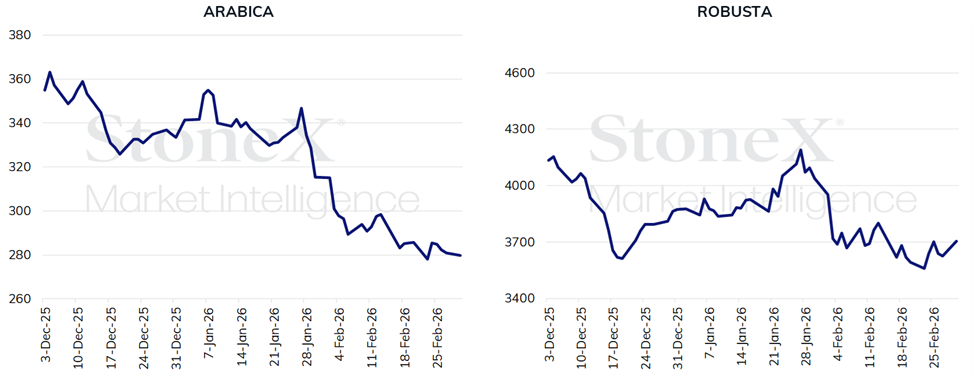

The past week delivered mixed results for coffee futures, with arabica prices falling in New York and robusta prices rising in London. The May arabica contract showed a weekly drop of 1.7%, closing at US¢ 280.75/lb. Meanwhile, in London, despite volatility throughout the week, robusta managed to end with a modest gain of 0.9%, priced at USD 3,624/ton.

In Brazil, optimism persisted, keeping the market under pressure. Positive expectations for the upcoming crop and favorable weather conditions have solidified a low-price scenario, with corrections being punctual and narrow, at least during the first semester.

Regarding arabica, the market remains pressured mainly due to the outlook for ample supply from Brazil's harvest. The incoming crop in the next few months is likely to reinforce the bearish trend and further pressure country differentials.

Recovery in certified stocks: As anticipated last week, certified stocks saw an uptick. ICE reported an increase of almost 20,000 bags, reaching 477,000 bags on Friday (27), the highest level since October last year.

Why it matters: Although still below the average of recent years, the recovery — combined with the expectation of more bags being submitted for grading — helps mitigate the perception of tight global availability. While not a precise reflection of global stocks, certified stocks act as a last-resort reserve and a relevant gauge of available supply.

Robusta with slight gains: Robusta posted modest advances driven by weather instabilities in Vietnam, which may disrupt local dynamics in the short term. Following the return of Asian holidays, the market regained momentum, with producers trying to hold back part of production in anticipation of higher prices, although trade is expected to pick up in the coming weeks. Weather conditions in the country remain under scrutiny.

Brazilian physical market: The Cepea indicator ended the week showing an arabica coffee price of R$ 1,797.6/bag, down 0.5%. Meanwhile, the robusta coffee indicator marked a 1.0% decline, priced at R$ 1,032.7/bag.

What could shift the market's bearish bias?

In a moment of predominantly optimistic perspectives across most major producing countries, except Colombia, new climate instability seems to be the factor most likely to bring volatility to the market.

In this context, while an El Niño scenario already appears highly probable for the second half of the year, monitoring the intensity of the phenomenon will be critical during the pre-flowering period. While a weak El Niño could have positive effects by bringing rainfall to the coffee belt, higher intensity, with significant warming, could raise concerns.

Therefore, based on current monitoring models, this could be the primary factor driving an increased perception of risk among traders and investors, providing more sustained support.

For this week: Alongside weather conditions in Brazil and Vietnam, traders should monitor upcoming releases of Vietnam's export figures and Colombia's production data for February. Preliminary Brazilian export data for last month will also be published by Secex.

Geopolitical conflict and potential impacts on the coffee market

Geopolitical conflict: On Monday, coffee futures prices appeared to be closely linked to heightened geopolitical tensions in the Middle East, particularly stemming from rising crude oil futures.

- Investors fear the conflict could disrupt the Strait of Hormuz, a critical route responsible for about one-fifth of global oil and LNG flows.

