Copper Market Outlook 2026: Navigating a Changing Trade Landscape

WHERE WE ARE WITH COPPER PRICES AND WHY?

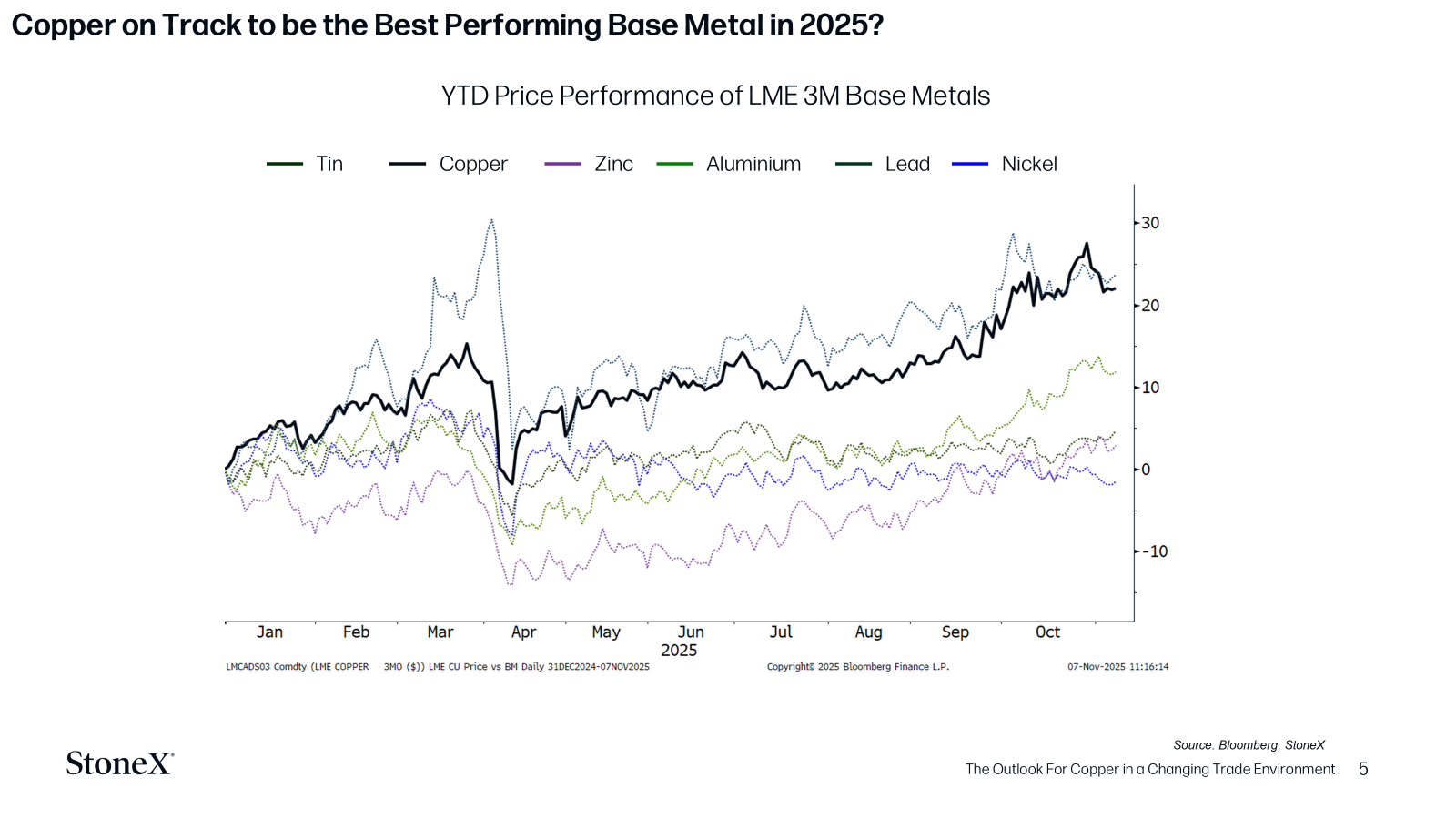

At the time of writing, copper is battling with tin to be the best performing base metal this year (+23%YTD). At first glance at the chart below, and taking into consideration tin’s usual price movements as being volatile given its small market size, this initially suggests that copper may be overvalued at its current level.

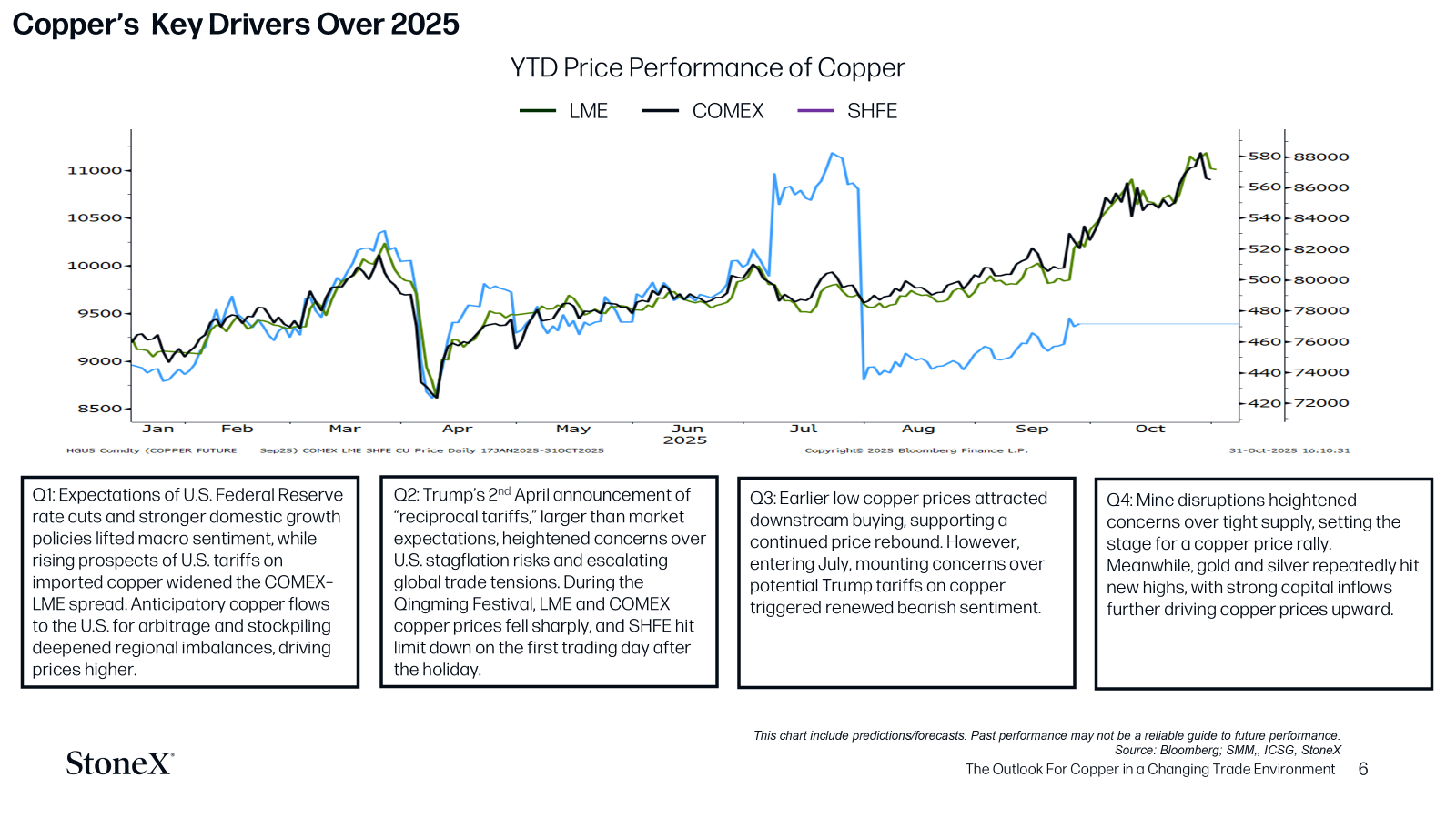

WITH THAT IN MIND, LET’S LOOK AT WHAT’S TAKEN US HERE?

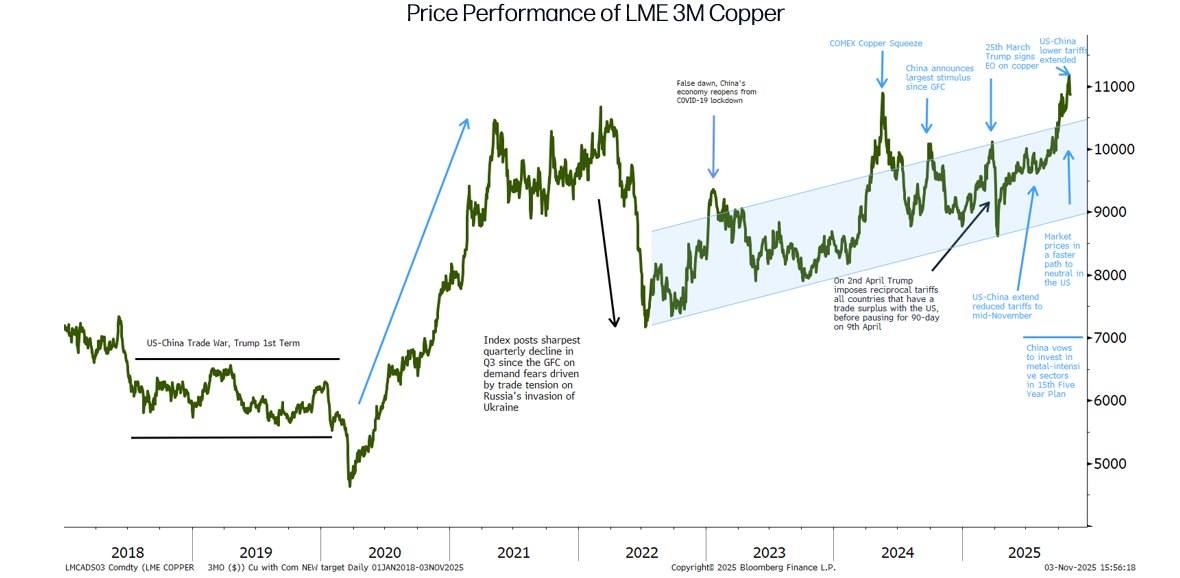

TAKING A STEP BACK AND LOOKING AT COPPER ON A EIGHT-YEAR CHART

Over the last three years, copper has formed a ‘new normal’ trading range of higher highs and higher lows. However, there have been several times in which copper has tried to break out to the upside, only to come back down into this range.

1. Start of 2023: China reopened from a year-long COVID-19 lockdown

2. H1 2024: during a copper squeeze on COMEX

3. September 2024: China announces its largest stimulus package since the GFC

4. March 2025: Following the aftermath of President Trump signing an Executive Order Investigation into US copper imports Under Section 232 of the Trade Act of 1962

At present, copper is once again trading above its three-year channel, driven by a ‘perfect storm’, with fundamental supply disruptions, a warming in the macro-economic outlook and investors favoring copper.

But the question everyone is asking = can this last?

In this presentation and written report, we will address the realities ahead for copper and how prices will be impacted by the outlook in the macroeconomic landscape, the fundamentals, tariffs and investors.

