-------------------------------------------

**COPPER = the technical levels that I care most about have not changed in the past week. If anything, we have come closer to bringing back $9550 and 9617** into the fray. Hopefully, I have not provided the jinx by including such here -- as it has been quite some time since these numbers have been included in any of the work, I have shared over instant chat or email!

--Taking a step back, for 10 months we have been talking about $8318, 8520 & 8715 resistance vs 8238, 8028 support with the short-lived potential to see a return to a 7 handle. Boring and exciting at the same time! Today, we have managed to close above 8520 for the 10th time this year which improves the foundation that the optimists are building (23% of the YTD closes).

--Reality, as noted last week, is however, that the narrow sub $1000 trading range (ref LME 3s) remains intact. Until the Chinese have to pay more than they want to and/or other consumers of the red metal demand more units... U.S. interest rate policy, the DXY and the revolving loop of uncertainty in the macro is likely to dictate the upper and lower boundaries.

--The micro fundamentals need to tighten up further to outweigh the macro forces (let's use recent developments in Cocoa as an example). How much time should it take for the concentrate shortfall to feed through to the cathode balance? Two to three months was the chatter in the mix a month ago, so we are closer to the moment...

--The newest supply-side variables to add to the pot are from Vale, Glencore and BHP amongst others. As revealed late yesterday, Vale is somehow losing its mining license to operate Sossego (~70ktpa) in Para, Brasil. Measures are being taken to reinstate validity -- so we will have to wait and see how many greenbacks are needed or concessions of another sort!

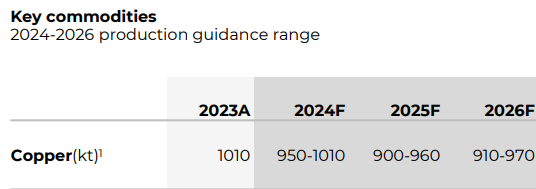

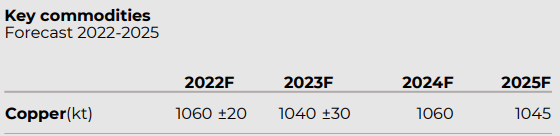

--Glencore has provided an update where you can lineup below (diagonal vision needed) - lower estimates as of yesterday's 2023 Preliminary Results for production in 2024-25 vs that which we received on Dec 6, 2022 in their Investor Update.

--Whilst we are on this topic, BHP gave us a wrinkle to think about in the future. Devil in the detail with their recently shared H23 results. Review slide 16 which focuses on the concentrator at Escondida delayed from '25/26 to '27/28. I believe we need to go back ~2 years to see the difference in summaries/decks -- which yields a ~100kt loss at the present... as discussions ensue regarding potential leaching options:

--Since spending time talking to clients/others in NYC on Feb 8/9, we have been knee-deep in conversations, largely revolving around reasoning to have length of some sort from 2H24 onwards. One trade we continue to mark is that which we recommended in November as the Panama situation was unfolding and TCs were falling = to borrow (buy/sell) Jun/Dec which is last at $49/t contango after tightening up to 30c the other day = recall this has come-in all the way from the $140 to 120c region as seen here:

LME Jun/Dec24 spread - is a 'back' inevitable?

--Another trade we have looked at once more after also recommending such in November, is to be long vol via calls (aka upsides or bullish option structures). What follows here is a chart of LME Copper 0.50 delta implied vol on a rolling 1 year basis = you can see the bid that arrived with Trump's election victory in 2016, the start of COVID-19 in 2020 and the recent move on the back of supply problems from Panama (P), Anglo American (A) & others (O) which I have labeled as PAOS (Panama, Anglo & Other shortfalls).

--Approximately 3,500 lots of open interest sits in the Dec24 expiry $10k call strike, followed by 466 lots in the $10.5k calls, 450 lots in the $10.6k calls before seeing 4,681 lots of OI in the $11k strike and 2,676 lots in the $12k strike [I repeat, only referencing the Dec24 expiry here]. Further forward, volumes/OI naturally falls off a bit with the similar range of strikes for Dec25 expiry, $10k to 12k, only amounting to a cumulative 1,291 lots of open interest.

