USDBRL is expected to reflect data from Brazil and the US, aiming to recalibrate interest rate expectations in both countries

- Bullish

- Brazil’s GDP moderation in the third quarter could increase bets on an early start to a cycle of cuts to the benchmark interest rate (Selic), which would hurt foreign investment attraction and weaken the Brazilian real.

- Bearish

- The release of private data on the US economy could strengthen investors' bets on interest rate cuts by the Fed in December, which would hurt external capital attraction and likely weaken the US dollar globally.

The week in review

- Global financial market trading volumes were reduced due to the Thanksgiving holiday in the US.

- US data suggested a sharper-than-expected weakening of the American economy, reducing bets on Fed interest rate cuts and boosting appetite for riskier assets.

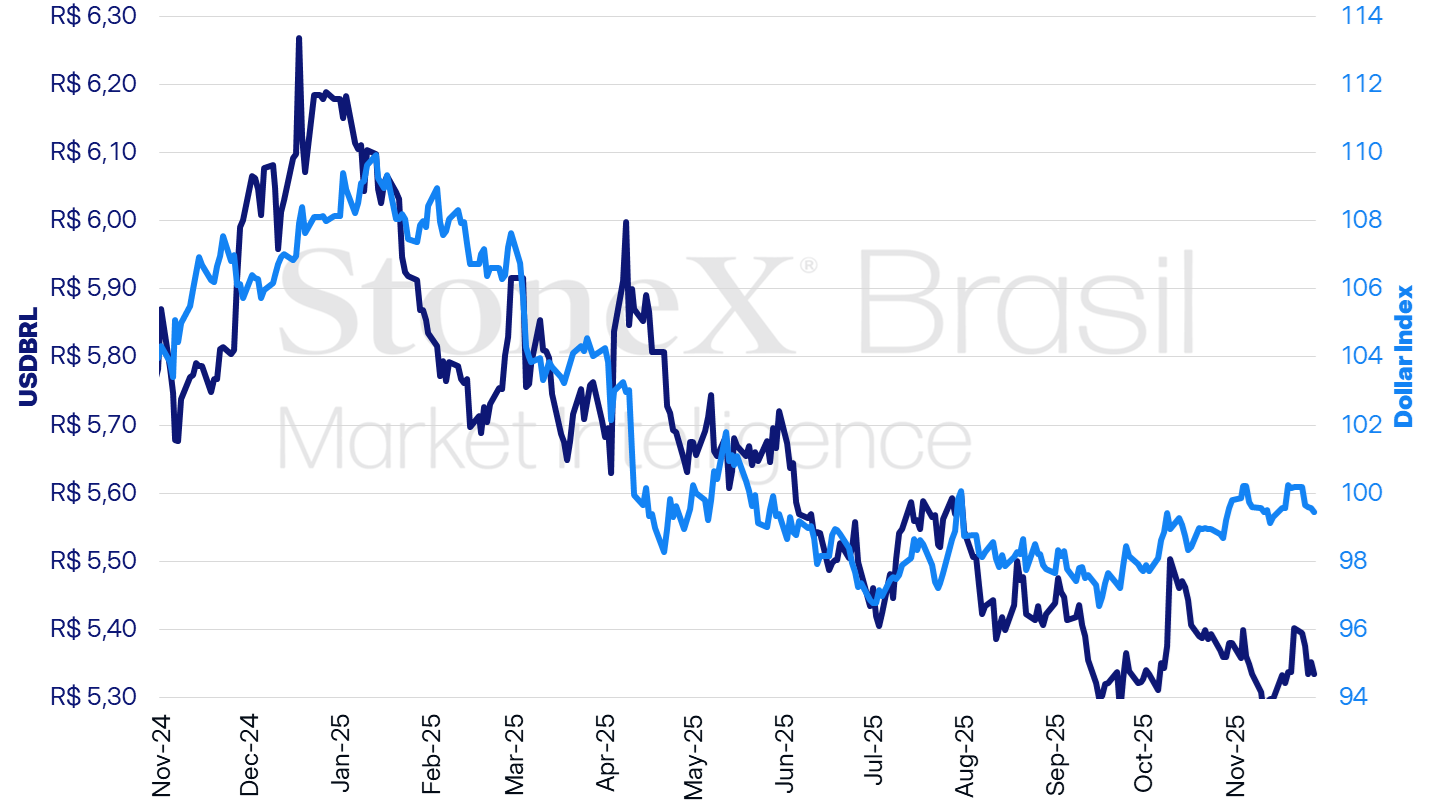

USDBRL and Dollar Index (points)

Source: StoneX cmdtyView. Prepared by: StoneX.