- Since the session's start, the surge in energy commodities quickly transmitted to major global commodity indices, which heavily weight oil. Consequently, repricing pulled the entire basket, raising agricultural commodity prices, including coffee, even without immediate changes to bean supply.

- At the same time, the conflict reignites logistical uncertainties, especially due to rising freight costs and higher insurance premiums for routes near the Middle East.

- Higher transportation costs and increased exposure to maritime risks could inflate operational expenses for coffee exporters, particularly those using routes affected by geopolitical instability, adding a risk premium to futures contracts.

- It’s worth recalling that during the 2024 Israel-Iran conflict, freight rates for routes from Asian countries to Europe and the U.S. rose sharply due to regional risk, particularly after armed Houthi group attacks on vessels in the Red Sea.

Long-term impact: Over the medium to long term, however, the effect could take a different trajectory.

- If oil prices remain elevated for an extended period, driven by potential escalation of geopolitical crises, the energy shock might evolve into broader inflationary pressure, reducing disposable income and slowing global consumption.

- This dynamic would likely affect discretionary products, including coffee. Thus, although the current shock is bullish due to indices and logistics, prolonged high energy prices could later create a more moderate consumption environment, introducing a potentially bearish bias for coffee in the medium term.

Weather instabilities in Vietnam and Colombia

Despite the transition of ENSO La Niña to neutrality, some residual effects of the phenomenon persist, contributing to weather disruptions across several regions.

Vietnam: In Vietnam, heavy rainfall in the Central Highlands — the main producing region — raised concerns during the final development stage of some fruits for the 2025/26 crop, increasing the risk of fungal diseases, hindering drying processes, and even causing fruit drop from later flowerings.

StoneX weather maps indicate that rainfall is expected to continue over the next two weeks but at more moderate levels, which may help normalize conditions. Nonetheless, the situation remains under market scrutiny.

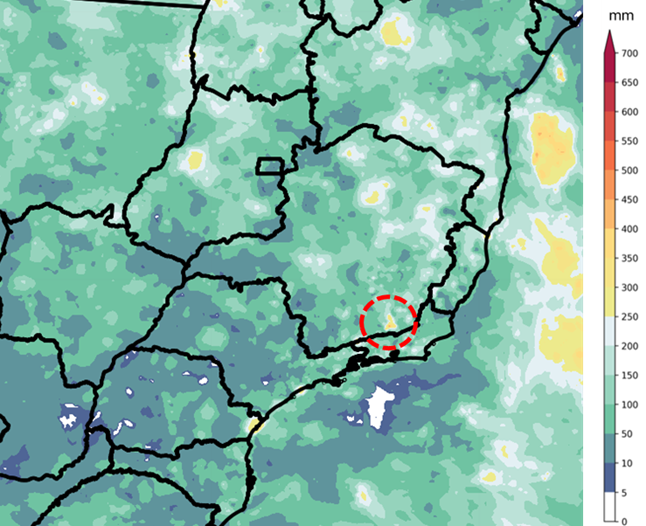

Colombia: In Colombia, torrential rains persist and may pressure differentials in the short term, exacerbating the already challenging scenario observed in January and February — a period when 30-day anomaly maps showed volumes well above average. Heavy rainfall has caused blockages, landslides, and erosion in production areas.

The 60-day anomaly maps indicate accumulations ranging from 60% to 100% above historical averages for the period across almost the entire country, harming flowering and, consequently, fruit formation in the coming months. The severity of the situation has prompted the government to implement emergency financial aid measures. The forecast for the next seven days suggests less intense rainfall, which may bring partial relief; however, there’s a risk of renewed intensity in the following week, requiring continuous monitoring.

For more details on historical data and forecasts for these countries, access the climate map dashboard.

Sector company results

Keurig Dr Pepper quarterly results

Last Tuesday (24), Keurig Dr Pepper (KDP) released its Q4 and full-year 2025 results.

- The company is one of North America’s largest beverage firms, with $16.6 billion in annual revenue.

- Within this total, the “U.S. Coffee” division, focused on domestic consumption via pods, generates about $4.0 billion annually.

