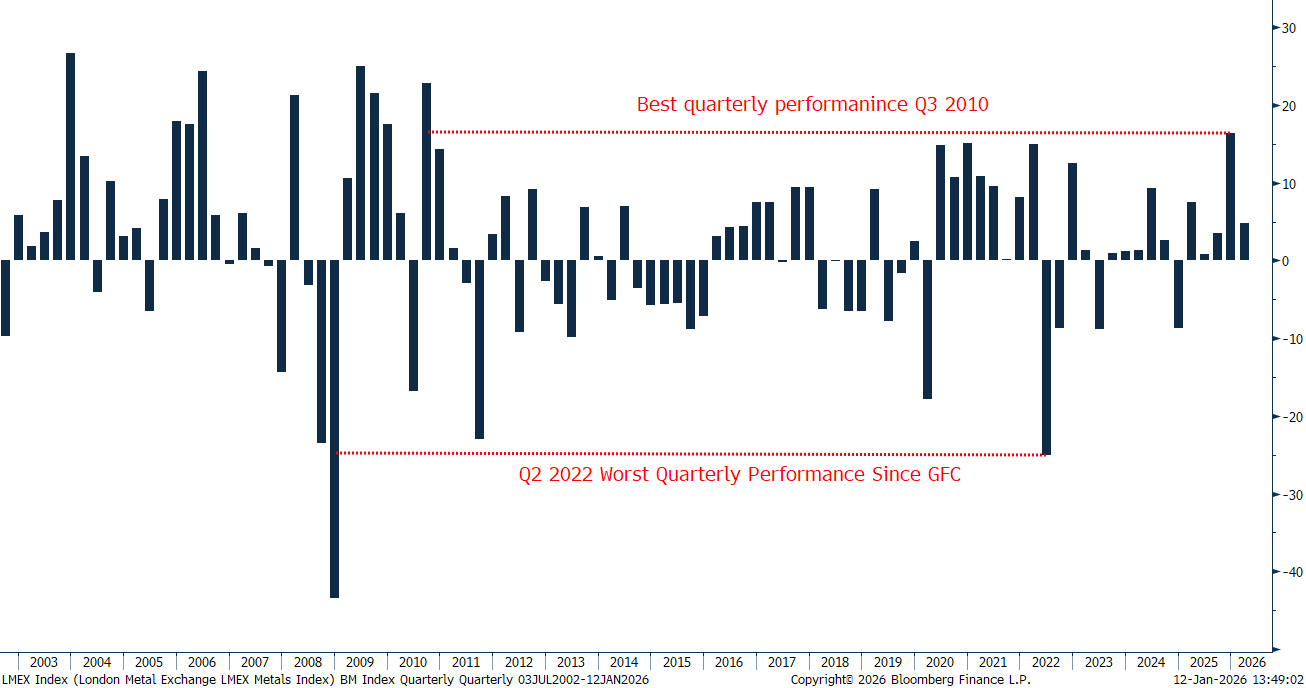

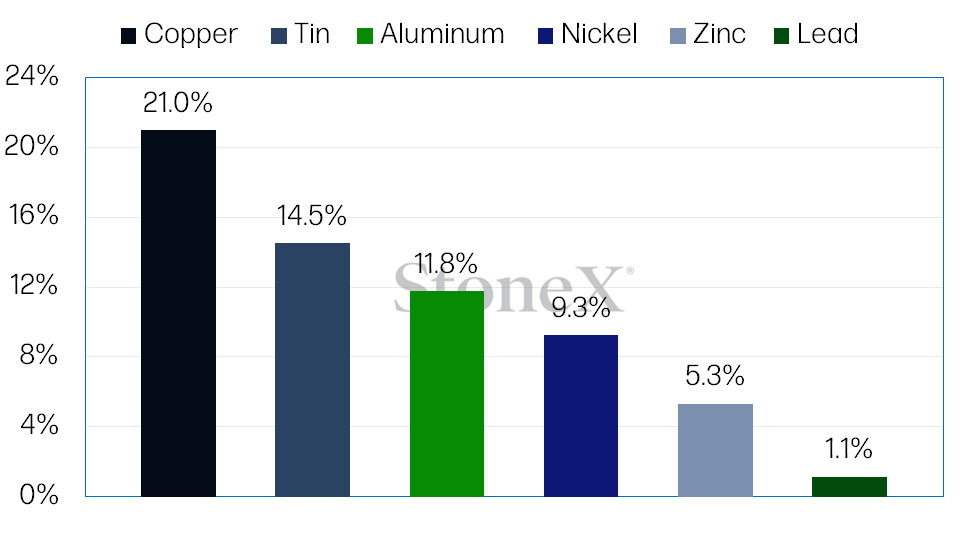

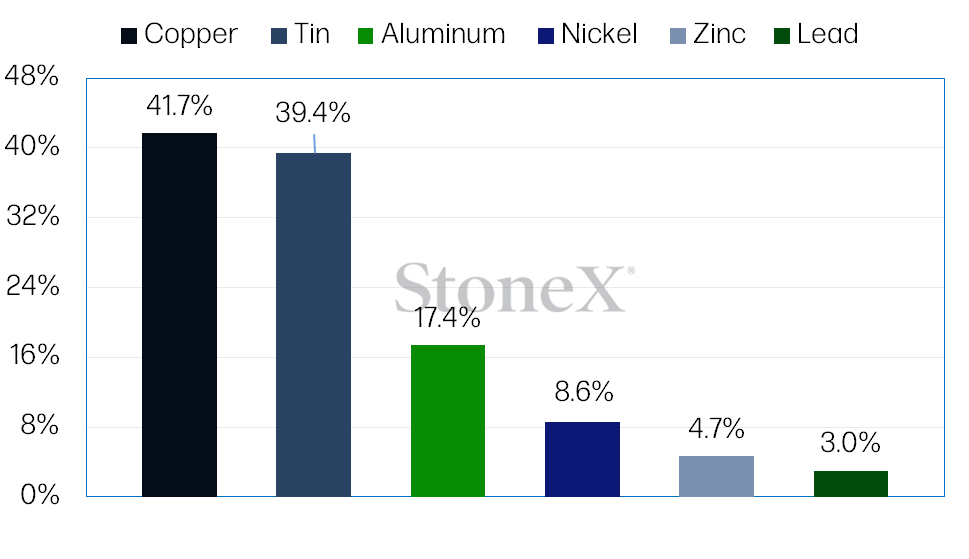

The LME base metal index closed last year with its largest annual gain since 2021 (30.5%), in large part driven by a robust performance over Q4 in which the index jumped 20.0%, posting its quickest quarterly rise since Q3 2010. The outperformance in the final quarter of the year dwarfed gains over Q3 (+3.5%), in which prices principally took their cues from weakness in the US dollar (on rate cut expectations), counteracting the traditional off-season for demand. Over Q4, the performances within the suite itself were highly divided with gains attached to specific metals including copper (+21.0%) and tin (14.5%) posting nominal record highs, alongside aluminium (11.8%), recording multi-year highs. Meanwhile, gains for nickel (9.3%) and zinc (5.3%) were more measured, while lead came in almost flat (1.1%). Typically when it comes to price forecasting for industrial metals, we look at impacts that will affect each metal from a macroeconomic, fundamental and speculative perspective; however, on the introduction of global and sector specific tariffs from the US this year, we now include this as one of our major price driving parameters.