USDBRL variations | Daily: -0.32% | Weekly: -1.25% | Monthly: -0.84% | Year-to-date: -13.65% | Last 12 months: -10.95% |

Dollar Index variations | Daily: -0.12% | Weekly: -0.75% | Monthly: -0.36% | Year-to-date: -8.04% | Last 12 months: -6.31% |

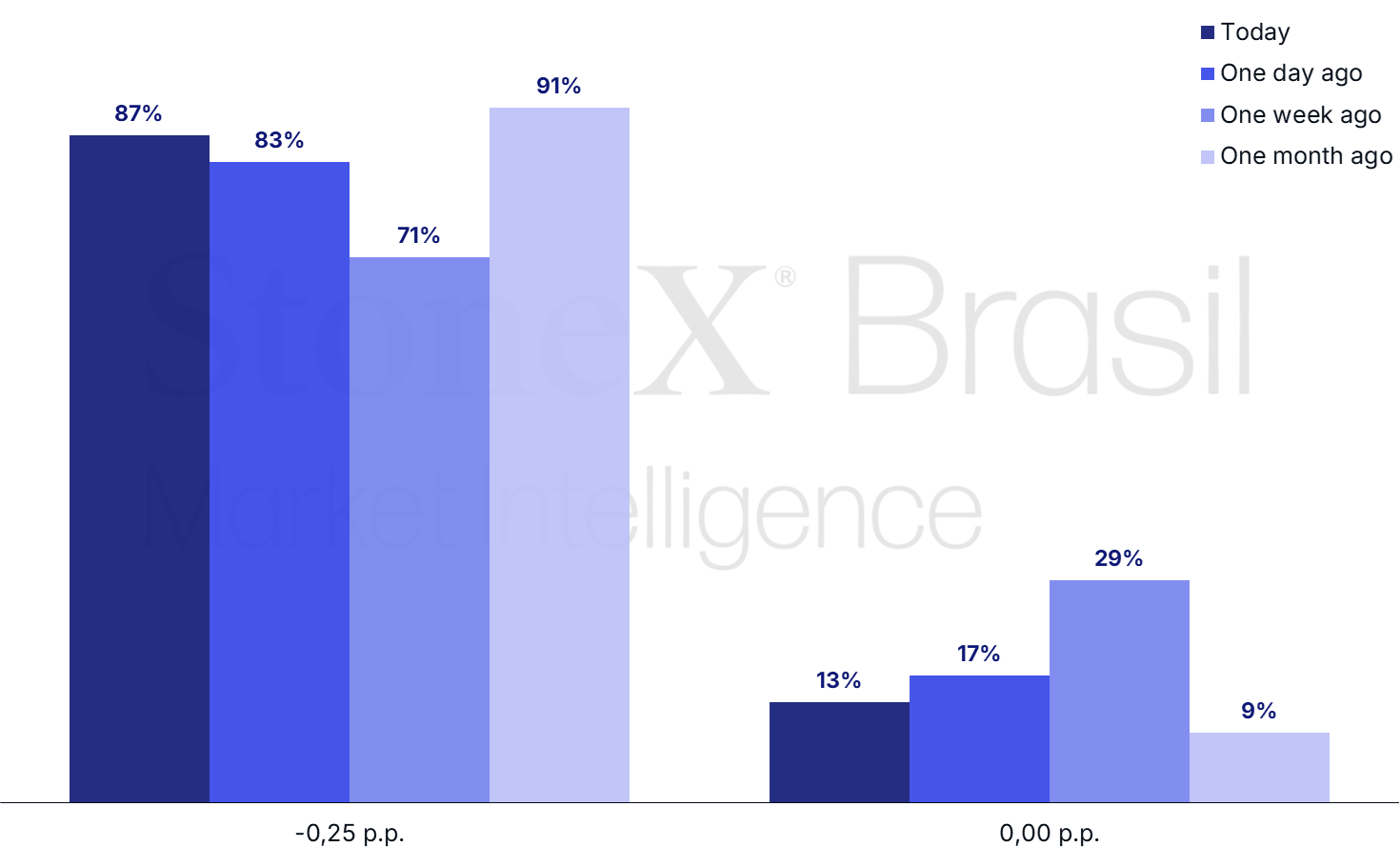

Key Events: Expectations for US interest rate cuts

Expected impact on USDBRL: Bearish

Bets for the Federal Reserve’s December 10 interest rate decision

Source: CME FedWatch Tool. Design: StoneX. Futures market probabilities based on November 28, 2025.

