Reuters Base Metal Price Polls

Every three months of the year, StoneX takes part in Reuters’s base metal price forecast polls. This article will highlight the average market expectations for each metal in the suite and StoneX’s view for prices out to 2025.

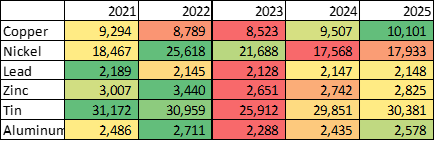

Reuters Base Metal Price Poll Forecast - Annual Mean Price $/t

Source: Reuters

With the exception of nickel, market forecasts all point to the weak performance in 2023 to act as a floor, with prices in 2025 elevating from 2024. Meanwhile, looking at 2025 prices, copper is the standout metal, the only one forecast to move higher than 2022’s levels.

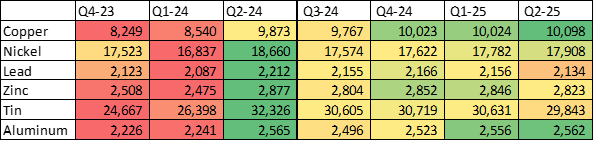

Reuters Base Metal Price Poll Forecast - Quarterly Mean Price $/t

Source: Reuters

Copper

• The market mean is forecasting for Q1 to remain the lowest quarter this year, followed by Q3, then progressive increases into H2 2025. Q4 and Q1 2025 price forecasts set to be very similar.

• On an annual basis, 2023’s dismal performance will remain the floor in these forecasts with averages moving over the $10,000 mark by 2025.

Copper: Our View

The weak performance of copper over Q3 was expected given the re-focus of the markets onto the reality of weak demand, building stocks and the fall out of the fund driven short COMEX squeeze. We are bullish for copper to year-end (once we get past August), with the first U.S. rate cut in sight, the promise of more fiscal stimulus out of China and further expected tightening on the supply side with October/November the timing for annual negotiations between major miners and Chinese smelters.

For 2025, we forecast the delayed cyclical demand recovery story to have begun (having been delayed from Q1 this year to Q4/Q1 2025), with investors' interest on copper’s long-term story renewed. It is still likely that COMEX could face future squeezes (given where we are with stocks); however, on risks to the downside, the outcome of U.S. election and any escalation in geopolitical tensions could derail our forecasts.

Nickel

• The market mean is forecasting for 2024 to be the floor for nickel prices (over the five-year horizon), with prices to only tick modestly higher in 2025.

• On a quarterly basis, the average nickel price is set to remain below Q2 2024 level (but above Q1), with quarterly increases ranging from Q3-Q2 2025 from $17,574-$17,908.

Nickel: Our View

With nickel prices trading below $17,000t, the risk of further mining closures is possible, with Anglo American reportedly in the process of looking to shut its nickel unit, while Glencore is halting its operation on the island of New Caledonia. Meanwhile, BBG BNEF are reporting that nearly half of the previously projected mined-nickel capacity in Australia could be eliminated upon further closures. However, Indonesia (the largest producing country of nickel) can operate with narrower margins, keeping the market well supplied.

Please note, given the change in refined nickel feed into LME warehouses moving from mainly Australian producers back in June 2023 (at 72%), to now a majority of Russian and Chinese producers (at 45%), with Australian producers only at ~29%. The outlook for nickel prices remains bearish in the longer-term, with more deliveries from refineries in Indonesia forecast, alongside an acceleration in the LME approval process for various Chinese nickel producing brands.

Lead

• The market mean is forecasting for 2024 to be a year of recovery in prices, following 2023’s weak performance, although the outlook for 2025 is flat.

• Prices to remain rangebound over Q3-Q1 2025, before moving modestly lower.

Lead: Our View

Lead is facing a global divergence with tightness appearing within China, versus excess stocks and weak demand resulting in LME exchange stocks doubling since the start of the year. However, we expect as arbitrage opportunities arise, China’s tightness will start to ease. Overall, we do not forecast robust demand for lead-acid batteries in 2024, and with stocks at their current levels, the outlook for lead is only modestly bullish in the year ahead.

Zinc

• Similarly to lead, the market mean is forecasting for 2024 to be a year of recovery in prices, following 2023’s weak performance, with prices set to accelerate into 2025 (although remain below 2022 robust level).

• Zinc prices set to remain somewhat rangebound over Q4-Q2 2025 from $2,852-2,823.

Zinc: Our View

Zinc holds the position as the third worst performing metal this year, with its increased end-use exposure to the construction industry (versus metals like copper) capping gains. In addition to this, the lift in prices from 2023 level’s resulted in major mine closures coming back online at the start of the year, not to mention the surprise move within Europe to re-start idled smelter capacity, easing supply tightness (both refined and concentrate) – a key theme of previous years. We forecast higher zinc prices in 2025, supported by additional stimulus efforts targeting the construction industry in China and the U.S.

Aluminium

• Similar to zinc, the market mean is forecasting for aluminium prices to extend higher from 2023 into 2024/2025. However, quarterly prices gains are set to be modest.

Aluminium: Our View

The outlook for aluminium has weakened after hitting a near two-year peak in May, given the record level of refined aluminium being pumped out of China and then exported to the ROW. Despite aluminium’s exposure to the green transition and areas of growth such as solar, the weakness in global demand (and especially within China), has made the outlook for aluminium bearish this year. Looking ahead, higher prices are only likely to materialise upon an acceleration in demand, while attention should be paid to the volume of undesirable ‘Type-2 Russian warrants’ being held in LME warehouses, which has been building monthly since May.

Tin

- Just like aluminium and zinc, tin is forecast to move higher from 2024 into 2025, although on a quarterly basis, markets are expecting a marginal pull lower by Q2 2025.

Tin: Our view

While tin is often a metal overlooked in the suite, its fundamental are arguably some of the best, with tin’s use in renewable energy, new technologies (e.g. artificial intelligence & electronics) and energy storage, versus a tightening supply outlook, resulting in the International Tin Association (ITA) forecasting a record 35,700t deficit by 2030 (from a deficit of just 15,300 this year). Looking ahead, with global stocks remaining near record highs, prices of late have come under significant downward pressure; however, the future remains bright.