LMEX Index Quarterly Price Performance

Source: Bloomberg

LME 3M Base Metal Q3 Price Performance

Source: Bloomberg

LME 3M Price Performance 2025

Source: Bloomberg

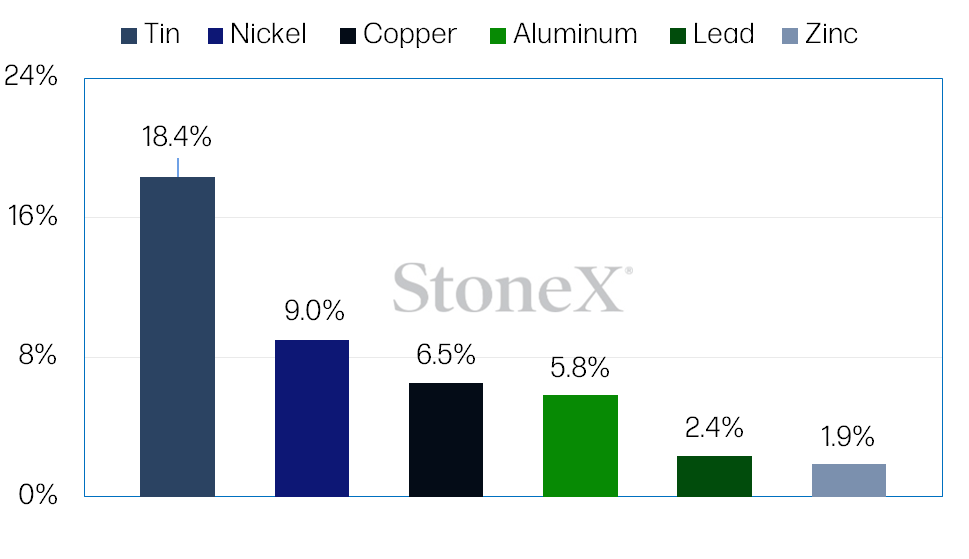

LME 3M Price Performance 2026 YTD

Source: Bloomberg

Q1 Bullish Parameters

- Supply side risks will remain prevalent in Q1, especially for metals such as copper, nickel and tin. Meanwhile, China announced at end-September that it will lower its annual output for key non-ferrous metals over 2025 and 2026.

- The impact of US sector-specific tariffs has resulted in increasing domestic premiums for metals such as copper, aluminium and zinc, encouraging atypical trade flows, creating tightness ex-US.

- China is expected to outline metal-intensive spending in its Two Session meeting in March, while providing targets for the start of the 15th Five Year Plan (2026-2030).

Q2 Bearish Parameters

- Traditional seasonal demand in China for ‘Golden September and Silver October’ disappointed, limiting expectations for demand ahead of the Chinese New Year. Attention will be paid to domestic inventory levels with Q1 a traditional period of restocking.

- The dramatic surge in prices for tin, copper and aluminium over the final quarter of the year may translate into downstream purchasers using just-in-time methods to obtain required material.

- At the time of writing, the market is pricing in only a 16% chance for a 25bps US rate cut in January, limiting one of the key parameters behind US dollar weakness.