Investors are expected to closely monitor the release of private data on the US economy to recalibrate expectations for the country’s interest rate trajectory.

- Indicators will carry greater weight than usual due to delays in the publication of official statistics caused by the US government shutdown.

Why This Matters: The perception that US interest rates will fall at a faster pace could reduce the yield on US Treasury bonds and hinder external capital attraction, weakening the dollar globally.

Contradictory Scenario: In recent weeks, data on the US economy has presented a mixed picture, with some indicators signaling stronger-than-expected performance while others suggest weaker-than-anticipated results.

- This scenario seems more aligned with a gradual economic slowdown rather than a sudden and intense deterioration.

Conflicting Interpretations: This mixed scenario also leads to differing interpretations among Fed members regarding the economic outlook and the balance of risks facing the US.

- Recent statements from Federal Open Market Committee (FOMC) members revealed that five support pausing the rate cut cycle, citing a better balance between inflation acceleration risks and labor market weakening.

- Another four members advocate for a new rate cut in the December 10 decision, arguing that labor market weakening risks remain predominant.

- The remaining three members have not commented or left their positions unclear.

- As a result, the decision appears uncertain and difficult to predict.

- However, it’s likely the decision—whether a cut or rate maintenance—will have broad support, as Fed Chair Jerome Powell is known for fostering consensus and minimizing dissension.

Majority Bets: Despite contradictions in economic data, risk assessments, and FOMC member opinions, investors have solidified their bets that the Fed will cut rates in the upcoming decision.

- These bets focus on indicators pointing to greater economic weakness, downplaying data that contradicts this view.

- Investor expectations could further strengthen this week following the release of ADP’s November private employment data and ISM’s Purchasing Managers’ Index (PMI).

Anticipating Changes at the Fed: Additionally, media reports suggesting White House Economic Council Director Kevin Hassett is the frontrunner for the next Fed chair have fueled investor expectations for a faster rate-cut cycle.

- Powell’s term as Fed chair ends on May 15, although he may wish to remain on the Board of Governors until January 2028.

- Investors perceive Hassett as the candidate most aligned with the White House, likely advancing Donald Trump’s priorities. His nomination raises concerns about the Fed’s independence.

- Trump believes US interest rates can drop significantly without spurring inflation, leading to assumptions Hassett would push for faster and potentially imprudent rate cuts.

- However, an official nomination may take weeks. Treasury Secretary Scott Bessent indicated there’s “a good chance” Trump will announce his pick by Christmas.

Brazil’s Q3 GDP

Expected impact on USDBRL: Bullish

This week’s highlight in Brazil is the release of third-quarter GDP data, expected to confirm the country’s economic growth moderation trend.

Why This Matters: If confirmed, GDP moderation could increase investor bets on faster interest rate cuts by Brazil’s Central Bank, as inflation gradually stabilizes toward the target.

- This, in turn, would reduce the appeal of domestic bonds and harm foreign capital attraction, weakening the Brazilian real.

Expectations: Median projections indicate quarterly GDP growth may have declined from 0.4% in Q2 to 0.3% in Q3.

- Annualized growth over four quarters could decrease from 2.0% to 1.8% during the same period.

- While the Central Bank remains concerned about Brazil’s inflation dynamics, weaker economic activity could prompt an earlier start to Selic rate cuts.

- Currently, most forecasts anticipate the first cut will occur at the January 28 decision.

