The MarketWatch Update

Today's commodity market news and analysis/advisory guidance.

US RJO - Scott Magnuson, CTA

- Precious Metals

- Grains & Oilseeds

- Energy

- Coffee

- Cotton

- Sugar

- Meats & Livestock

- Currencies

- Interest Rates

By: Vitor Andrioli, Market Intelligence Manager - Brazil

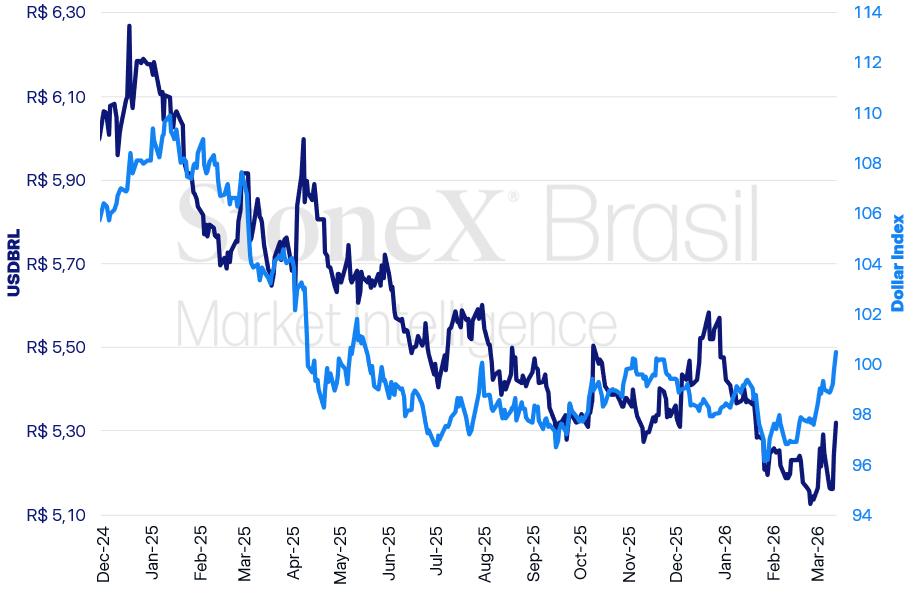

USDBRL and Dollar Index (points)

USDBRL Variations

Daily: +1.47% | Weekly: +1.37% | Monthly: +3.58% | Annual: -2.84% | 12 Months: -8.23%

Dollar Index Variations

Daily: +0.74% | Weekly: +1.48% | Monthly: +2.95% | Annual: +2.18% | 12 Months: -3.26%

The ongoing conflict between the US, Israel, and Iran enters its third week, with the Strait of Hormuz effectively closed during this entire period, increasing uncertainty and fears of global inflation among investors.

Why This Matters: The global environment remains marked by heightened uncertainty, reflected in pronounced volatility in financial markets. Oil futures prices continue to serve as a key gauge of investor sentiment, reacting to each new development in the conflict.

Conflict Duration: Currently, news suggests a mixed scenario, contributing to investor uncertainty.

Oil Price Surge: On Friday (13), investors reacted to news that the US had granted a 30-day exemption allowing countries to purchase Russian oil derivatives currently in transit, despite sanctions imposed at the start of the Ukraine War.

Inflationary Impacts: Amid rising oil prices, the risk of prolonged inflationary shocks remains the primary concern for investors and monetary authorities.

In Brazil, investor focus will turn to “Super Wednesday” (18), when both the Central Bank of Brazil and the Federal Reserve will hold their monetary policy meetings on the same day.

Why This Matters: A reduction in the benchmark interest rate lowers the attractiveness of domestic assets, which tends to weaken the real globally.

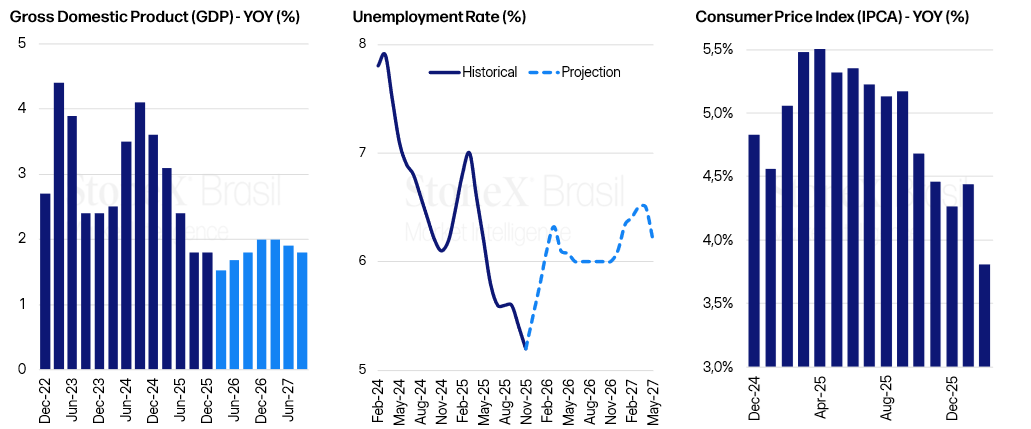

Inflation: The latest release of the Broad Consumer Price Index (IPCA) slightly exceeded expectations, surprising investors.

