As we approach the conclusion of a positive 2023 for digital assets, one of the most dominant themes in crypto remains the potential approval of spot Bitcoin (BTC) ETFs. Below, we will delve into a brief history of the filing process, some of the remaining steps, logistics surrounding the trading of the product, and factors that could impact BTC price action upon potential final approval. Our base assumption is that there will be ETFs approved for trading in early 2024. While we anticipate volatility in the price action during the approval process, potential delays, and the initial launch, we hold the belief that the ETF will play a role in the long-term adoption of BTC. This could lead to a more extensive investor and user base, ultimately driving increased demand for the bitcoin asset.

How Did We Get Here?

The first filing for a BTC spot ETF came from the Winklevoss brothers, founders of the Gemini platform, on Jul 1, 2013, for the Winklevoss Bitcoin Trust. Since then, the SEC has denied their filing as well as all subsequent filings for such products. Over the years we have seen more than 20 ETF issuer firms try to launch a spot BTC ETF product, all of which have been withdrawn or rejected. That has not prevented the listing of similar products, such as the Grayscale Bitcoin Trust (ticker: GBTC). GBTC was initially launched as a private, open-ended trust for accredited investors in September of 2013. The trust vehicle trades OTC and attempts to offer indirect ownership of BTC. Because the trust does not offer a redemption feature, it has traded at a material variance to the Net Asset Value (NAV) of the underlying trust holdings of BTC. In the early years of its trading, GBTC represented one of the few ways investors could access exposure to BTC price movements, without owning spot BTC. This led to a significant premium of GBTC price to NAV. At its highest point in June 2017, GBTC was trading at over +132% premium to the value of its underlying holdings, creating an arbitrage opportunity which would later come to hurt many of crypto’s early institutional players. Over time, this premium eroded into a meaningful discount to NAV as the lack of redemption facility, turmoil in the industry and poor price action left holders stuck holding the asset. The trust currently owns ~620,000 BTC currently valued at over $26B, but the trust is still trading at ~10% discount to that value. As time passed, Grayscale had tried to convert its trust into an ETF, which would unlock that value from its discount to NAV (-45% at its lowest point in Dec 2022). On June 29th, 2022, Grayscale filed a lawsuit against the SEC calling its continued rejection of the conversion “arbitrary, capricious, and discriminatory.” Part of their argument rested on the fact that the SEC had previously approved trading of a futures-based ETF, the ProShares Bitcoin Strategy ETF, in October of 2021. It would be the outcome of this lawsuit that would spur the 2023 flurry of filings that are coming due soon.

The Stage Is Set

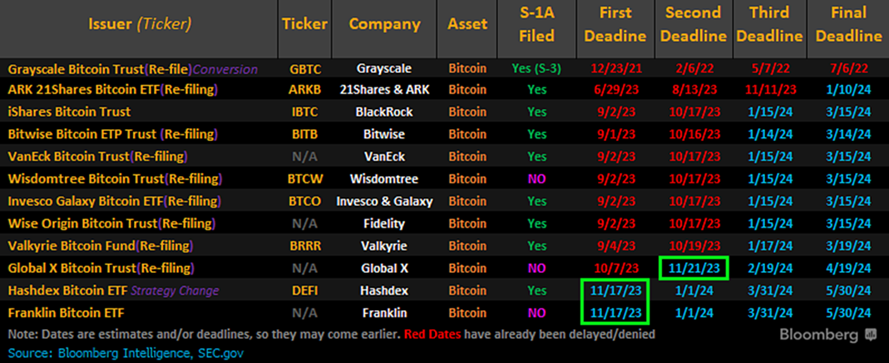

On Aug 29th, 2023, the court ruled against the SEC, saying they were wrong to reject Grayscale’s attempts to convert its trust to an ETF, and forced them to review the Grayscale application in light of this. Since then, many of the largest ETF issuers, including Blackrock, Van Eck, ProShares, Bitwise, Valkyrie and others, have re-filed their applications for spot ETF products. These subsequent filings have incorporated the court decision as well as evolving SEC discussions, aiming for final approval to launch the products. According to public records, the SEC has been engaging with these issuers increasingly, with some issuers meeting with them multiple times in the last week alone. As of now, the current schedule for potential approvals has Jan 8-10 as the next potential window. This is based on both the Jan 10 final deadline for the ARK ETF as well as early deferrals for Franklin and Hashdex on 11/28/23 – which sets their next deadline in the Jan 8-10 timeframe. Those had both been deferred just 11 days earlier on 11/17/23.