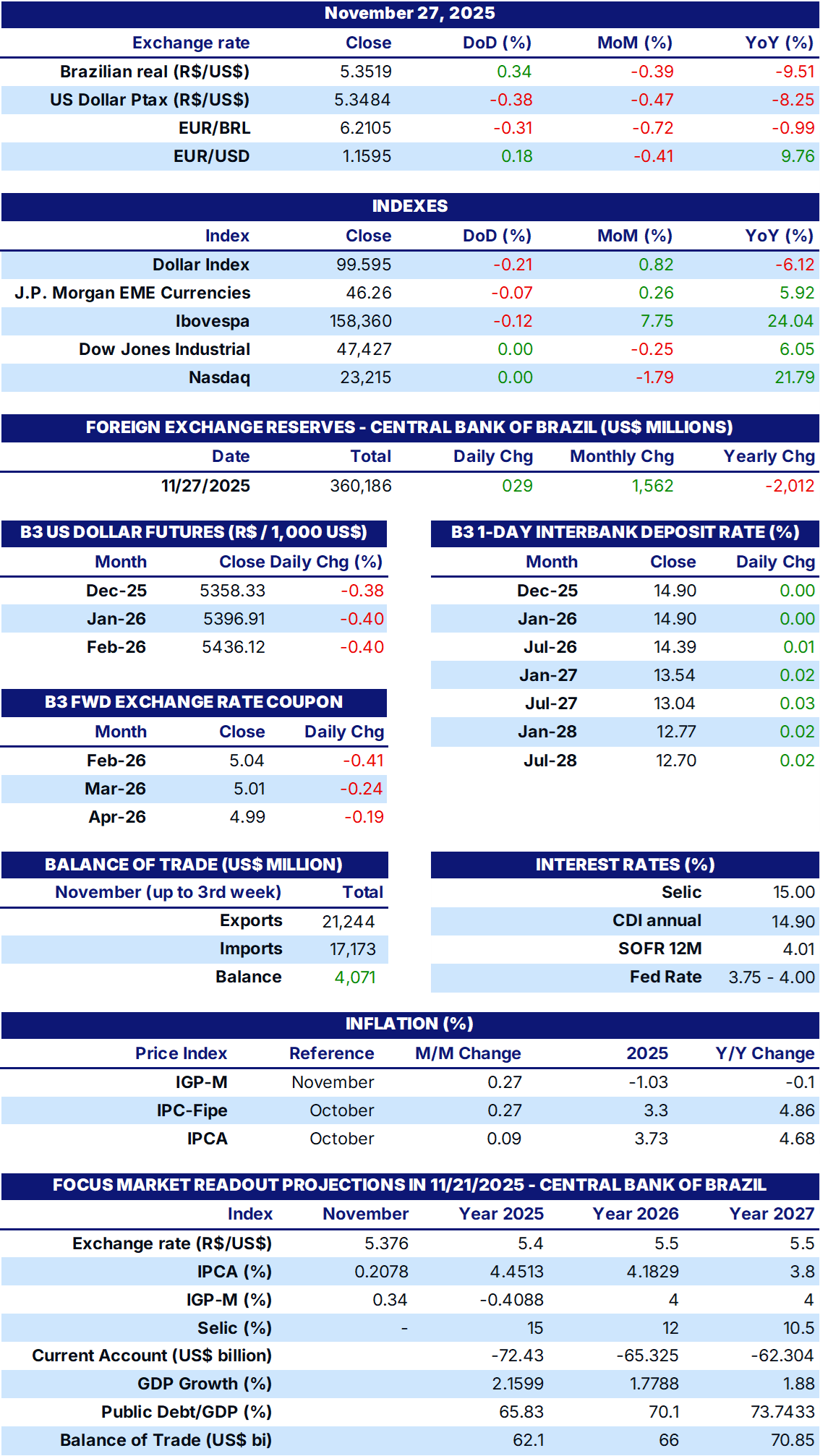

INDICATORS

Sources: Central Bank of Brazil; B3; IBGE; Fipe; FGV; MDIC; IPEA; and StoneX cmdtyView.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided. References to over-the-counter (“OTC”) products or swaps are made on behalf of StoneX Markets LLC (“SXM”), a member of the National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM. StoneX Financial Inc. (“SFI”) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (“SEC”) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Adviser. References to securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to exchange-traded futures and options are made on behalf of the FCM Division of SFI . StoneX is a trading name of StoneX Financial Ltd (“SFL”). SFL is registered in England and Wales, Company No. 5616586. SFL is authorized and regulated by the Financial Conduct Authority [FRN 446717] to provide to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorised to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorised & regulated by the Financial Conduct Authority under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorised by the Financial Conduct Authority. StoneX Group Inc. acts as agent for SFL in New York with respect to its payments services business. StoneX APAC Pte. Ltd. acts as agent for SFL in Singapore with respect to its payments services business. ‘StoneX’ is the trade name used by StoneX Group Inc. and all its associated entities and subsidiaries.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

© 2026 StoneX Group Inc. All Rights Reserved.