Why it matters: Given its size and the widespread use of Keurig systems in the U.S., its figures provide valuable insights into domestic consumption behavior in one of the world’s leading coffee consumer markets.

- As a demand resilience gauge at the final chain stage, the company’s financial disclosures can also impact coffee futures prices.

Details: In 2025, the coffee division’s revenue remained stable, with slight annual growth (+0.6%).

- Volume decreased (-4.2%), but revenue did not drop proportionately, and the operation maintained operating margins above 30%.

- Revenue stability primarily resulted from a 4.8% price increase implemented by the company.

- For a business of this scale, the adjustment appears manageable. Consumers absorbed some price hikes, reducing volume slightly, but the consumption base did not experience structural deterioration.

- This trend continued in Q4 2025, with revenue growth (+3.9%) despite volume declines (-4.1%). During this period, the company reported an 8.0% price increase, explaining revenue growth despite lower sales volumes.

- Although the U.S. consumer market demonstrated resilience to price increases in 2025, with signs of improvement especially in the second half, the company’s results indicate that part of the sector still has room to recover higher volumes in 2026.

Luckin Coffee quarterly results

Market participants also monitored the release of Luckin Coffee’s Q4 2025 results on Wednesday (26).

- Founded in 2017, Luckin Coffee has become China’s largest coffee shop chain in terms of store count and one of the world’s largest in operational scale, closing the year with 31,048 locations.

- In 2025, total revenue reached approximately $7.0 billion, reflecting annual growth of 43%.

- The fourth quarter showed a 32.9% year-on-year revenue increase, while the active monthly customer base grew 26.5% compared to the same period last year, reaching 98.4 million.

Why it matters: Due to its operational scale and rapid expansion pace, Luckin’s figures provide direct insights into coffee demand in the world’s largest emerging consumer market.

- While China’s per capita consumption remains low relative to Western markets, it has one of the fastest structural growth rates.

- When a company of this size sustains robust growth in revenue, stores, and customer base, especially amidst recent volatility in coffee futures, it helps assess interpretations of global demand strength.

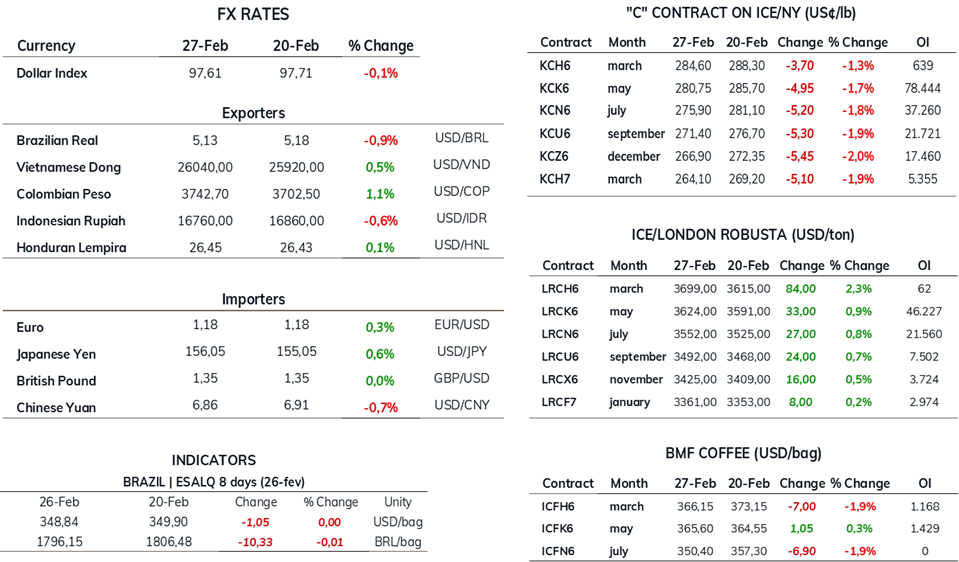

INDICATOR TABLE

Sources: ICE/NY; ICE/EU; B3; Commodity Network Trader’s Pro.