This aligns with the timing of previous re-file requests from the SEC, aiming to coordinate a date for multiple approvals.

Important Note: We should point out that the launch process here requires two filings to be approved. The first is the rule change under Sec 19b-4 to allow for the listing of shares as Commodity-based shares. The second filing is the S-1A registrations, which will need to be deemed effective by the SEC. This creates the potential for the approval of the ETF, but not necessarily the launch of trading. There could be a window between blanket rule-change approval (Jan 10th) and the actual launch of any of the issuer ETFs.

What Are the Issues and Other Considerations

The logistics of a BTC ETF product differ from prior ETFs primarily due to the nature of the underlying asset. While other ETF products have underlying assets that are traded on US securities or commodities exchanges and traded by regulated broker dealers and FCMs, spot BTC does not have a specific regulated US exchange. More importantly, entities regulated by the SEC and CFTC, and more broadly, the Fed and OCC, are generally unable to trade spot BTC. This creates a logistical issue in the creation of the ETF. Typically, ETF issuers engage Authorized Participants (“APs “) in the creation/redemption process, requiring APs to handle underlying assets. Recent conversations between issuers and the SEC have focused on this issue within the workflow. Media reports have suggested that the SEC prefers cash redemptions versus in-kind redemptions. While unable to discern the exact issue the SEC has with in-kind redemptions, where spot BTC is delivered to the redeemer, we would note that taking delivery of BTC would require specific custodial wallet infrastructure. This raises the question about whether the SEC inadvertently endorses the broker-dealer community trading spot crypto if they allow in-kind redemptions? Perhaps they do not want to open that pandora’s box just yet. Cash delivery, on the other hand, would only require a traditional prime brokerage account. Additionally, it has been speculated that taxes may play a role in this preference, considering the historical complexity of collecting taxes on crypto transactions for US governing bodies.

In our view, there is an additional layer of complexity to the creation/redemption process – a duration mismatch in the settlement of the underlying asset and the ETF security. When traditional security-based ETFs are created, the underlying securities transactions will settle at the same time as the delivery of the ETF and the cash to settle those transactions. Crypto is a T-0 settlement asset, whereas ETFs are a T+2 settlement asset. Crypto market makers (“MMs”) will have a mismatch in transacting the crypto (and paying for the crypto) on the same day as instructed, while potentially not receiving the funds to settle their delivery of the crypto to the AP for 1-2 additional days. This introduces both balance sheet and funding considerations when the crypto MMs are transacting on behalf of the issuers.

Finally, we would highlight the issues surrounding the reference rate chosen to set the 4:00pm Est Net Asset Value. As ETF issuers strive to transact as close to the 4pm reference rate as closely as possible to reduce slippage costs. The selected rate and its construction methodology can significantly impact price action around the 4pm NY close. To mitigate the risk of executing large amounts of BTC at exactly 4pm, reference rates with a smoothing function are likely to be preferred. Our conversations point towards the CME CF Bitcoin Reference Rate – New York Variant (BRRNY) as a potential reference rate (Link). This rate is a 1-hour TWAP created using twelve 5-minute periods between 3:00-4:00pm ET, utilizing trade data (price and size) from various exchanges. While the use of a reference rate like the BRRNY should help smooth end of day volatility, we do not expect it to eliminate the potential for dislocations around 4pm.

That’s All Great, But What Does It Mean for the Price of BTC?

Much has been discussed regarding the potential impact of a spot-based BTC ETF on the short and long-term price of Bitcoin. We would be foolish to prognosticate specifically on price action; however, there are some significant variables we would point out as investors try to look into the future price of BTC. The price of BTC has appreciated significantly this year (+151%), and one could argue ETF approval has been a factor in its rise.