--Switching to demand, I reference a conversation with market participants. Wins in consumption focus on new energy demand & regional energy security priority over GHG emissions in China as well as NEV production which received a +1.5 million unit increase in '23 from 7m units in '22 and forecasts for ~11.5m in 2024. Taking other end-use areas into the equation in China and Globally, whilst demand forecasts are largely balanced vs supply in 2024, there is clear room for movement in the S&D balance if China consumption manages to grow above 5% this year as it did in '23, amongst other variables.

--Finally, we must keep an eye on Chinese housing completions and the global inventory situation for copper cathode. If and when the red metal can convincingly take out $8520 and 8715, then let's take a look at the copper scrap supply-side potential... Until then, keep your ear to the ground on stimulative measures in China for residential, commercial and other infrastructure related projects as well as consumer confidence which was crushed during Xi's rolling lockdowns of 2020-22!

------------------------------------------

**NICKEL = in recent days Xiaoyu and I have commented on the upside potential for price and whilst the naysayers have advised us in recent months, "don't cry wolf", we apologize for being too early with the call to buy futures in December ahead of the commodity index rebalance in early January... but feel it's 'different' now. Notes from the last 24 hours follow:

--Sanction headlines earlier this week - US vs Russia could impact nickel more than ali - which provided the catalyst for the initial bid, yes.

--BHP criticized the increase of LME nickel cathodes brands, which are not suitable for battery production and do not comply with ESG standards.

--Market chatter has Tsingshan pausing some high-cost nickel matte production due to the profitability concern (low nickel price), which led to tightness in nickel sulfate -- a reminder is that the average cost for nickel sulfate production is circa $15.5k/t.

--Which brings us to the largest spec short for our LME positioning model (-7 on the -10 to +10 scale) and now back above $17k to the top-end of the trading range since November = resistance we have our eyes = 17375, 17600 & 18230.

--In short, yes, good volume selling showed up above $17k, which we expected as the 1st battleground zone.

--Still, we think there is merit to add length 'in here' looking for a weekly settlement break of $17375... which can than lead to more MT/LT short-covering up towards 18000/230 which could act as a larger/much needed basing area.

--Do not forget that P. Subianto's expected victory in Indonesia should keep the mining policy as status quo, maybe even becoming more nationalistic & conservative!?!:

https://www.spglobal.com/marketintelligence/en/news-insights/latest-new…

------------------------------------------

**ALI = as M. Lovecchio pointed out yesterday and again today, the bid seen this week on the back of headlines related to sanctions from the U.S. or UK seemed to be poorly placed - not a reason to leg into a fresh long position, quite the contrary which a Producer or two jumped onto at/around $2265/50 basis LME 3s

--The U.S. already has a 200% tariff on Russian aluminum imports (issued 1 year ago), and the U.S. has not imported any Aluminium (of size) from Russia since 2022. So for something to be meaningful it will have to be agreed at the G7+ level to move the needle (which we would assume takes longer to ink).

--As for today, the UK released Russia sanctions (https://shorturl.at/lvMO7) but it is important to highlight that nobody from RUSAL was mentioned on the list as we witnessed in 2018, which makes it much more difficult for the U.S. to bring them into the mix when they announce details tomorrow.

--In today's sea of green, aluminium was front & center = flat out of love. We may need to wait until China's economy is super healthy which could be indicated by a new chapter of the Blue Sky policy, which has fallen to the back burner over the last year-plus!

--The 3 horizontal lines in the chart below, white, green and red show us how tight the trading range is - until push comes to shove, right? We need to see demand kick-in to a higher gear or prices weaken further to knock out production, b/c all the tonnes from Russia continue to make their way into China & elsewhere - 3M LME Aluminium, $/t - stuck between $2300 and 2150 for the most-part since May 2023

------------------------------------------

We will be in touch with more inputs. Until then, all the best,

Mike

*Sources on charts = Bloomberg unless noted otherwise above the graphic*