Key

Source: Bloomberg

LME 3M Copper Price Performance 5Y

Source: Bloomberg

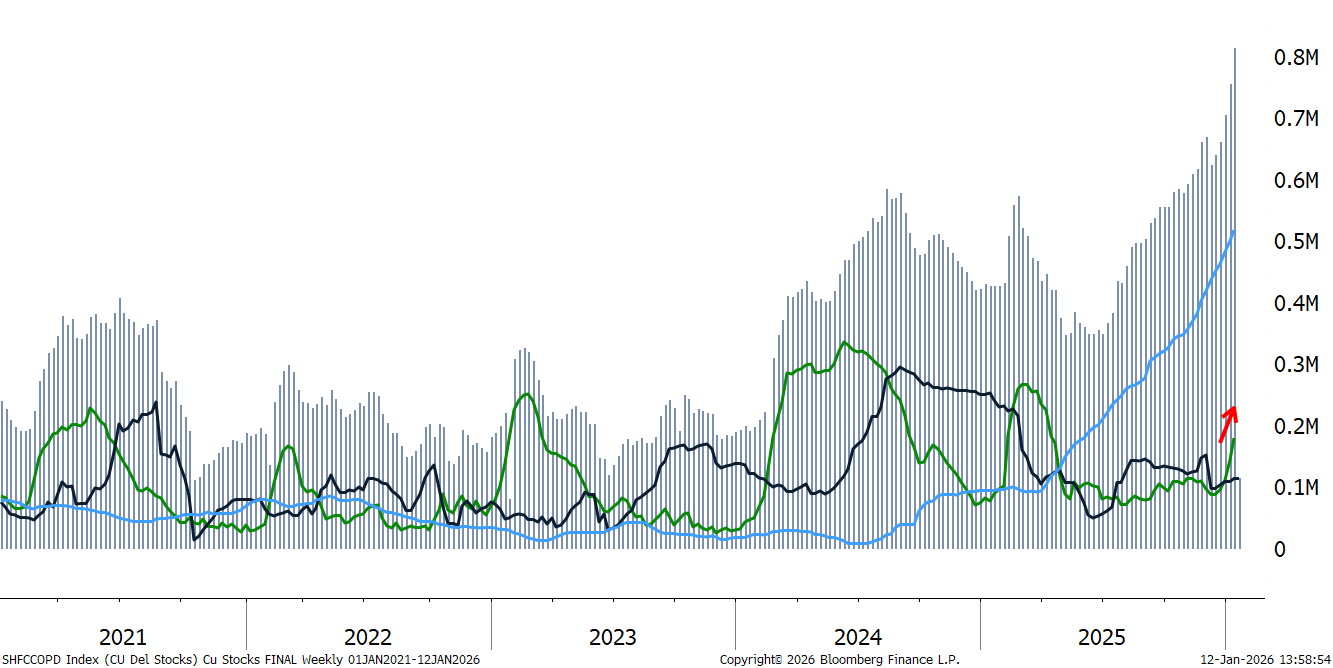

Visible Exchange Stocks

Source: Bloomberg

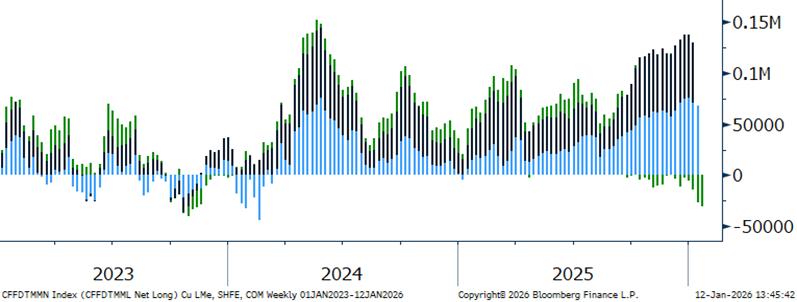

LME, SHFE & COMEX Net Positions

Source: Bloomberg

Copper ended 2025 as the best performing base metal having posted a nominal record high (at the time) on 30th December of $12,559/t, marking an annual gain of 41.7%. Copper’s remarkable climb over the course of the year, and in particular Q4 (+21.0%), was supported by a perfect storm of factors. Firstly, we witnessed a warming in the macroeconomic outlook, with China-US tensions lowering, the Federal Reserve moving to cut rates three times in 2025, China outlining metal-intensive spending in the year ahead, the end of the US Government shutdown and tentative talks of peace in Russia and Ukraine. Secondly, within the fundamentals, the conclusion of negotiations between Chinese smelters’ and major miner Antofagasta resulted in a record low RCTC benchmark of 0 cents per pound and $0/t, increasing supply risks following a year in which more than 500,000t of mined supply was removed from the market following disruptions, resulting in flat mine production growth. Thirdly, the expectation for future US import tariffs on refined copper has resulted in >890,000t of metal entering the country, creating tightness ex-US, with two-thirds of global visible stocks now held within COMEX. Given these factors, speculative investors have soared into copper with net longs on COMEX and LME at their highest levels on record and March 2025 respectively. As things stand, withholding a downward shock to the macroeconomic landscape, we expect copper prices over the next three-to-six months to be led by sentiment from investors over US copper specific tariffs, with focus on regional levels of global stocks and material entering the US, rather than underlying global fundamentals (i.e. demand). In turn, we expect copper to trade within a new higher normal range over this period, posting bouts of volatility within the forward curve.

