CBOT Grains Daily Options Report

Recap of day's options activity and data.

PJ Quaid

- Grains & Oilseeds

By: Arlan Suderman, Chief Commodities Economist

February 19 – Stocks remain in the red at mid-day, with the Dow Jones leading the way lower, followed by the Nasdaq, then S&P 500 amid concerns of a divided Fed and rising geopolitical risks. Uncertainty appears to be creeping back into the minds of Wall Street traders, with the VIX rising back above the 20-mark today after dipping to a six-day low just below 18.5 yesterday. The dollar is extending yesterday’s gains as this morning’s economic data continues to point to a more resilient than expected U.S. economy, weakening the doves’ case, especially in the context of an already skeptical FOMC (more on that below). Treasuries are trading just above unchanged at the time of writing, with 10-year yields at 4.085% and 2-year yields at 3.470%. Crude oil prices are continuing to spike as the buildup of military assets in the Middle East carries on and weekly U.S. fundamental data comes in much tighter than expected, pushing nearby WTI to a fresh six-month high just below the $67/barrel mark earlier in the session. The ags are largely mixed, with the wheat complex leading the way higher on a combination of the aforementioned geopolitical risk, especially with Russia’s potential tie-in to the U.S./Iran tensions, as well as worsening forecasts in major winter wheat producing regions, all taking place amid sizable net managed money shorts.

The minutes from the FOMC’s January meeting that were released yesterday afternoon point to a divided Fed in 2026—no surprise given the upcoming change of leadership as current Fed Chair Jerome Powell’s term ends in May and Kevin Warsh takes over. Despite political pressure for lower rates, several Fed officials appeared notably hawkish, with some pushing for a “two-sided” final statement to reflect the possibility of needed rate hikes if inflation remains at above-target levels. In the end, the Fed’s final statement from the January meeting remained one-sided, focusing only on whether or not there would be more cuts. We’ll get an update on the Fed’s preferred inflation metric, the PCE, tomorrow. As a reminder, headline PCE has been above the Fed’s 2.0% mandated level for nearly five straight years now, as has headline CPI; this doesn’t support additional rate cuts. On the other side of the Fed’s dual mandate, the U.S. labor market has continued to prove more resilient than expected, as evidenced by another lighter than expected week of jobless claims reported this morning; that doesn’t support additional rate cuts either. Fed officials were also notably more optimistic about the labor market than previously in 2025, with the minutes saying, “the vast majority of participants judged that labor market conditions had been showing some signs of stabilization and that downside risks to the labor market had diminished.” Others did continue to point to downside risks remaining, especially in a “low-hiring environment,” again highlighting the growing internal divide.

CME’s FedWatch tool still points to market expectations of the Fed’s next rate cut coming at their June meeting, which will be the first under the new leadership, though the probability of such a cut did fall following the release of the minutes yesterday. The highest odds are for a total of two 25-basis point cuts by the end of 2026, which would bring the Fed’s target rate to 3.00% - 3.25%. Look for significant debate among FOMC members to be a central theme hanging over the broader markets in 2026, especially in the latter half of the year.

Pending home sales fell 0.8% month over month in January, sharply missing analyst expectations of a 1.3% month-over-month rise. December’s ugly drop was revised from the -9.3% originally reported up to -7.4%, though that still represents the worst monthly decline in home sales seen since April 2024 as the housing market remains relatively tepid. In year-over-year terms, pending home sales fell 0.4% in January, with notable declines seen in the Northeast (-8.3%) and Midwest (-3.3%) while the West (+0.3%) saw small gains and the South (+4.0%) saw the largest increase. Despite falling mortgage rates, with the national average 30-year rate falling to 6.09% in this morning’s update from Freddie Mac, National Association of Realtors Chief Economist Dr. Lawrence Yun noted that “improving affordability conditions have yet to induce more buying activity.” Yun also pointed to the need to increase housing supply due to the potential for a notable uptick in buyers stepping forward in 2026 which could drive home prices up further.