Economic Activity: GDP data for Q4 2025 aligned with expectations but indicated a slowdown in economic activity during the second half of the year.

Labor Market: The latest data showed Brazil’s unemployment rate rising to 5.4%, in line with expectations.

Interest Rate Outlook: In late February, the majority of bets were on a 0.5 percentage point cut. However, the Middle Eastern conflict and the surprise IPCA data have led to more dispersed expectations.

Brazil Economic Indicator Overview

US Interest Rate Decision

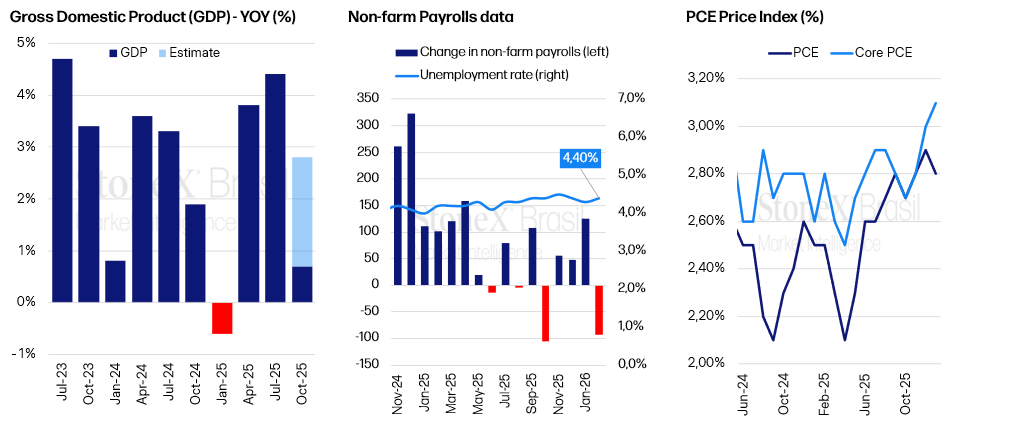

In the US, unlike Brazil, the expectation is for the benchmark interest rate to remain unchanged. Investors’ focus will be on statements from Federal Open Market Committee (FOMC) authorities, particularly regarding the impacts of the Middle Eastern conflict and future monetary policy direction.

Why This Matters: The expectation of prolonged maintenance of the benchmark interest rate could increase the attractiveness of domestic assets, strengthening the dollar globally.

Inflation Concerns: This week, the Personal Consumption Expenditures (PCE) Price Index—the inflation indicator most closely watched by the Federal Reserve—showed signs of deceleration. However, its core component remains concerning.

Economic Activity and Labor Market Indicators: While inflation remains resilient, typical of a heated economy, other indicators suggest the opposite.

Interest Rate Outlook: Recent indicators present a mixed picture of the US economy. While inflation remains elevated, economic activity and labor market data show signs of weakness.

US Economic Indicator Overview

Next week, markets will also monitor the European Central Bank’s (ECB) interest rate decision.

Why This Matters: Maintaining interest rates in the European Union tends to favor euro appreciation against the dollar. This movement could indirectly benefit the real, as a stronger euro is often associated with a weaker global dollar.

Committee Member Projections: Alongside the interest rate decision, the ECB will release official forecasts from committee members. Markets will closely watch these updates amid growing fears of an inflationary escalation due to rising energy costs following last week’s Strait of Hormuz closure.

Analysis: In a scenario where purchasing power increasingly dominates global public discourse, a renewed inflation spike could heighten popular dissatisfaction with incumbent governments.