Source: Bloomberg, StoneX

UNDERSTANDING MACROECONOMIC DRIVERS IS CENTRAL IN FORECASTING FUTURE PRICE PERFORMANCE

There are five key area’s that we follow:

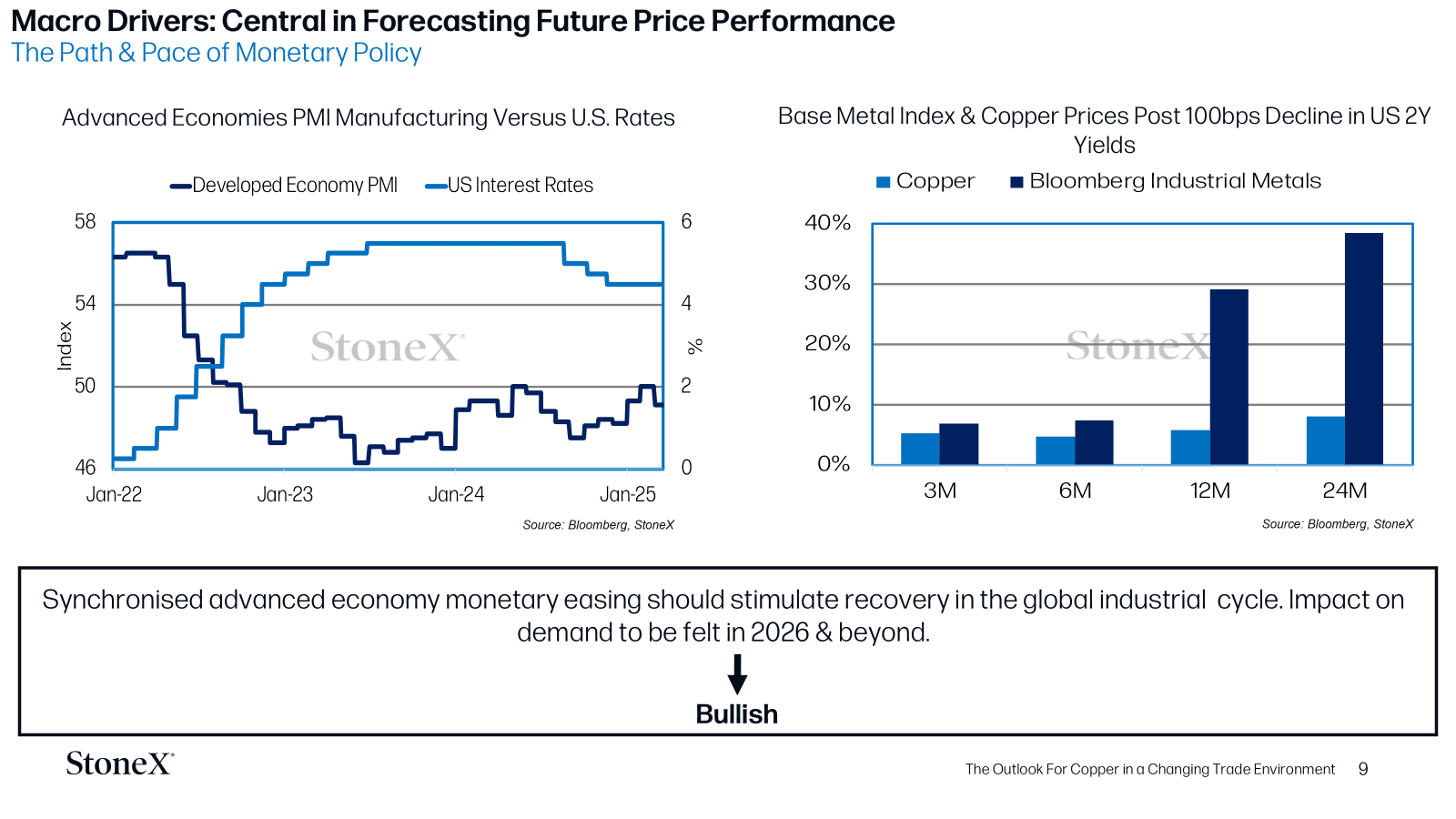

1. The pace and path of monetary policy

We see synchronized, advanced economy monetary easing as supportive for a recovery in the global industrial cycle, with falling yields as holding a net positive impact on copper. Here, while the path of monetary policy in the west has become more uncertain given the impact of tariffs, with its impact to inflation still being digested and the path of tariffs itself still highly uncertain. In our view, despite the pressure being placed on Federal Reserve Chairman Jerome Powell from President Trump to cut rates. We expect that the Federal Reserve will remain data dependent and continue to hold their dual mandate goal of balancing maximum employment and price stability in the country. We forecast ~100bps of rate cuts over the course of 2026.

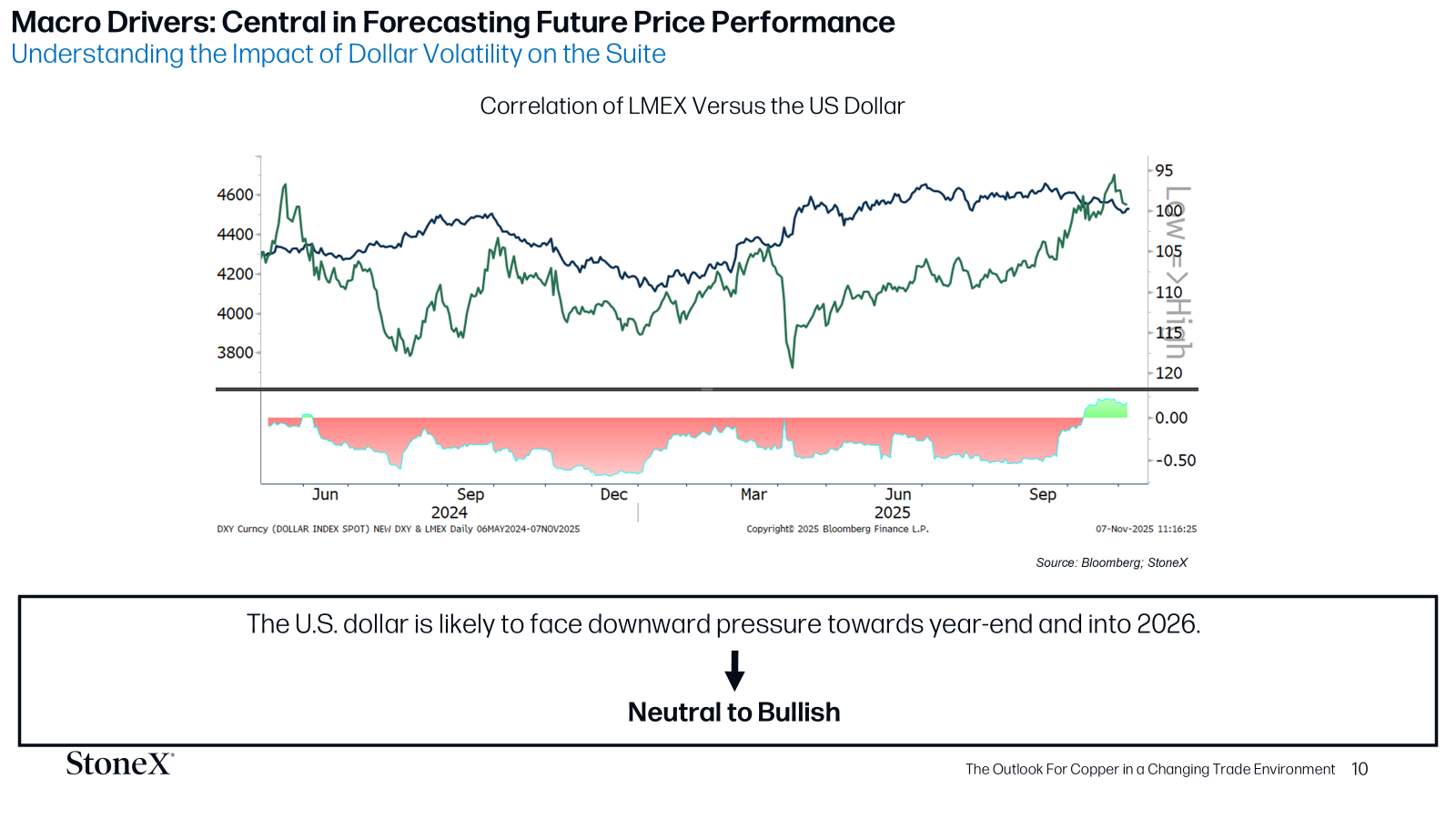

2. The Impact of the US Dollar

The US dollar historically holds an inverse relationship with copper, however, at present this relationship has turned positive, with copper prices instead taking its queues from fundamental and investor driven impacts. With this said, we see this as temporary, with dollar weakness over the year ahead on the back of a dovish Federal Reserve and waning foreign appetite for US assets supporting copper prices. Please note, we do not rule out a bouts of dollar strength, if global risk appetites shift or geopolitical tensions rise, with US dollar remaing the world’s key reserve and investment currency, lacking credible long-term alternatives.

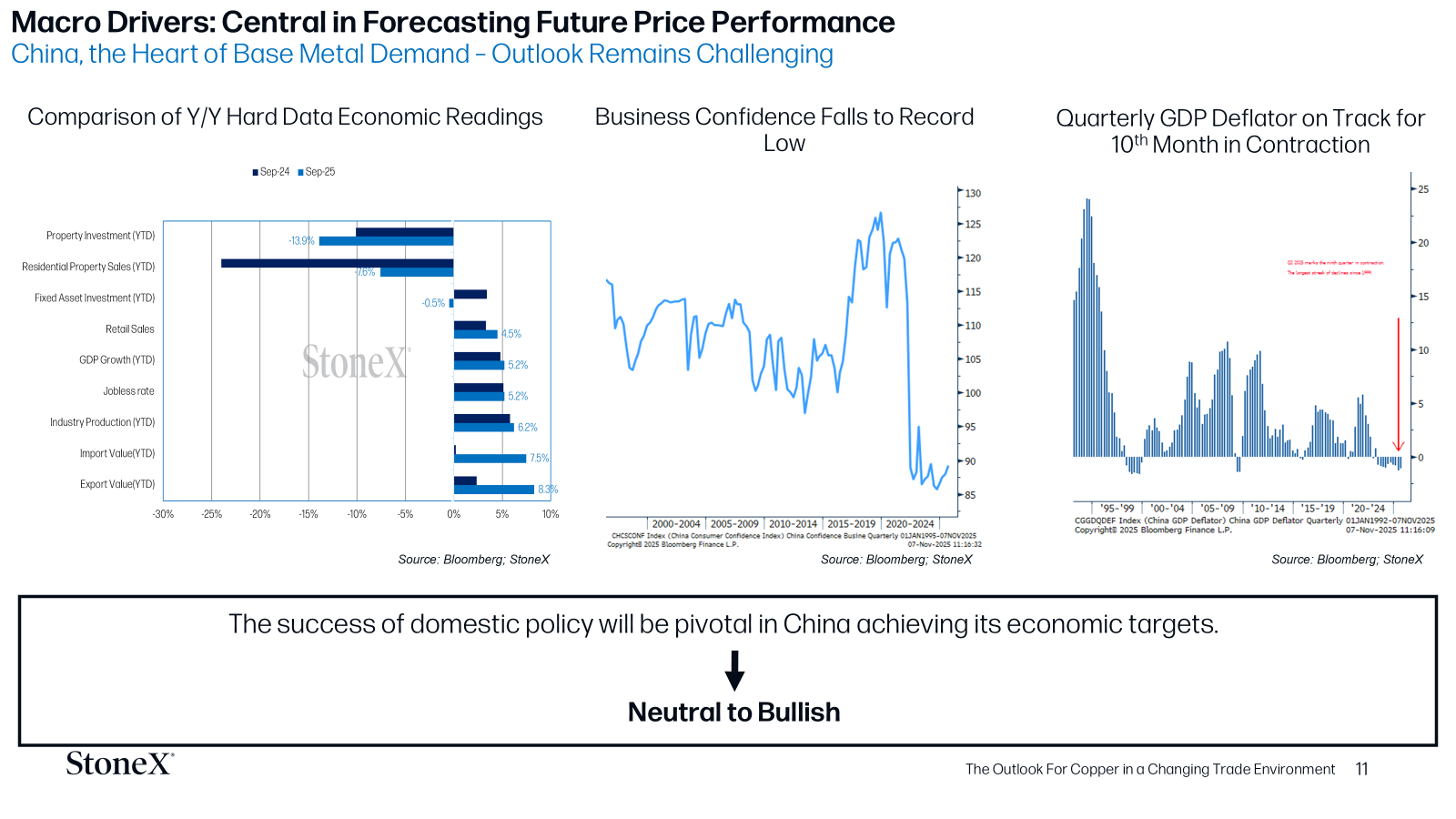

3. The Health of China

In our view, despite announced (and future expected) stimulus in the country over the next year, that will fall in line with China’s 15th Five Year Plan (starting in 2026), supporting investment into copper intensive areas such as advance industrial modernization and digital transformation. We forecast that the economy will face ongoing challenges in reaching its targets, especially given there were no announcements in the outline of the five-year plan that includes any ‘bazooka style' stimulus, instead signaling a phase of consolidation and stability rather than aggressive expansion.

