May 2 – Stocks are looking to end a strong week on a strong note, with optimism abounding on Wall Street at mid-day after this morning’s better-than-expected jobs data as well as a potential easing of trade tensions between the U.S. and China. This is also allowing the VIX to cool to its lowest level in a month, trading below 23 for the first time since April 2nd. The dollar is wiping out this week’s gains, pushing back below the 100 level as it hovers near 99.6 at the time of writing. Treasuries are ending the week on a strong note, with 10-year yields trading at 4.31% and 2-year yields trading near 3.81%. Crude oil is ending an ugly week on a weak note, with WTI down another 1.3% on the day as it hangs just above $58/barrel. The ags are mostly higher on the day, save for soybean oil, with the wheat complex leading the way higher as it rebounds from contract lows made earlier in the week.

Another positive takeaway from this morning’s jobs data was an unexpected decline in the U-6 unemployment rate down to 7.8% versus expectations of a rise back to 8.0%. The U-6 rate goes a step further than the headline reading by adding in individuals who are underemployed, those forced to work part time because they can’t find full time employment but aren’t technically unemployed, as well as marginally attached workers who have given up in their job search. This provides a deeper picture of the labor market and had been trending higher through much of 2024 before hitting a three-plus year high in February at 8.0%. Today’s reading is the lowest for the measure since January, again providing some welcomed optimism regarding the resiliency of the U.S. labor market to end the week and helping drive stock higher.

Headline factory orders in the U.S. jumped 4.3% month-on-month in March, up sharply from 0.5% growth in February and marking the hottest growth seen since July, though still slightly below analysts' expectations of 4.5%. However, like much of the March economic data we’ve seen in recent weeks, this was driven largely by consumers front-loading purchases ahead of impending tariff announcements at the start of April, especially on vehicles. Excluding transportation, U.S. factory orders actually fell 0.2% month-on-month in March, well below market estimates of 0.2% growth and marking the first drop seen since August. Again, we’ll need to wait for more hard data post-tariffs to see the true impact on the U.S. economy thus far, though this reading is far from encouraging.

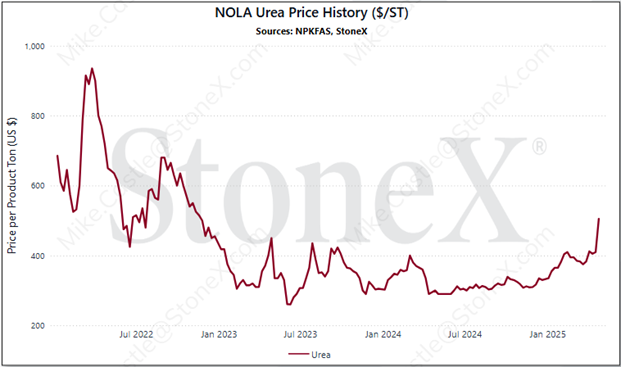

While most of the focus on President Trump’s announcement of secondary sanctions on countries making purchases from Iran is centered on Iranian oil, this threat includes direct implications for the ag industry, as both anhydrous ammonia and urea are considered petrochemical products and would therefore be subject to secondary sanctions. Domestic fertilizer prices have already been spiking this spring, especially on the nitrogen side. In fact, front-end New Orleans (NOLA) urea prices traded to a fresh high of $523/ton this morning, the highest level seen since November 2022, when prices were still working their way downward from all-time highs made earlier that year. Despite the tranche of existing sanctions that have already been in place, Iran is still the world’s third largest urea exporter as well as the seventh largest anhydrous ammonia exporter, making them a very important global nitrogen supplier. Ongoing Chinese export restrictions exacerbate this issue, though there have been rumors of their return at some point in the late second quarter (though this is far from a guarantee). The real question will be whether or not these sanctions can actually be enforced or lead to a realized slowdown in trade, as Iranian fertilizer shipments are already very adept at dodging sanctions by claiming to be from other origins, primarily Oman and other nearby Middle Eastern nations.