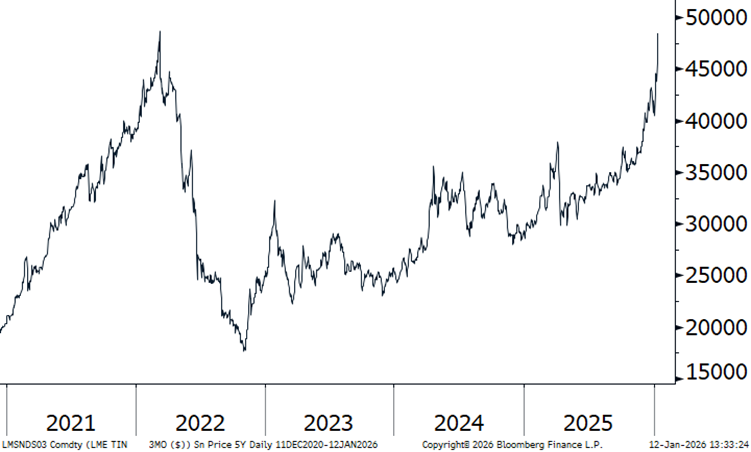

LME 3M Tin Price Performance 5Y

Source: Bloomberg

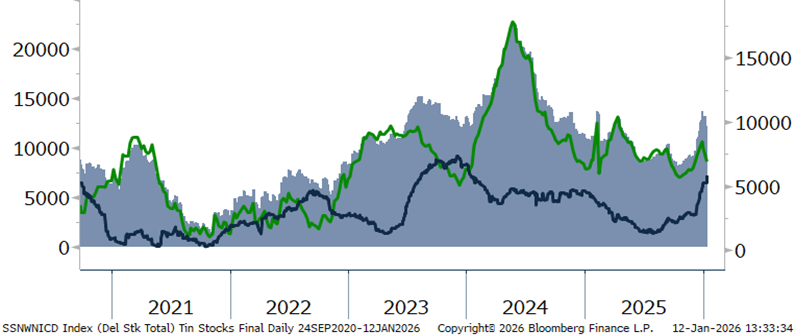

Visible Exchange Stocks

Source: Bloomberg

LME & COMEX Net Positions

Source: Bloomberg

Tin’s robust performance over the final quarter of the year secured its place as the second best performing base metal in 2025 (39.4%), resulting in a nominal all-time high of $43,277/t being posted on 19th December. Tin’s key price drivers have stemmed from the fundamental and speculative sides of the market. Within the fundamentals, inflamed supply side risks (with 40% of mined production having faced a form of disruption in 2025, including within major producing countries such as the DRC, Indonesia, Bolivia and Myanmar), resulted in refined output coming in flat (+0.3%). Meanwhile, tin’s resilient and fast-growing demand associated with its use in renewable energy, new digital applications and energy storage, lead to tin posting a second year of deficits (-5,600t). As a result, tin gained focus from the global speculative market, with LME net longs hitting a record high on 12th December. Looking to the quarter ahead, we expect supply risks to remain prevalent, especially given that Indonesia (the second largest tin miner in the world) vowed to close 1,000 illegal mines in the country, while also moving in October to a one-year, from three-year, KRAB license requirement. Furthermore, questions marks surround the level of production from Myanmar’s largest mine Man Maw in the Wa State, which was expected to come out of a 20-month mining ban in August. However, as it stands, imports of tin ore into China remain down 70% Y/Y in 2025, with average monthly exports to China at just 2,175t, a far cry from the 15,000t level pre-closure. Note, Myanmar is the third largest tin producing country in the world and the largest importer of tin ore to China, in 2022 accounting for ~77% of the country’s imports. Given this, we expect tin to remain vulnerable to the upside at the start of 2026, with volatility likely given its small market size versus the rest of the suite and current stretched speculative positioning.