While China appears on track to achieve its goal of ~5% growth in 2025, risks ahead are mounting from:

- deflationary concerns

- weakening investment demand

- record low confidence and consumer appetites

- deepening declines in the property market

In addition, anti-involution and tariff directives directly threaten the country's strongest growth areas of industrial production and exports.

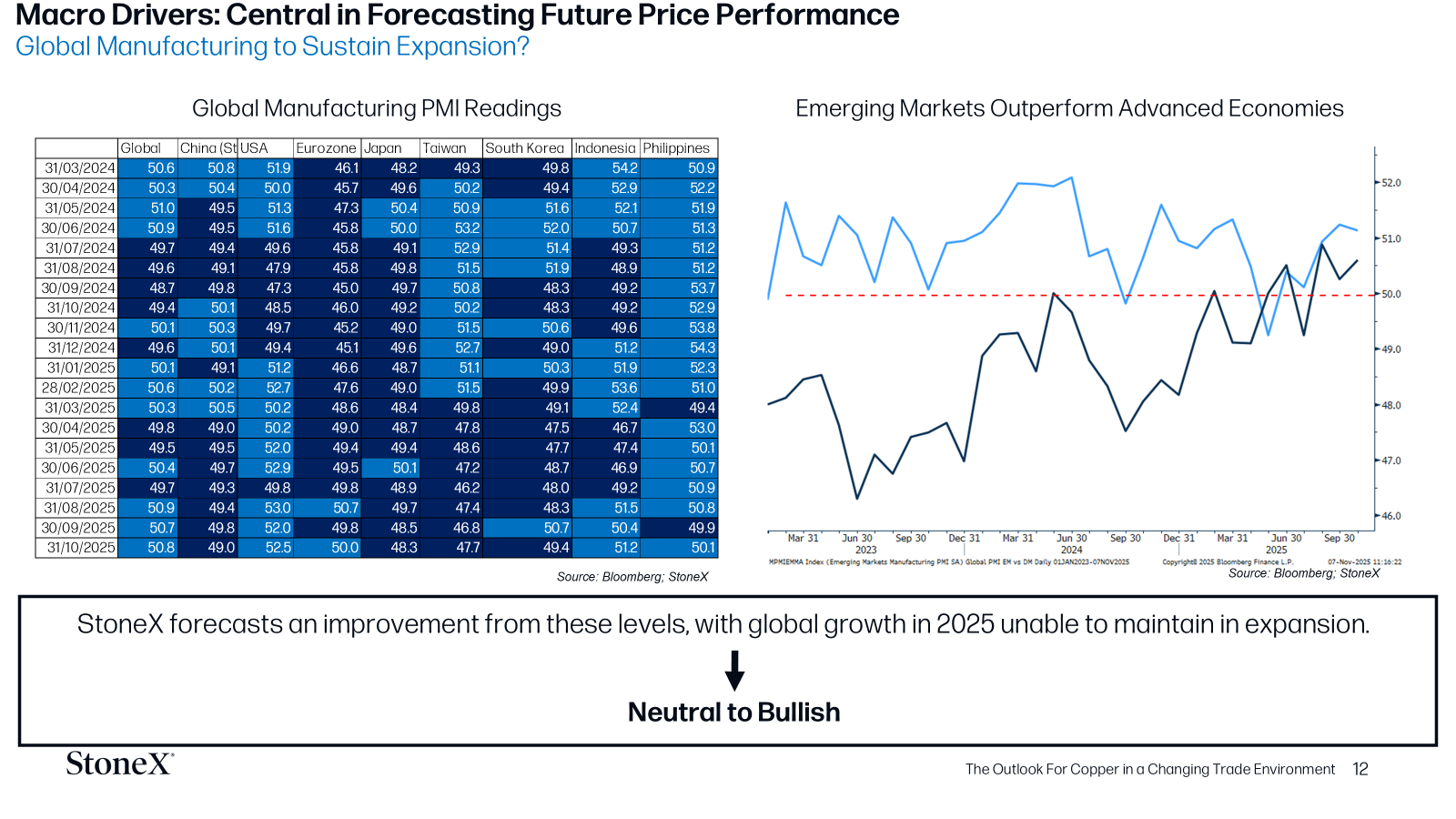

4. The Health of Global Manufacturing

We expect that global manufacturing should modestly improve from current levels, supported by:

- lower western interest rates

- stimulus efforts in China

- a general move towards an easing in trade tensions

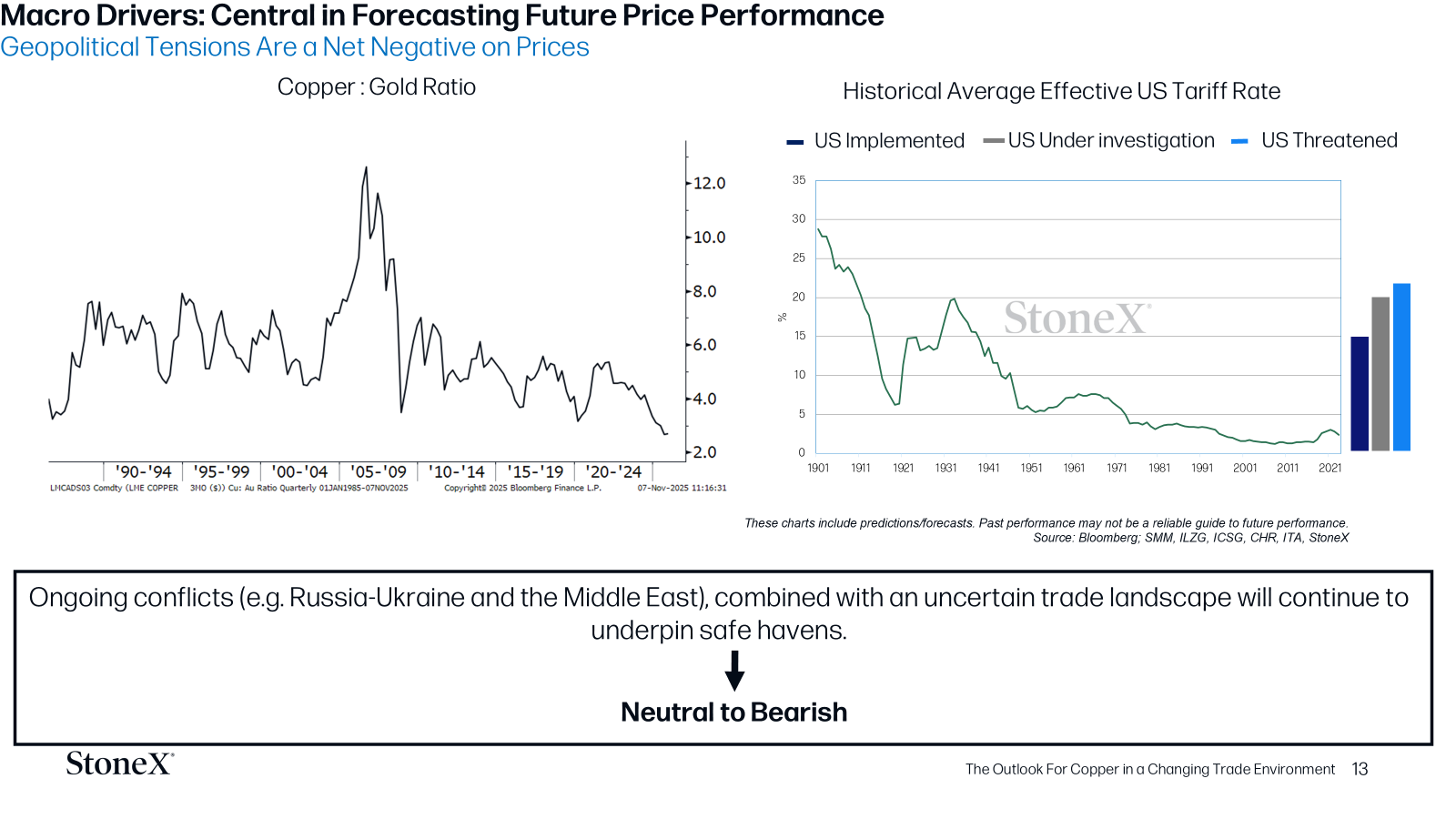

5. Weighing the risk of an escalation in ongoing or unknown geopolitical tensions

Geopolitical tensions can impact a commodity market in two ways:

- A risk channel: in which financial markets overestimate the impact on supply resulting in higher prices.

or

- An economic activity channel: Where a shock to economic growth creates uncertainty in investment and demand, leading to lower prices.

We see the addition of tariffs as playing a net negative for base metal demand in the longer-term.