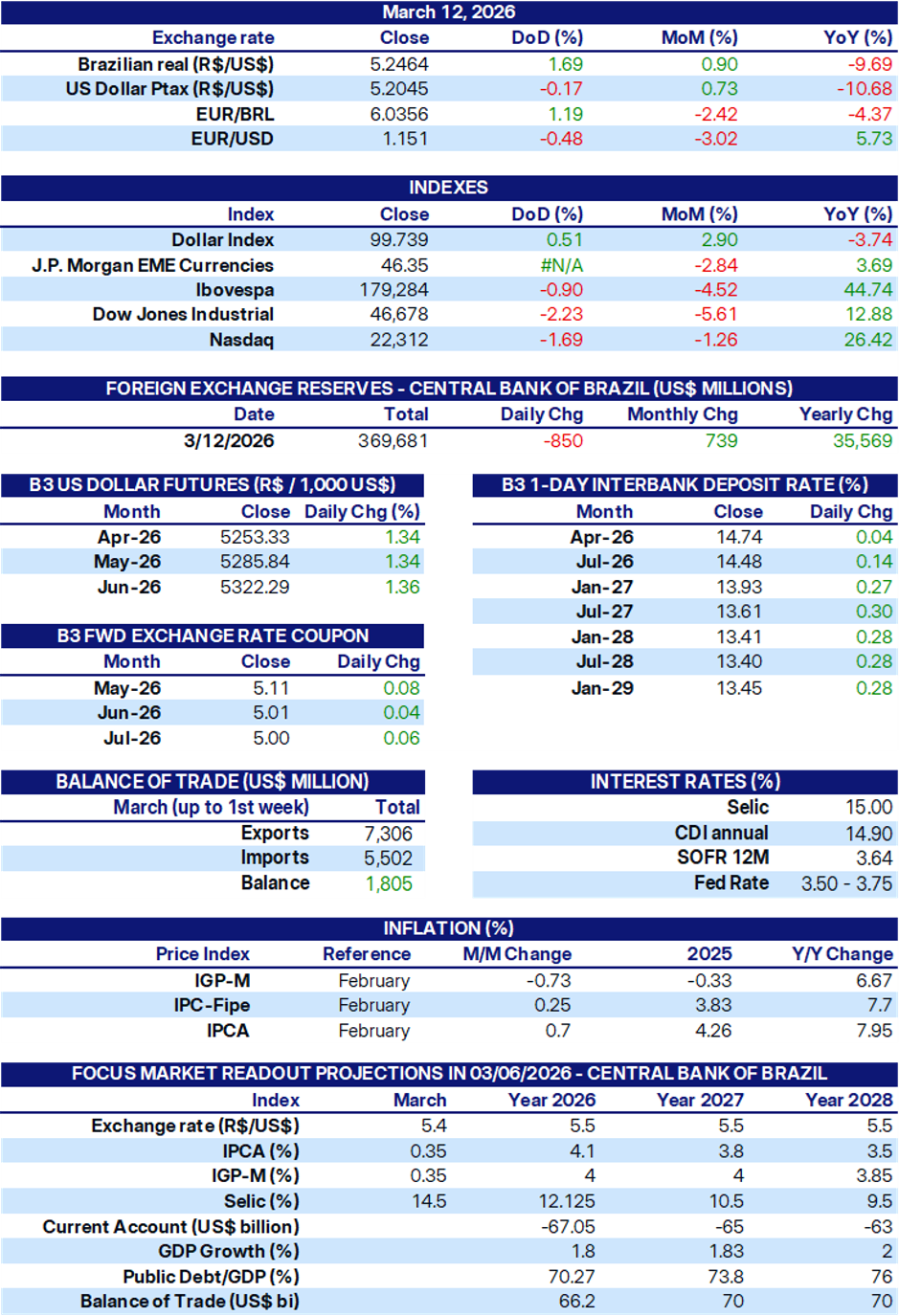

INDICATORS

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided. References to over-the-counter (“OTC”) products or swaps are made on behalf of StoneX Markets LLC (“SXM”), a member of the National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM. StoneX Financial Inc. (“SFI”) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (“SEC”) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Adviser. References to securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to exchange-traded futures and options are made on behalf of the FCM Division of SFI . StoneX is a trading name of StoneX Financial Ltd (“SFL”). SFL is registered in England and Wales, Company No. 5616586. SFL is authorized and regulated by the Financial Conduct Authority [FRN 446717] to provide to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorised to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorised & regulated by the Financial Conduct Authority under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorised by the Financial Conduct Authority. StoneX Group Inc. acts as agent for SFL in New York with respect to its payments services business. StoneX APAC Pte. Ltd. acts as agent for SFL in Singapore with respect to its payments services business. ‘StoneX’ is the trade name used by StoneX Group Inc. and all its associated entities and subsidiaries.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

© 2026 StoneX Group Inc. All Rights Reserved.

Our subscribers have access to comprehensive market analysis from StoneX spanning commodities, equities, currencies and more.

Today's commodity market news and analysis/advisory guidance.

Dollar expected to reflect inflation data in the US and Brazil, geopolitical tensions in the Middle East, and ECB interest rate decision

This daily commentary delivers a concise, expert-driven overview of global futures markets, designed for traders and investors seeking actionable insights. Each edition covers the technical setups, and trade recommendations across major commodity contracts, including grains, livestock, metals, energy, currencies, and equity indices.

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bi-lateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve; our financials and record of accomplishment are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform, to “boots on the ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.