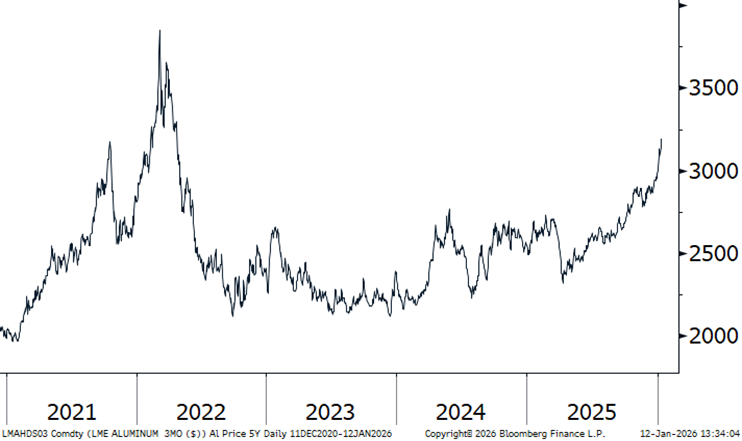

LME 3M Aluminium Price Performance 5Y

Source: Bloomberg

Visible Exchange Stocks

Source: Bloomberg

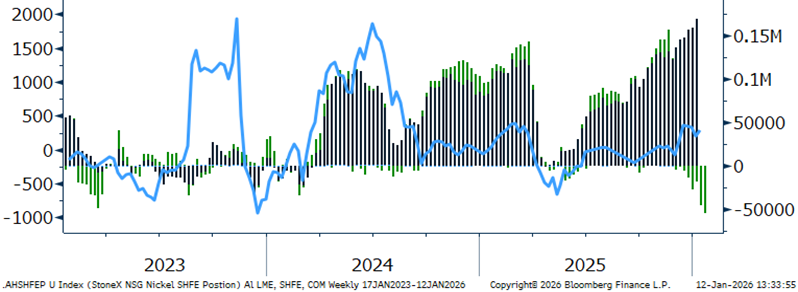

LME, SHFE & COMEX Net Positions

Source: Bloomberg

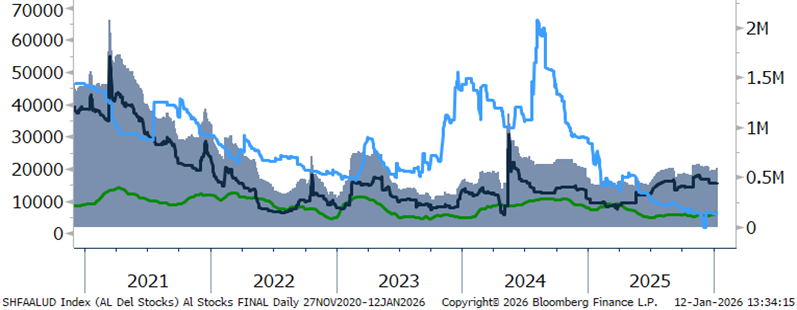

Aluminium posted a gain of 11.8% over Q4, taking the spot as the third best performing base metal over the quarter and indeed 2025 (17.4%). Upward momentum for aluminium rose late in the year driven by concerns over future output in China (the largest producing country), with a self-imposed capacity ceiling of 45.5Mt expected to be reached in 2026. Meanwhile in Europe, disappointing output over the last several years was further challenged by the temporary outage of Century Aluminum’s Grundartangi smelter in Iceland (with two-thirds of production offline over the next 11-12 months), alongside the shuttering of South 32’s Mozal smelter in Mozambique, due the inability to secure long-term power supply. Note, Mozambique and Iceland are the two largest importers of aluminium into the EU (<10%). In the quarter ahead while supply risks will be in view, we expect prices to come under pressure given new capacity additions in China, set against a period of domestic restocking, with downstream demand muted over the Chinese New Year period. However, on the introduction of CBAM in Europe (which may limit imports into the region), in addition to record premiums in the US, focus will remain on regional inventory availability, muddying a clear market trend. Furthermore, LME benchmark prices are likely to be driven by movements in copper, with speculative net longs at their highest level on record.