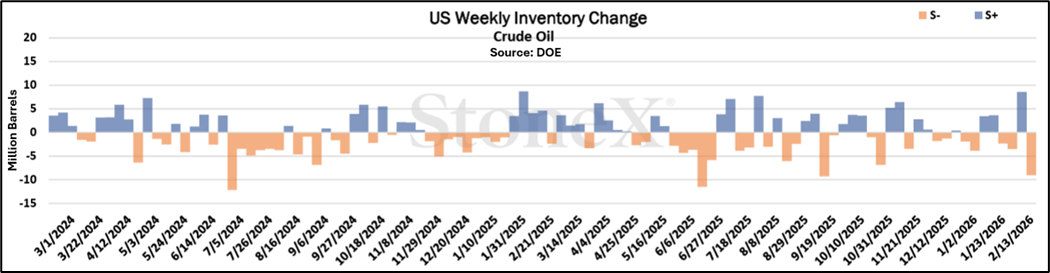

U.S. crude oil stocks fell by 9.01 million barrels week-over-week in the week ended 2/13, dramatically sharper than the expected 2.149-million-barrel increase expected by analysts and marking the largest weekly decline seen in five months. This puts total U.S. crude oil stocks, excluding the SPR, at 419.82 million barrels, the lowest level of 2026 thus far. This surprisingly bullish data adds to an already red-hot crude oil market amid rising tensions between the U.S. and Iran, driving WTI to a six-plus month high at mid-day. Throw in the potential tie-in to the Russia/Ukraine conflict with Iran and Russia continuing to conduct joint naval drills in the region today in response to the ongoing buildup of U.S. military equipment in the theater, and the risk to global crude supply looks even broader. Elsewhere in today’s DOE report, refined products also saw much sharper than expected draws, with U.S. gasoline stocks falling 3.213 million barrels week-on-week versus estimates of a much lighter 0.284-million-barrel drop, and distillate stocks falling 4.566 million barrels week-on-week versus estimates of a 1.440-million-barrel drop. Refinery utilization also jumped much sharper than expected, up 1.6% week-on-week to a four-week high of 91.0%, well above the estimated 0.4% weekly uptick.

This material should be construed as market commentary and represents the opinions and viewpoints of the author, and does not reflect tailored advice associated with any specific account.

The views are current only through the date stated and are subject to change at any time based upon market or other conditions, and StoneX Group Inc. (“SGI”) disclaims any responsibility to update such views. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. Past performance does not guarantee future results.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided.

References to certain OTC products or swaps are made on behalf of StoneX Markets, LLC (SXM), a member of the National Futures Association (NFA) and provisionally registered with the U.S. Commodity Futures Trading Commission (CFTC) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ and who have been accepted as customers of SXM.

StoneX Financial Inc. (SFI) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (SEC) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Advisor. StoneX Financial (Canada) Inc. (SFCI) is registered in Canada and is a member of CIRO and CIPF. References to certain securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to certain exchange-traded futures and options are made on behalf of the FCM Division of SFI. Wealth Management is offered through SA Stone Wealth Management Inc., member FINRA/SIPC, and SA Stone Investment Advisors Inc., an SEC-registered investment advisor, both wholly owned subsidiaries of SGI.

R.J. O’Brien & Associates, LLC (RJO) is registered with the CFTC as a Futures Commission Merchant and is a member of NFA.

StoneX Financial Ltd (SFL) is registered in England and Wales, company no. 5616586. SFL is authorized and regulated by the Financial Conduct Authority (FCA) (registration number FRN:446717) to provide services to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorized to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorized and regulated by the FCA under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorized by the FCA.

This communication is issued in the European Economic Area by StoneX Financial Europe GmbH (SFEG). StoneX is the trade name used by STONEX GROUP INC. and all its associated entities and subsidiaries. StoneX Financial Europe GmbH (“SFEG”) is a securities trading firm registered in Germany under Company No. HRB 80844.

StoneX Financial Pte Ltd (Co. Reg. No 201130598R) (“SFP”) is regulated by the Monetary Authority of Singapore and is a Capital Markets Service Licence holder (for dealing in capital market products), an Exempt Financial Adviser (for advising on investment products and issuing or promulgating analyses/ reports on investment products) and a Major Payment Institution (for domestic and cross-border money transfer services).

SFP may distribute analysis/report produced by its respective foreign affiliates within the StoneX Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations Recipients should contact SFP at (65) 6309 1000 for any matters arising from, or in connection with, this webinar.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism.

StoneX Financial (HK) Limited (CE No.: BCQ152) (“SHK”) is regulated by the Hong Kong Securities and Futures Commission for Dealing in Securities and Dealing in Futures Contracts.

StoneX Financial Pty Ltd (ACN 141 774 727) holds an Australian Financial Service License (AFSL: 345646) for Dealing in Securities, Exchange-Traded Derivatives Contracts, OTC Derivatives Contracts and Foreign Exchange Contracts, and is regulated by the Australian Securities and Investments Commission.

StoneX Securities Co., Ltd. (“SSJ”) (Co. Reg. No 010401047199) is regulated by the Japanese Financial Services Agency as a Type-I Financial Instruments Business Operator (Kanto Local Finance Bureau (FIBO)No.291’), is a member of the Financial Futures Association of Japan for dealing and broking FX and FX Option transactions, and is a member of the Japan Securities Dealers Association for dealing and broking stock indices and option transactions.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

The report/analysis herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

© 2026 StoneX Group Inc. All Rights Reserved.

Our subscribers have access to comprehensive market analysis from StoneX spanning commodities, equities, currencies and more.

Recap of day's options activity and data.

Bevan Everett Grain Recap Chinese Translation

Kansas City Wheat Report

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bi-lateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve; our financials and record of accomplishment are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform, to “boots on the ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.