it could cause UAN to break away on the higher side.

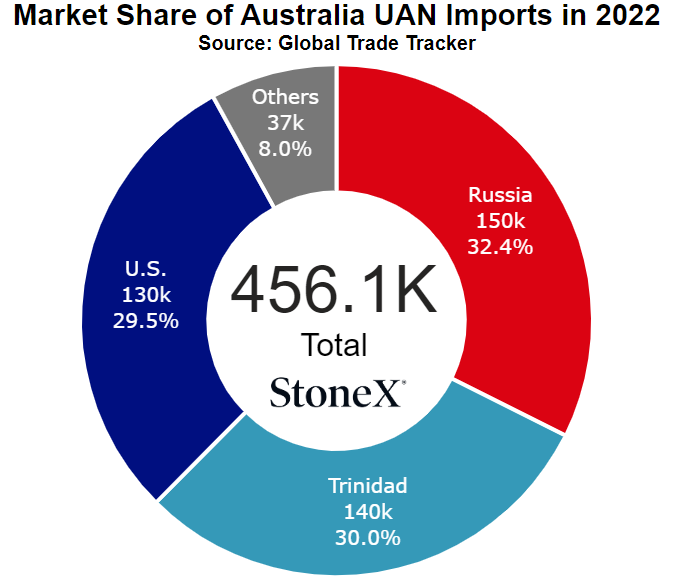

- U.S. imports/exports (U.S. activities matter to Australia due to exports) - UAN exports from the U.S. continue at a heavy pace. This has been helped recently with Trinidad production issues. July saw exports of 226K tons with almost all of those tons leaving North America (Australia/Argentina/France/Columbia). Normally, a lack of buying domestically would cause weakness in values but the fact that manufacturers have a "relief valve" in exports gives them more time. Fortunately, imports continue as well though they were a bit short at 121K. This dynamic needs to continue to be watched, especially if steps start being taken to block certain imports. If we lose that, hard to see where UAN wouldn't move higher...

- Farmer sentiment with spring so far away (again, N.A. farmer sentiment matters) - while most of my outlooks foresee higher UAN values, I cannot understate pissed off farmers. Farm economics stink for 2024. Farm economics stink for 2025. Yes, the demand outlook still looks solid and exports continue to be a thing...but do not underestimate farmers. We could see demand remain nearly non-existent for a while longer. April/May is still a very long way away. If this happens long enough, maybe we see some short term weakness. Maybe.

StoneX Ratio Calculation

The ratio calculation is derived from Bloomberg historical grains values as well as fertilizer values from StoneX, NPKFAS, and Argus.

The calculation is simply dividing the fertilizer price by each grain price.

All data was sourced from StoneX unless otherwise noted.