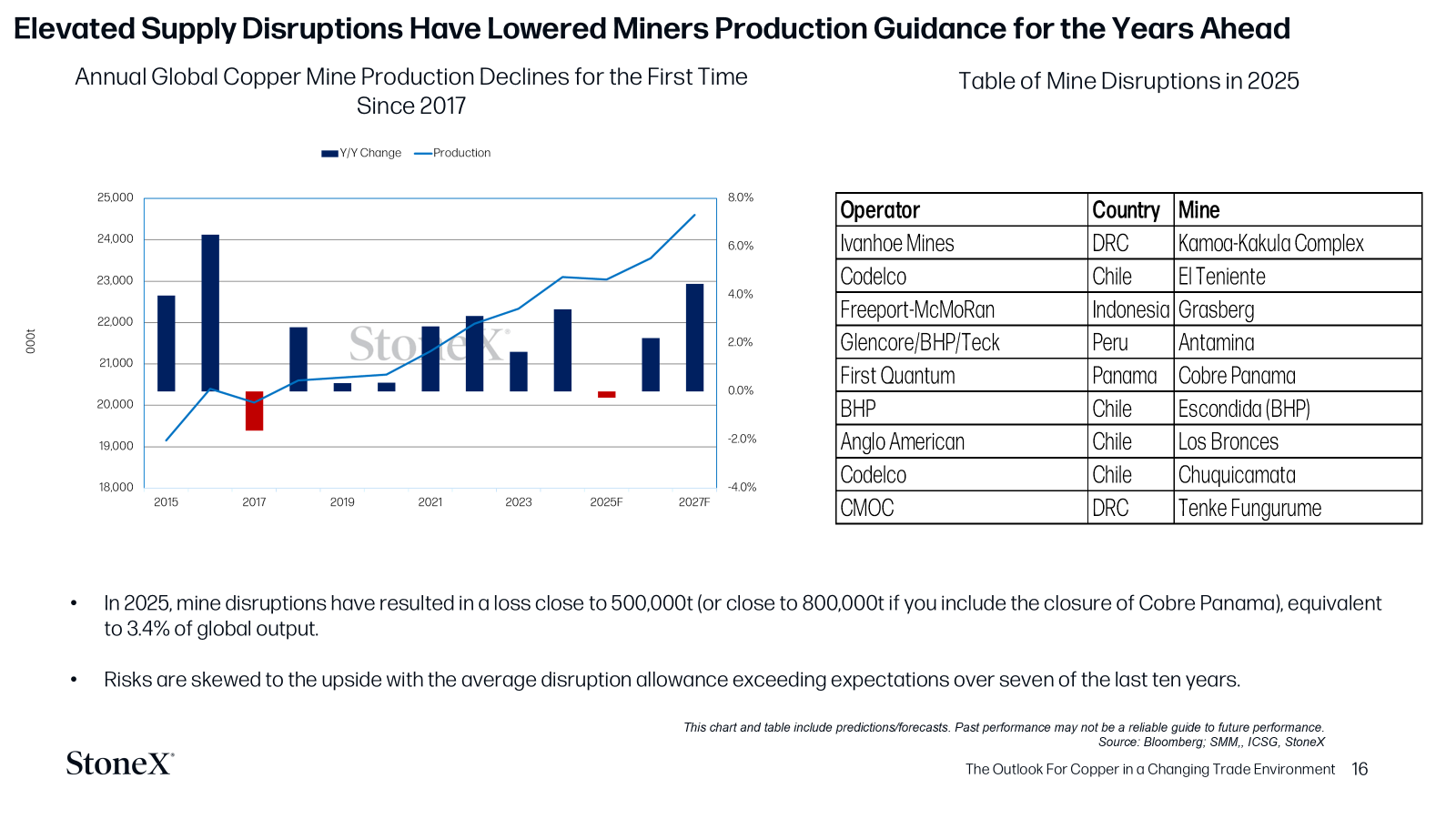

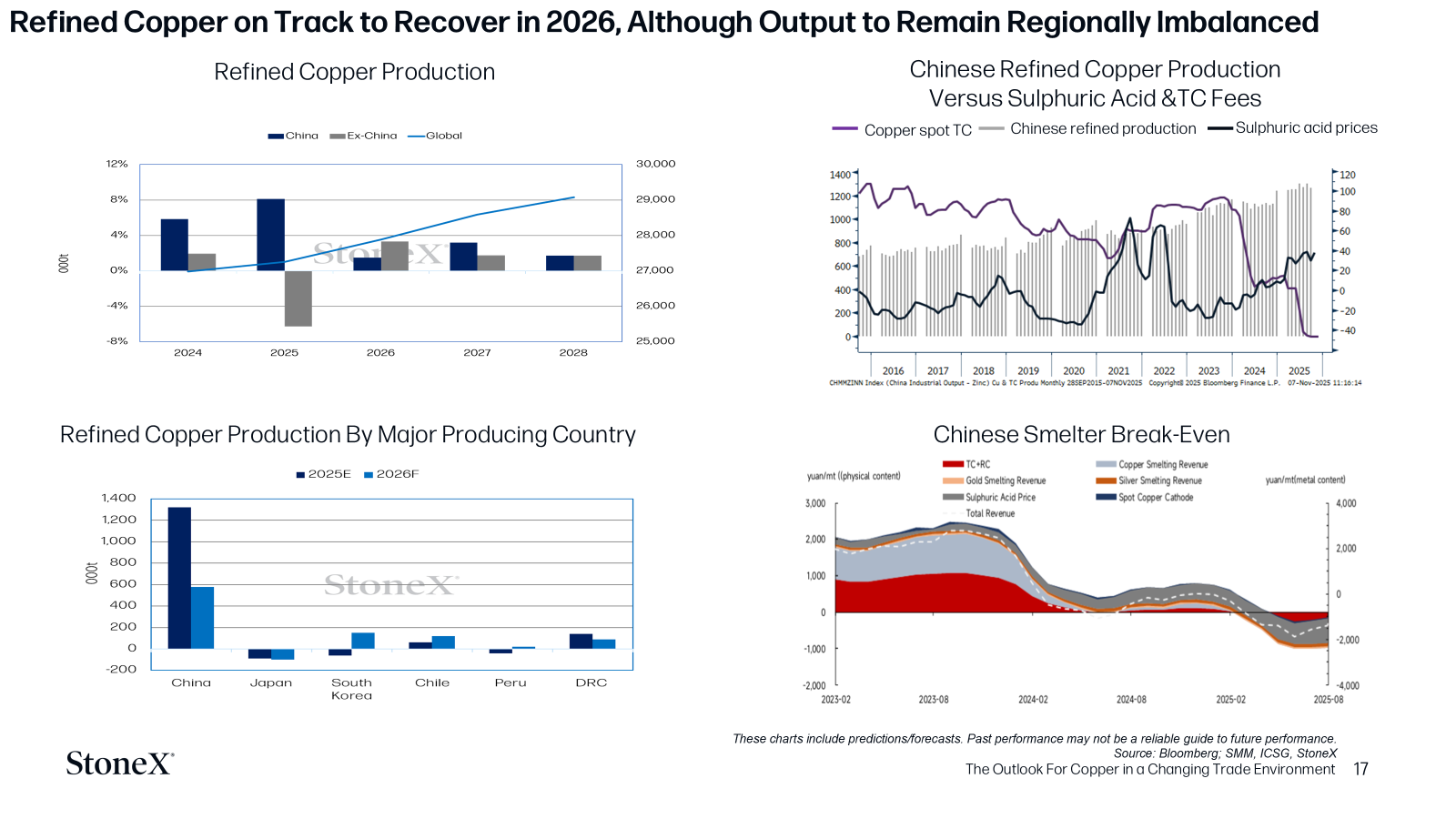

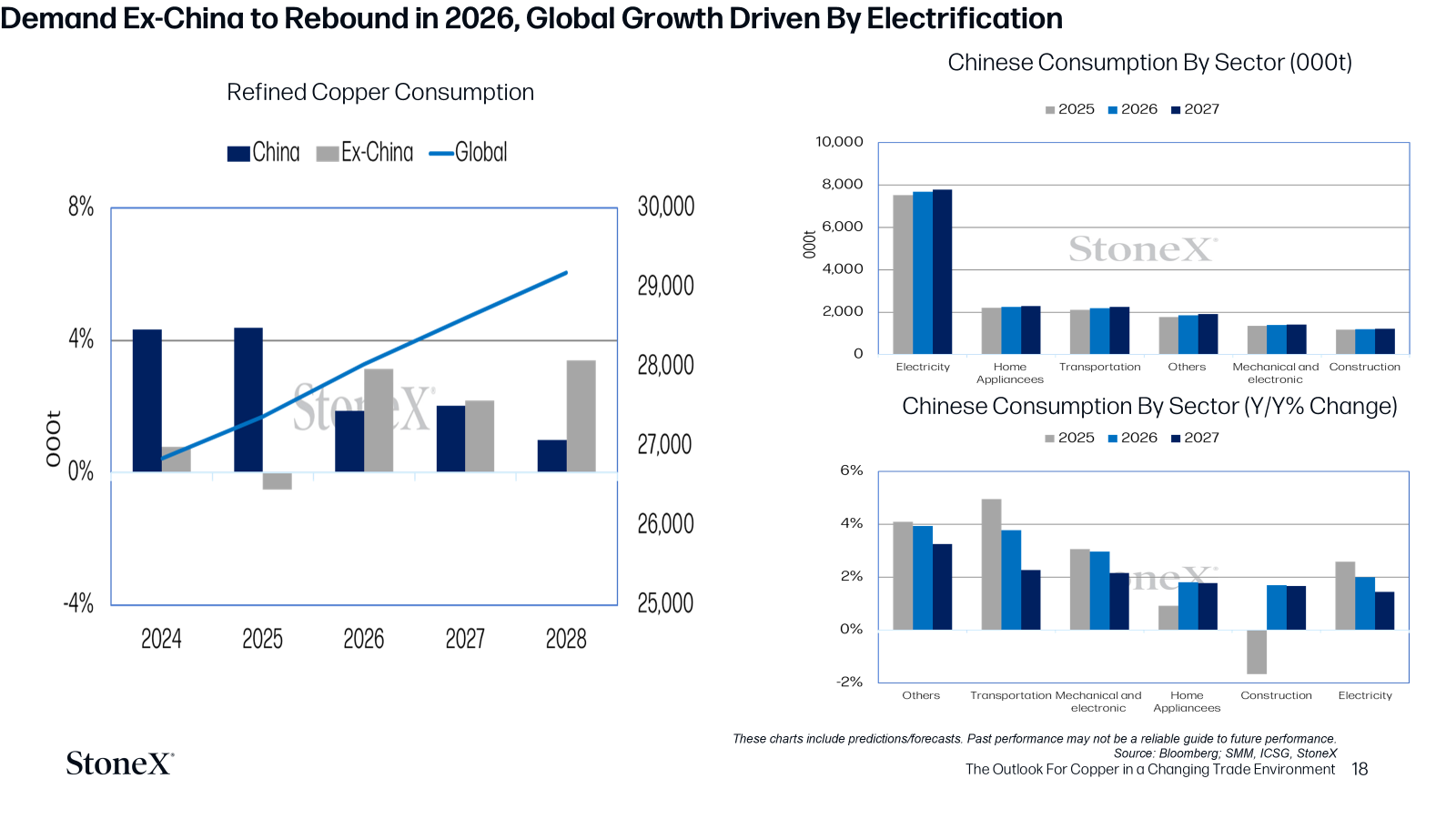

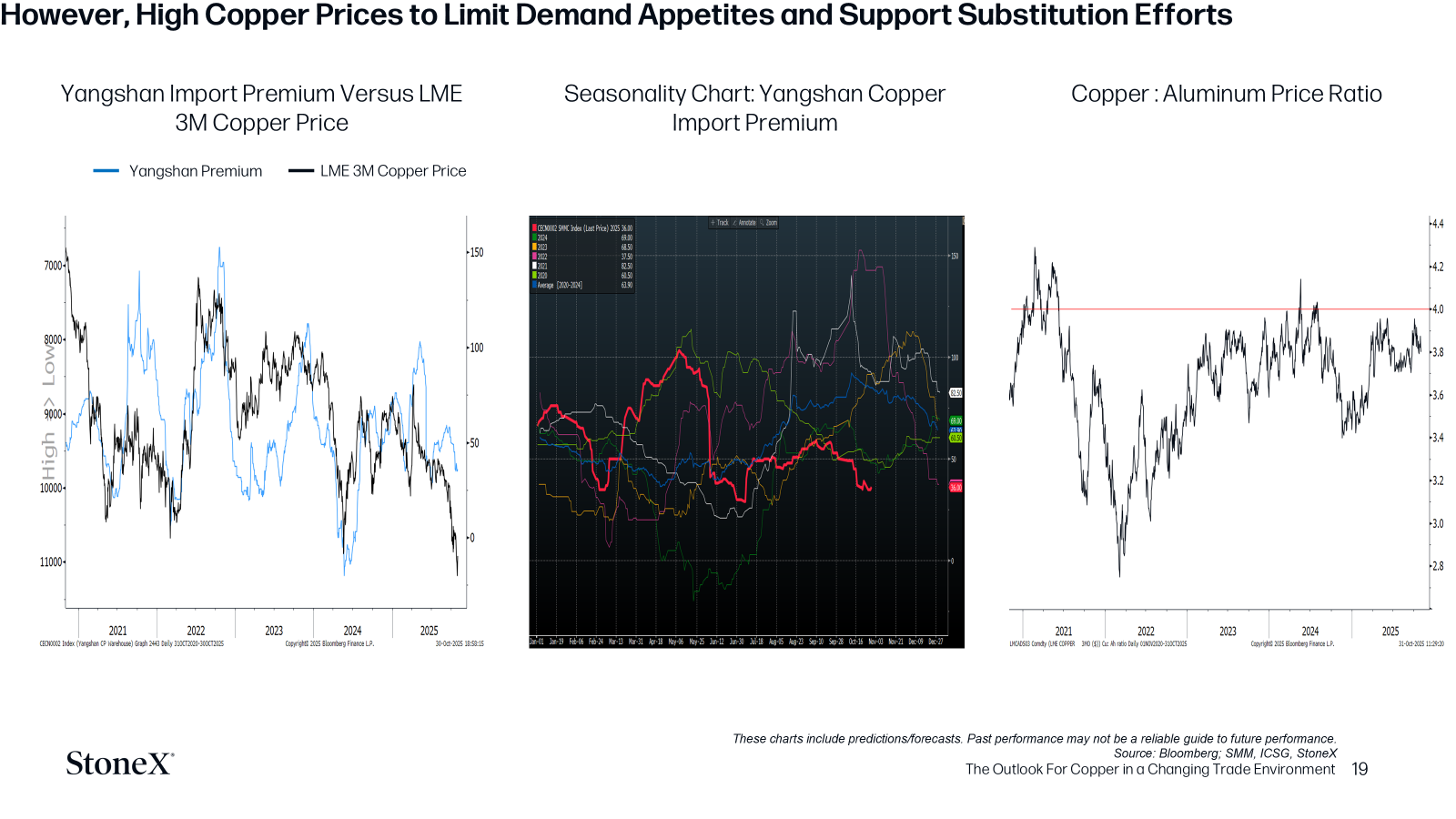

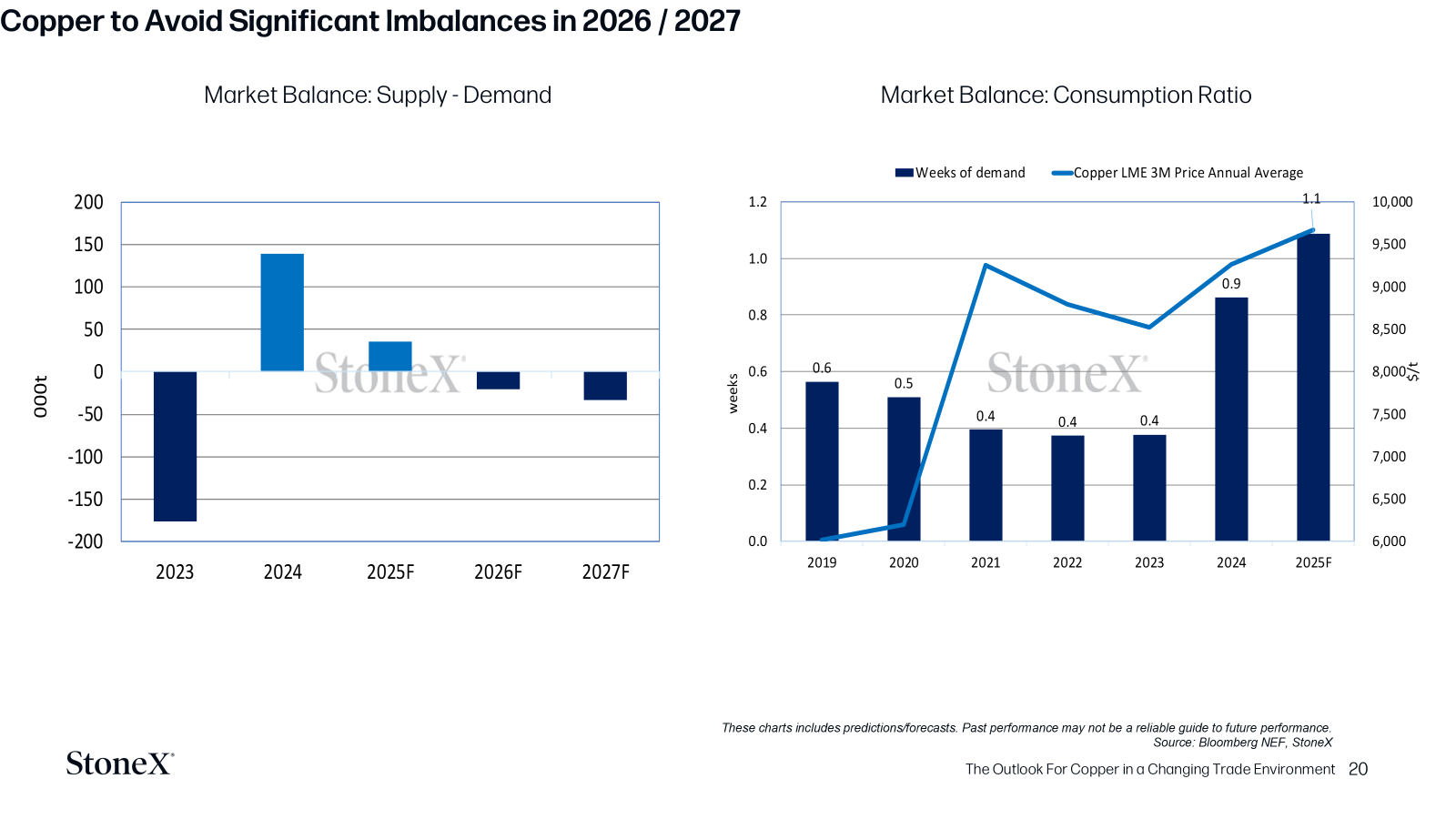

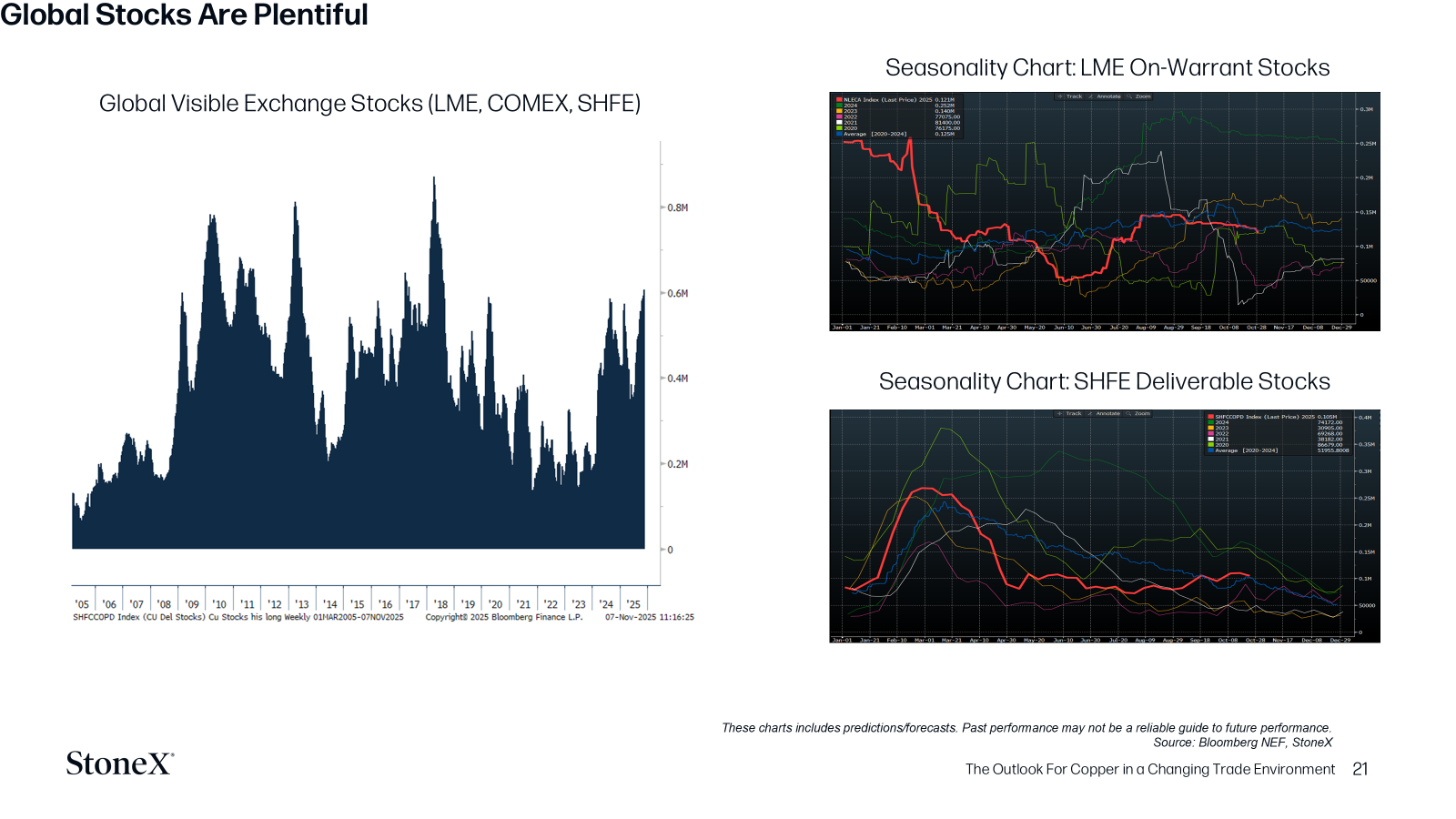

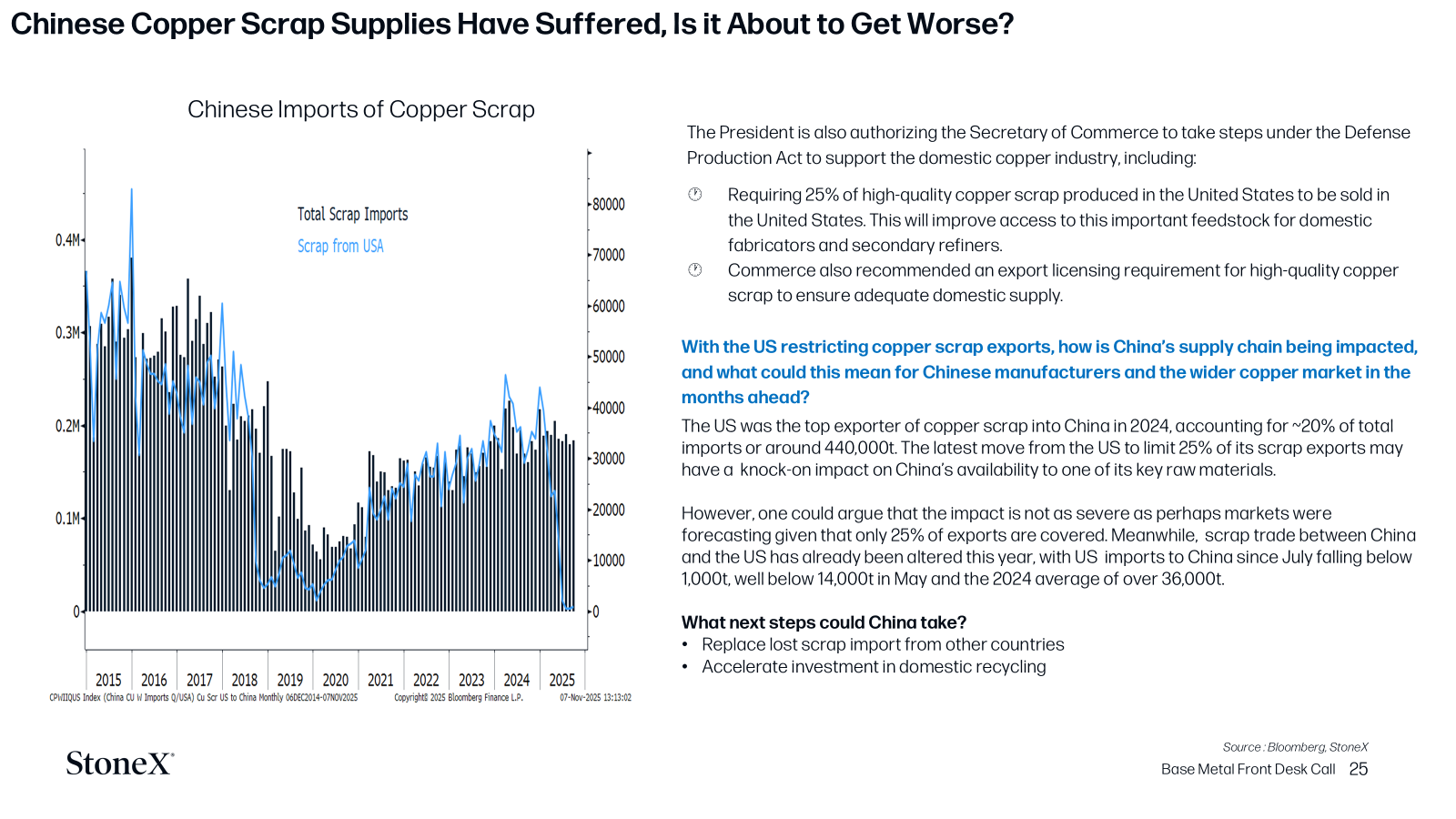

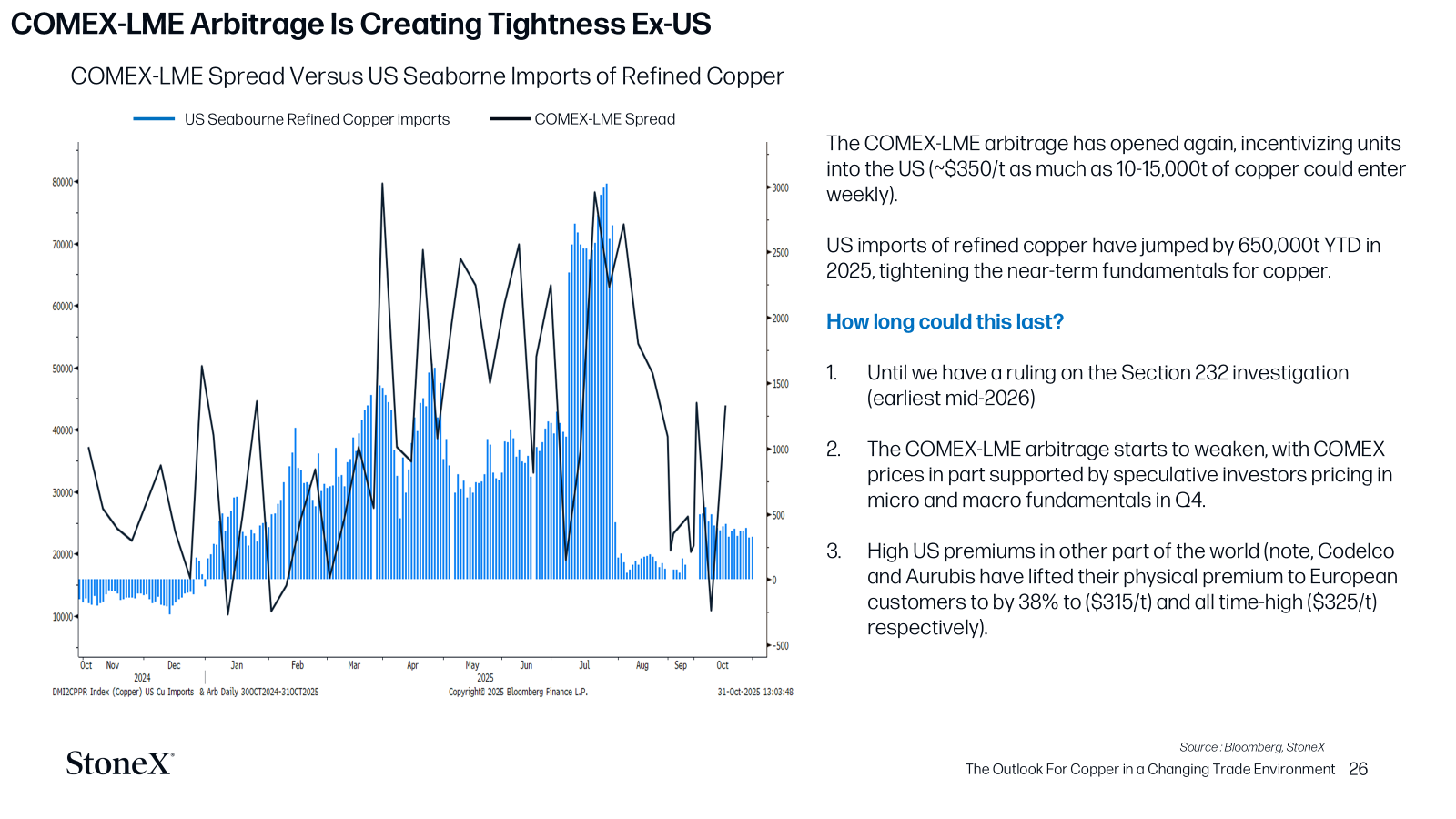