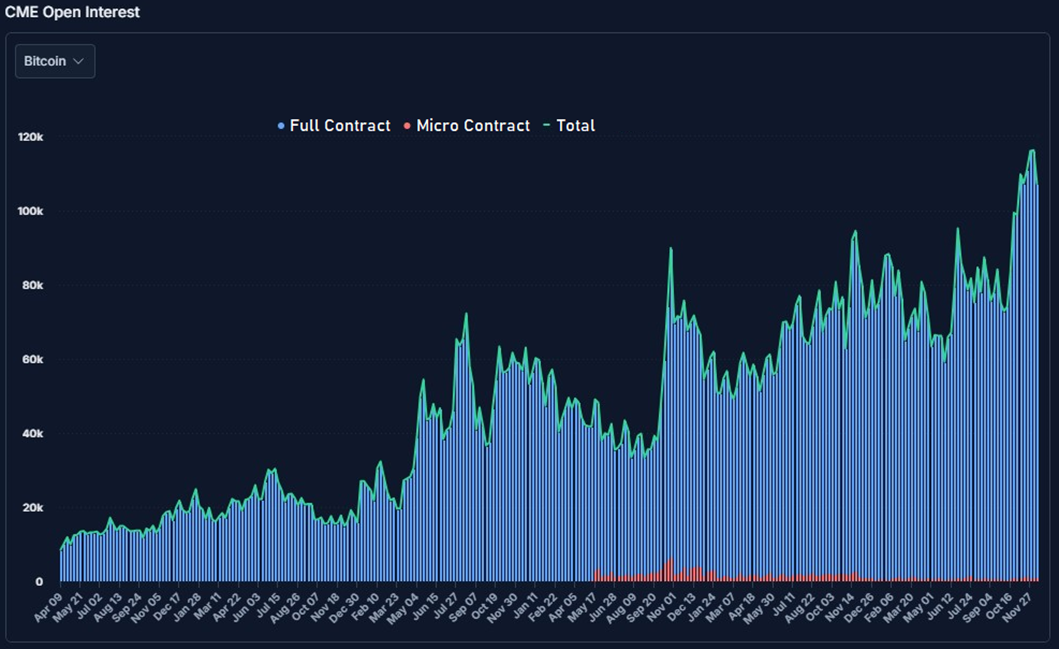

US Institutional players are in the market – while largely being unable to participate meaningfully in spot BTC markets, we would point to the significant growth of CME BTC futures open interest as coinciding with price movements of BTC this year. This has been even more apparent in the last few months. The formal approval of the ETF could see these players unwinding their positions as the short-term trade has played out.

GBTC has $26B in capital that has been locked up – as we highlighted above, GBTC is the largest vehicle that holds spot BTC in a tradeable US security. Most of this capital has been trapped within the Trust, with no redemption feature, and it has traded at a significant discount to NAV. If GBTC were approved to convert to an ETF, the discount (~10% currently) could narrow to close to parity to NAV. This could be an event that holders have been waiting for to exit the product. With holdings of ~620,000 BTC, a cash redemption-only approval by the SEC could result in Grayscale having to sell these holdings to meet significant redemption requests. We would note that we believe that there is a significant amount of GBTC held by funds that are able to “arb” the discount, by being long GBTC and short spot BTC though other vehicle. Holders of this trade are isolating the discount to NAV as a trade and unwinding it would not likely impact the price of BTC, as selling of GBTC would be offset by covering spot BTC shorts.

The door to retail/RIA market is wide open – this could be a source of significant sustained inflows over the next few years. Given the US RIA market's estimated $5-7 trillion in assets and its easy access to exposure to spot BTC price movements through a liquid product, even a modest and broad allocation to crypto could influence the demand for BTC. Our Digital Data Scientist David Kroger opines on anticipated inflows a spot BTC ETF could receive: “Our estimates are grounded in current global assets of $4.16 billion in Bitcoin ETFs tied to the spot price, including $2 billion invested in seven spot Bitcoin ETFs in Canada since 2021. Chainalysis adoption scores for Canada (.069) and the U.S. (.367) in 2023 suggest a 5.318 multiple in adoption, implying potential inflows of $10.6 billion in the first year. Alternatively, comparing the Toronto Stock Exchange (TSX) market cap of approximately $4 trillion CAD to the combined market cap of the U.S.'s NYSE and NASDAQ at $40 trillion USD, we could infer an approximate interest of $20.95 billion, nearly 10x what Canada saw.” Others have estimated inflows to be anywhere between $25-100B of inflows in the first year.