COPPER’S FUNDAMENTALS IN THE YEAR AHEAD

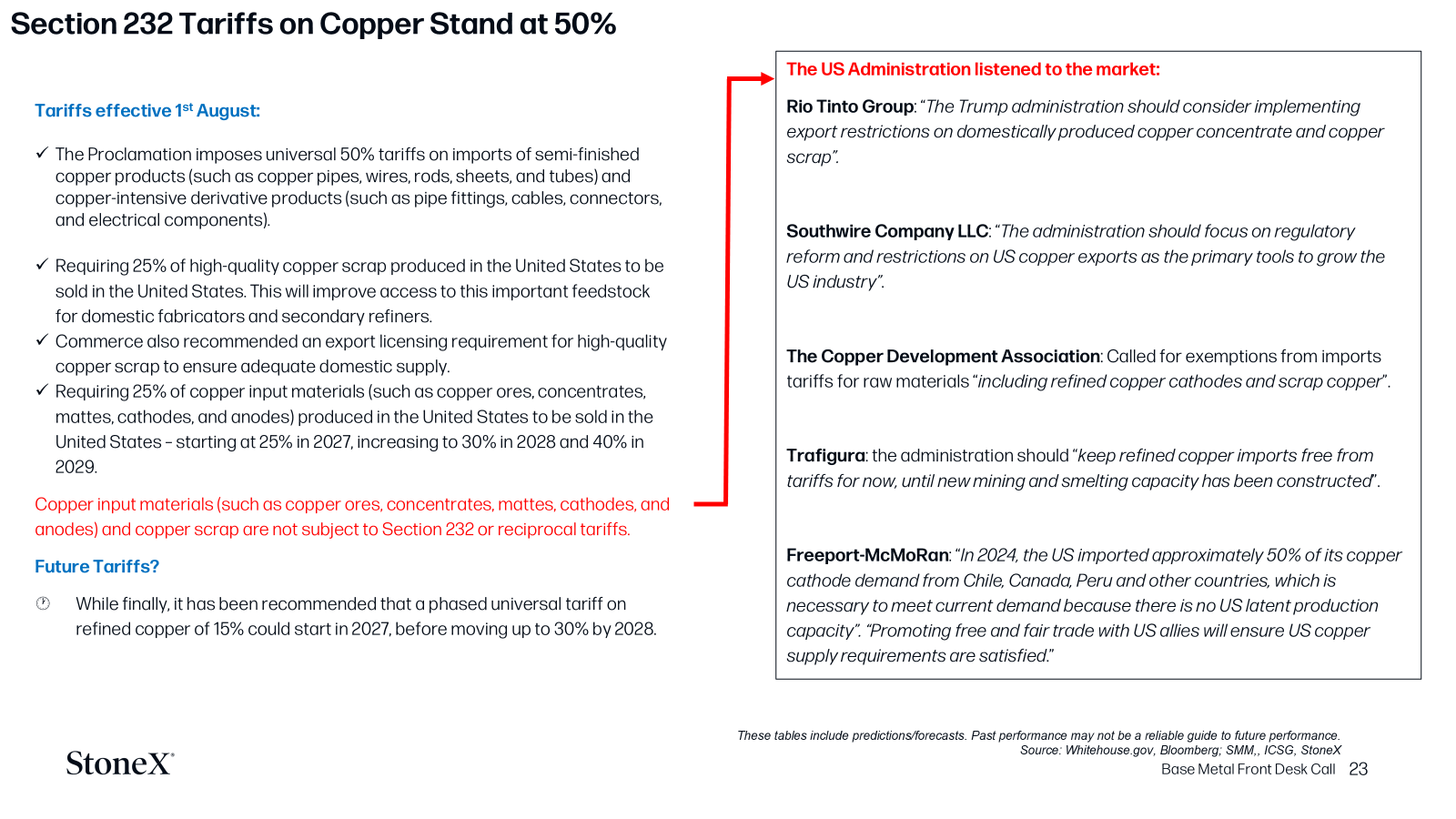

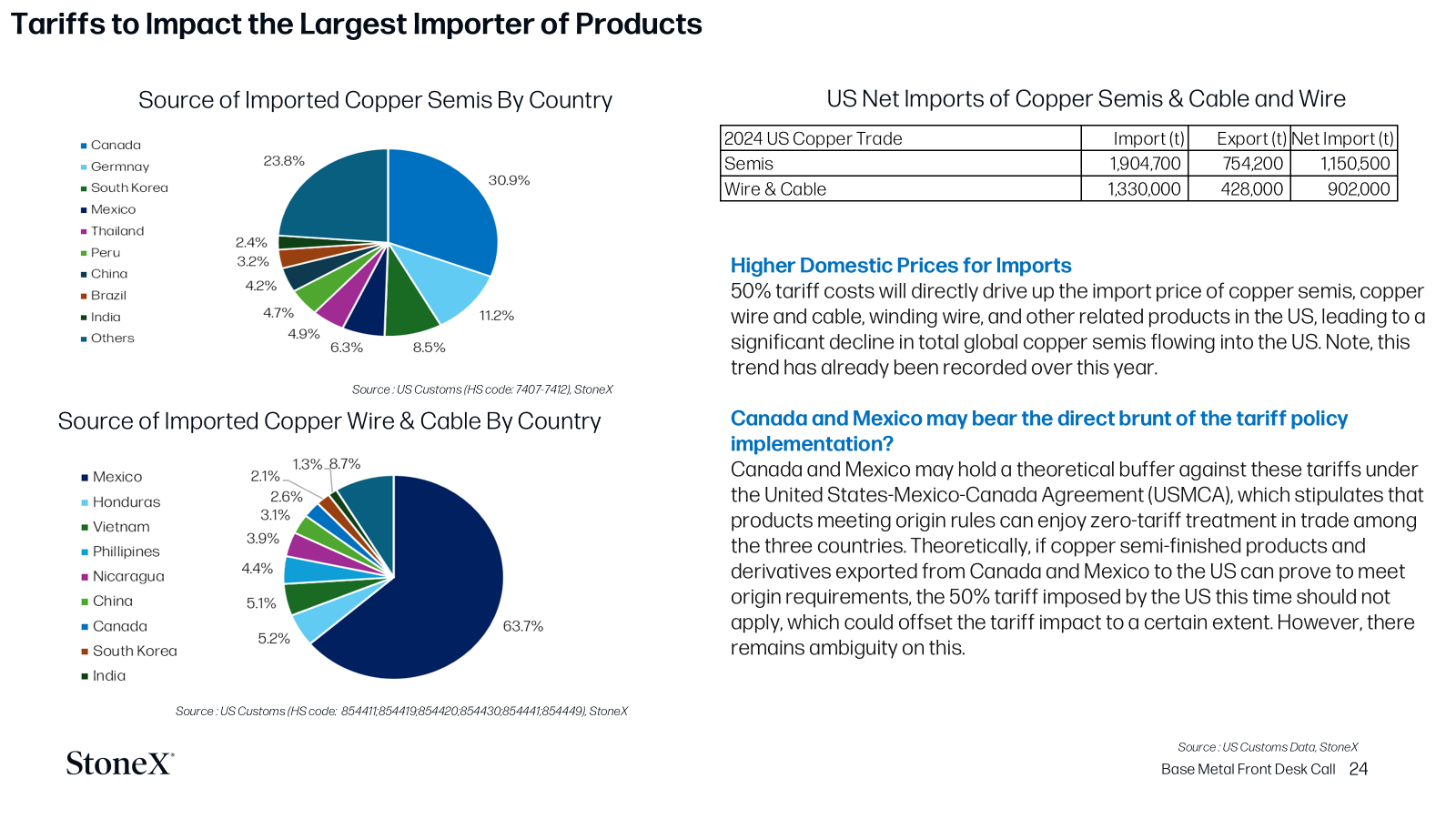

TARIFFS

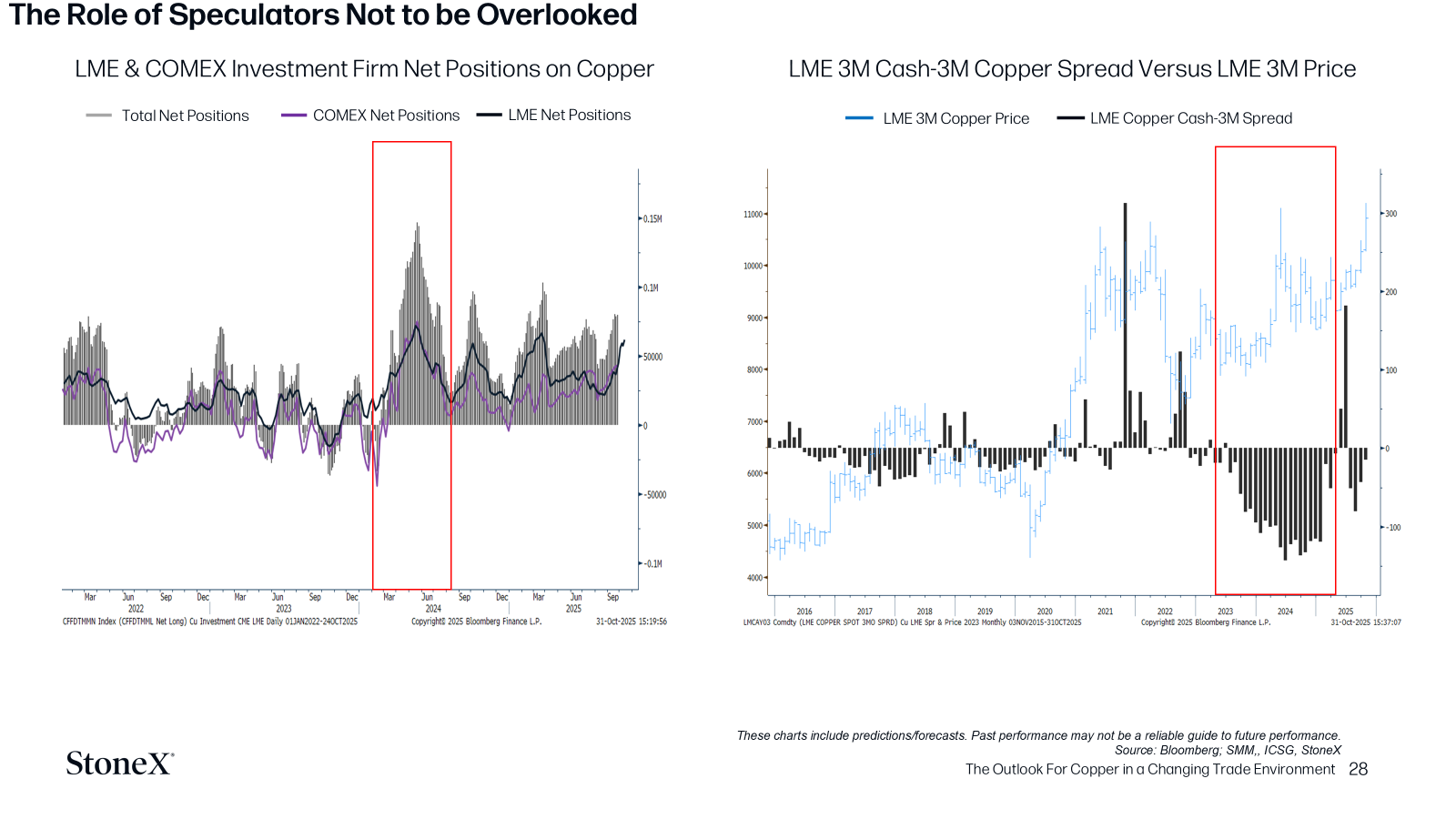

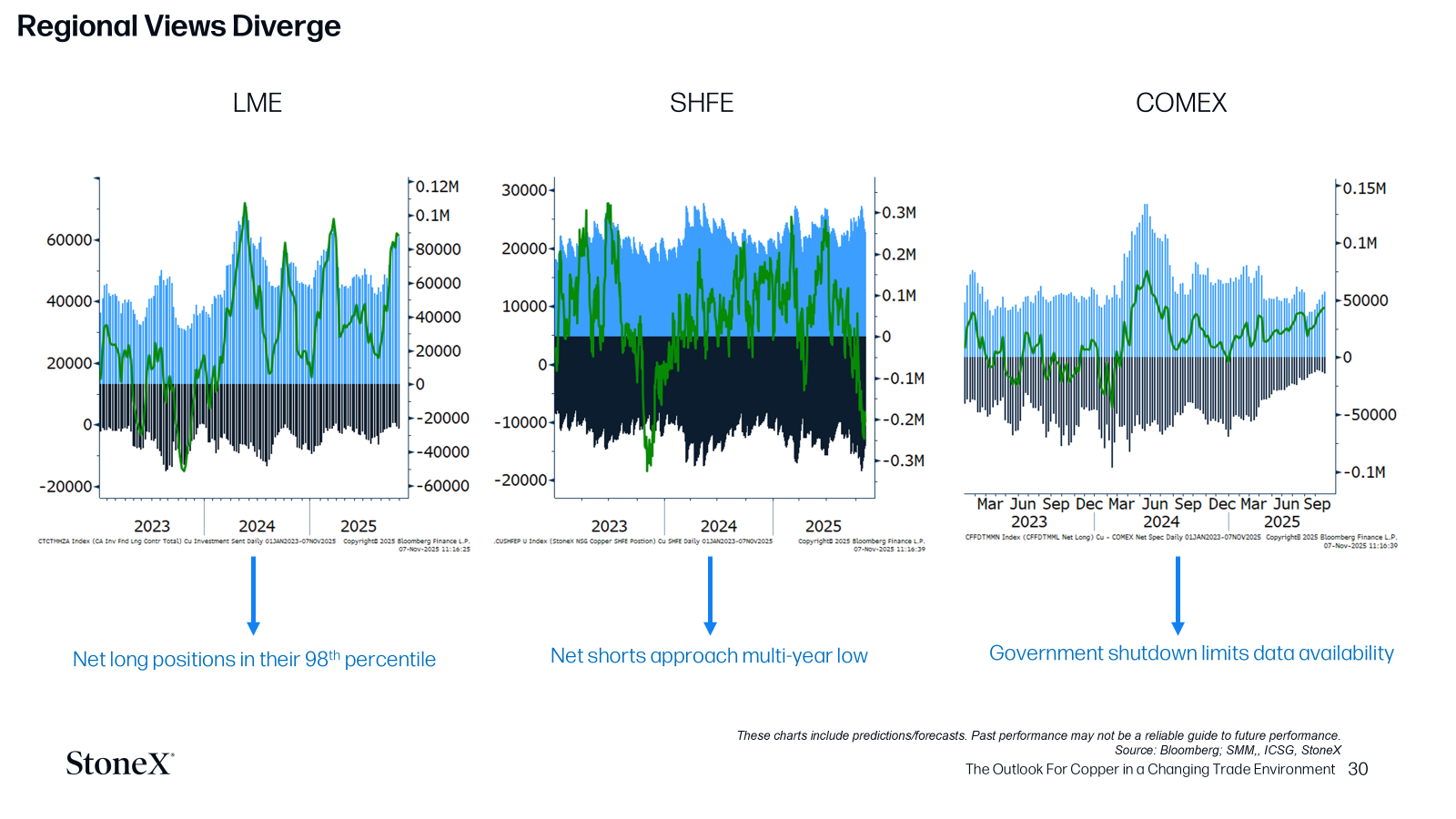

THE IMPACT OF INVESTORS AND SPECULATORS ON COPPER

The first thing to point out is, that the role of speculators and its impact on copper prices shouldn’t be overlooked given its ability to move pries away from either macroeconomic and/or fundamentals views.

The Classic example we have is H1 2024, in which investor interested soared into copper on the LME and COMEX exchanges, resulting in a squeeze on COMEX and a record nominal high on copper (for that time). The key takeaway here, is that during this period, we had record high copper prices, but historically wide contangos in the LME cash-3M spread. We have never seen prices this high, in a contango market, demonstrating the removal of copper price action from traditional price drivers.

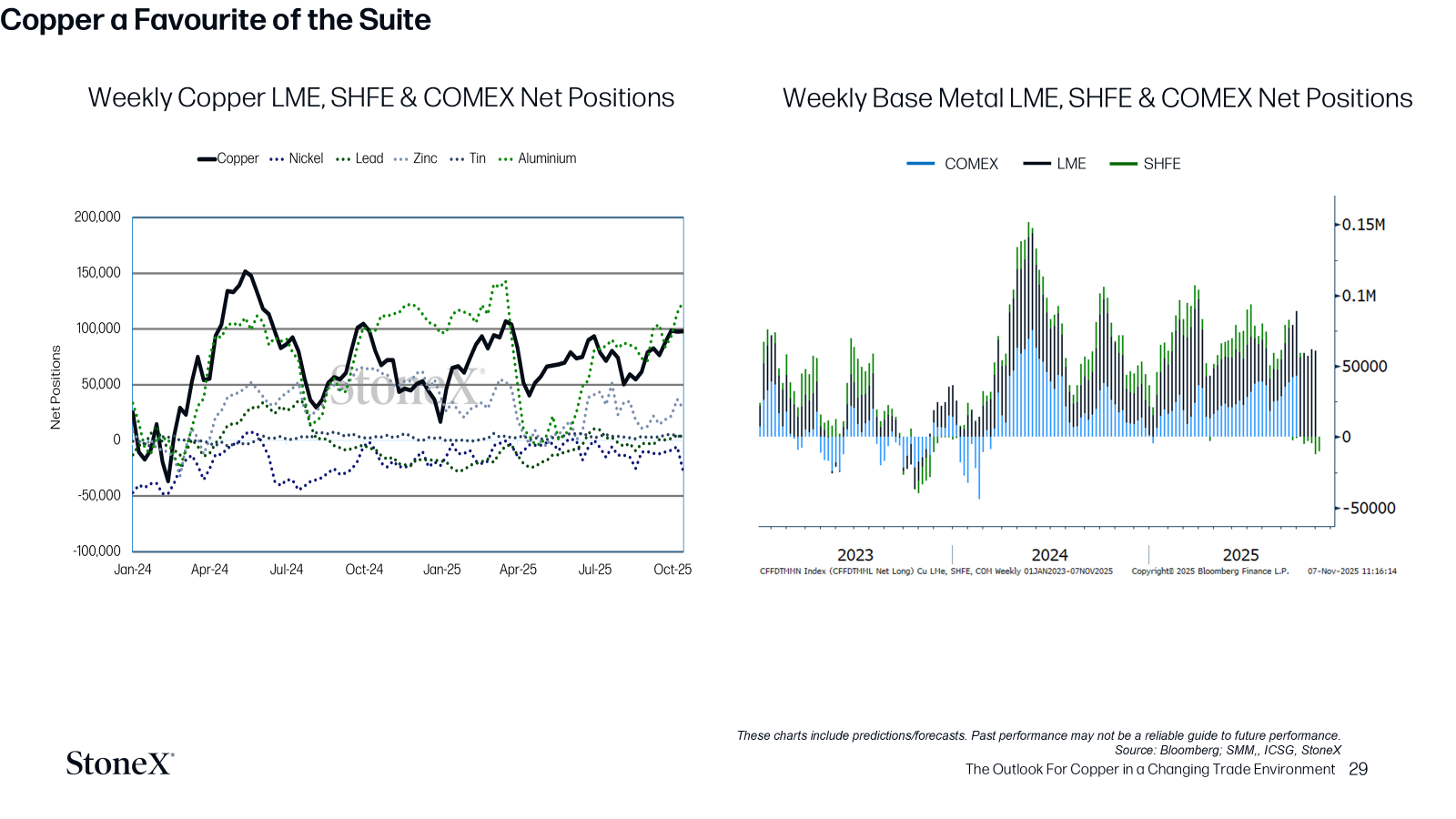

No surprise to see that copper remains one of the favorites of the suite underpinned by its long-term structural deficit outlook. And due to its use in electrification, copper is now seen as seen as a strategic alternative asset (not just a cyclical industrial commodity)

The global picture for copper is highly uneven, once again in our view reducing the argument for outright bullish themes for copper.

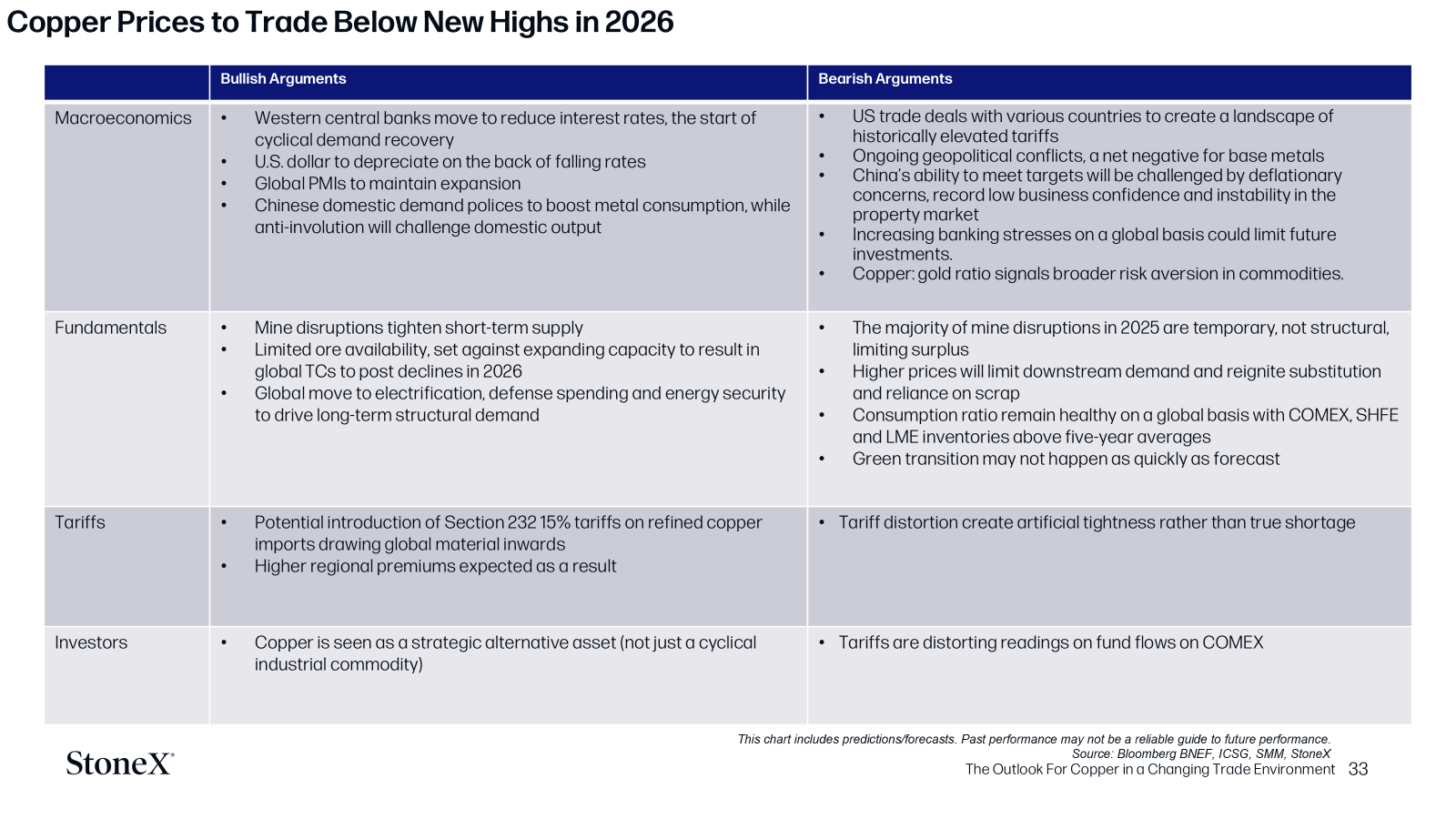

Copper Price Outlook

To year-end, copper prices are likely to remain elevated, underpinned by bullish themes:

Macroeconomics: warming momentum

- - China-US tensions have modestly eased

- - US Federal Reserve rate cuts

- - Expected announcements from China on its 15th five year plan

- - End of US Government shutdown

Fundamentals

- Market continues to digest supply disruptions and record low RCTCs

Tariffs

- Copper units are being drawn into the US on arbitrage opportunities

Investors and Speculators

- Riding on the themes above

However, we do not see a clear break higher being able to be maintained

With this in mind, our argument is – what would be the next big push for copper prices to hold above or maintain new highs in 2026?

Macroeconomics:

The majority of the warming in the outlook has already been priced in, meanwhile, risks to global growth are plentiful:

- Trade tensions could escalate again (especially between China and the US)

- Ongoing conflicts (Russian-Ukraine war, Middle East)

- Unlikely we will get bazooka stimulus in China in 2026

- Building concerns about global debt (Cu:Au ratio at lowest level on record)

Fundamentals:

- High copper prices negatively impact demand

- Chinese demand figures have been weak of late (disappointment over this year's and Golden September, Silver October)

- Outlook in major advanced economies remain tepid

- Copper market is relatively balanced

Investors:

- We may start to see long positions excited as a result of this and this is especially true if we see global visible inventory pick up (note, Q1 restocking period in China).

This material should be construed as market commentary and represents the opinions and viewpoints of the author, and does not reflect tailored advice associated with any specific account.

The views are current only through the date stated and are subject to change at any time based upon market or other conditions, and StoneX Group Inc. (“SGI”) disclaims any responsibility to update such views. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. Past performance does not guarantee future results.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided.

References to certain OTC products or swaps are made on behalf of StoneX Markets, LLC (SXM), a member of the National Futures Association (NFA) and provisionally registered with the U.S. Commodity Futures Trading Commission (CFTC) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ and who have been accepted as customers of SXM.

StoneX Financial Inc. (SFI) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (SEC) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Advisor. StoneX Financial (Canada) Inc. (SFCI) is registered in Canada and is a member of CIRO and CIPF. References to certain securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to certain exchange-traded futures and options are made on behalf of the FCM Division of SFI. Wealth Management is offered through SA Stone Wealth Management Inc., member FINRA/SIPC, and SA Stone Investment Advisors Inc., an SEC-registered investment advisor, both wholly owned subsidiaries of SGI.

R.J. O’Brien & Associates, LLC (RJO) is registered with the CFTC as a Futures Commission Merchant and is a member of NFA.

StoneX Financial Ltd (SFL) is registered in England and Wales, company no. 5616586. SFL is authorized and regulated by the Financial Conduct Authority (FCA) (registration number FRN:446717) to provide services to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorized to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorized and regulated by the FCA under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorized by the FCA.

This communication is issued in the European Economic Area by StoneX Financial Europe GmbH (SFEG). StoneX is the trade name used by STONEX GROUP INC. and all its associated entities and subsidiaries. StoneX Financial Europe GmbH (“SFEG”) is a securities trading firm registered in Germany under Company No. HRB 80844.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism. SAP is an “Approved International Trading Company” authorized to act as a “Spot Commodity Broker” under the Commodity Trading Act.

StoneX Financial Pte Ltd (Co. Reg. No 201130598R) (“SFP”) is regulated by the Monetary Authority of Singapore and is a Capital Markets Service Licence holder (for dealing in capital market products), an Exempt Financial Adviser (for advising on investment products and issuing or promulgating analyses/ reports on investment products) and a Major Payment Institution (for domestic and cross-border money transfer services).

SFP may distribute analysis/report produced by its respective foreign affiliates within the StoneX Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations Recipients should contact SFP at (65) 6309 1000 for any matters arising from, or in connection with, this webinar.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism.

StoneX Financial (HK) Limited (CE No.: BCQ152) (“SHK”) is regulated by the Hong Kong Securities and Futures Commission for Dealing in Securities and Dealing in Futures Contracts.

StoneX Financial Pty Ltd (ACN 141 774 727) holds an Australian Financial Service License (AFSL: 345646) for Dealing in Securities, Exchange-Traded Derivatives Contracts, OTC Derivatives Contracts and Foreign Exchange Contracts, and is regulated by the Australian Securities and Investments Commission.

StoneX Securities Co., Ltd. (“SSJ”) (Co. Reg. No 010401047199) is regulated by the Japanese Financial Services Agency as a Type-I Financial Instruments Business Operator (Kanto Local Finance Bureau (FIBO)No.291’), is a member of the Financial Futures Association of Japan for dealing and broking FX and FX Option transactions, and is a member of the Japan Securities Dealers Association for dealing and broking stock indices and option transactions.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

The report/analysis herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

© 2026 StoneX Group Inc. All Rights Reserved.