The advertisers are coming! – with almost 20 issuers vying for market share of the ETF pie, we would expect a heavy onslaught of marketing over the next few months. Not only do we expect print, online, and TV ads to become significant, the marketing efforts by issuers with RIAs and family offices would add material exposure to the potential for BTC investment.

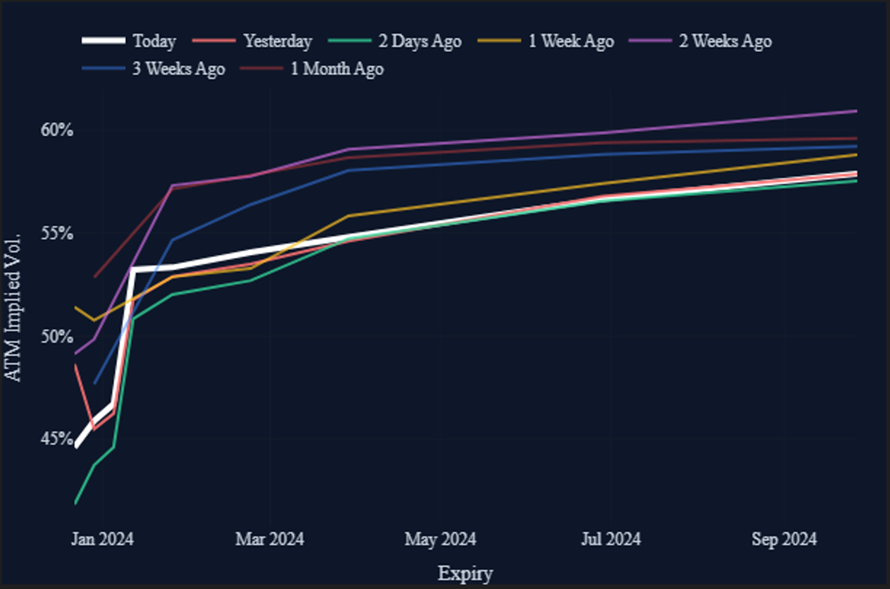

What are the options saying – we like to examine the options market to gather insights on implied option moves around a particular event. During the rapid rise in spot prices in Oct-Nov, we saw an explosion in option implied volatilities as systematic vol sellers (who had done well for the past year) were forced to cover their short vol positions. Interestingly, as realized volatility has slowly increased (from low 30s to low 40s) with several gap moves in the last 90 days, implied vols have softened to the mid-50s, from their initial pop to 60+ in October.

Another view of the options market is how At-The-Money (ATM) implied volatilities have moved over time. As we can see below, expiries before the Jan 10 window have fallen materially, as they should not capture the event. We can see implied for Jan 12 and further out remain elevated, but have been softening over the last month. This could be interpreted as the options market implying less of a move in the next few months, and that perhaps approval (being the base case) has been mostly priced in the near-term at this point.

But What If the SEC Doesn’t Approve It? – there are many ways to interpret further delays in approval, but a continued rejection seems unlikely at this point. There are several issues that remain outstanding, as the level of SEC and issuer interactions can attest to, but none seem like full deal breakers as of now. There could be downward pressure on spot BTC prices in a delay scenario as short-term holders, especially via futures, may look to unwind positions. Institutions that can trade listed equity options might look at near-dated put options on BITO (a futures-based ETF that more closely tracks spot BTC movements) if they are concerned about negative outcomes in the next few weeks.

IMPORTANT NOTE: We will be transitioning our StoneX Digital content delivery method to the StoneX Market Intelligence platform. If you are interested in receiving this note (and all future content, including future Deep Dive reports, daily trading commentary, etc.), please click the link below to confirm your contact details and sign up or reach out to the team at StoneXDigital@StoneX.com:

Market Intelligence Link