LME 3M Nickel Price Performance 5Y

Source: Bloomberg

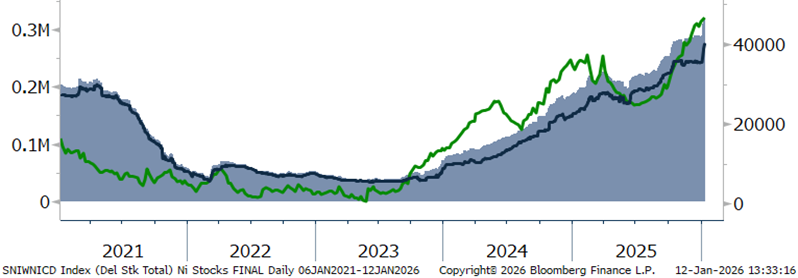

Visible Exchange Stocks

Source: Bloomberg

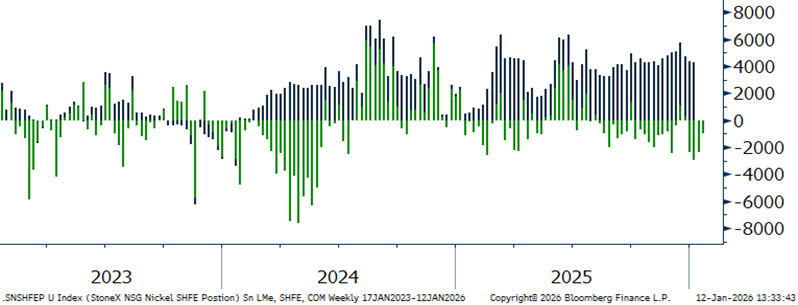

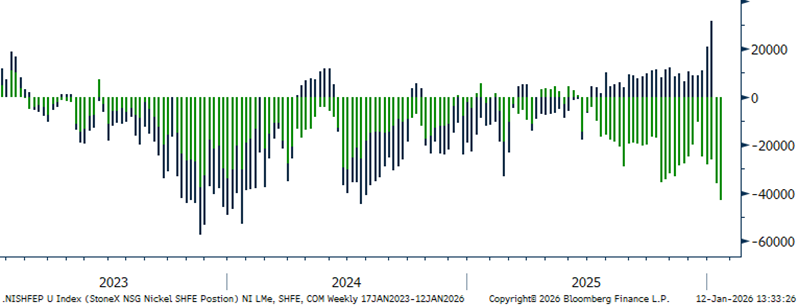

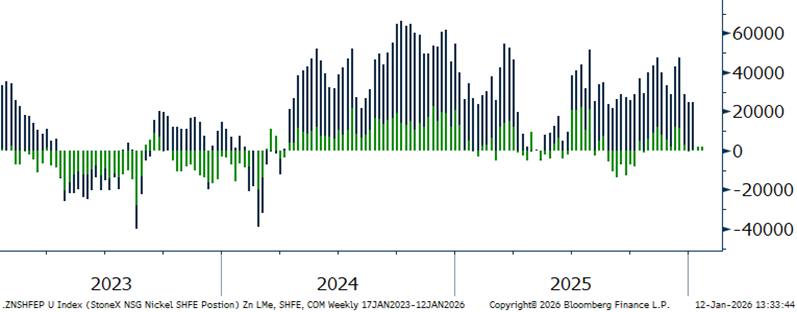

LME & SHFE Net Positions

Source: Bloomberg

Nickel completed 2025 as the third weakest performing base metal, rising 8.6% Y/Y, reversing declines over the previous two-year period, with gains concentrated solely in December on Indonesia supply risks. However, despite nickel hovering below $15,600/t over the majority of H2 (putting increasing pressure on both mine and smelter profitability, especially ex-Indonesia), this has not been enough to prevent refined output posting a record high in 2025. In turn; this, alongside the LME’s fast-tracking of Chinese and Indonesia brands has led to global refined stocks jumping 56% in 2025, pushing global visible inventory to its highest level since 2018.

LME 3M Zinc Price Performance 5Y

Source: Bloomberg

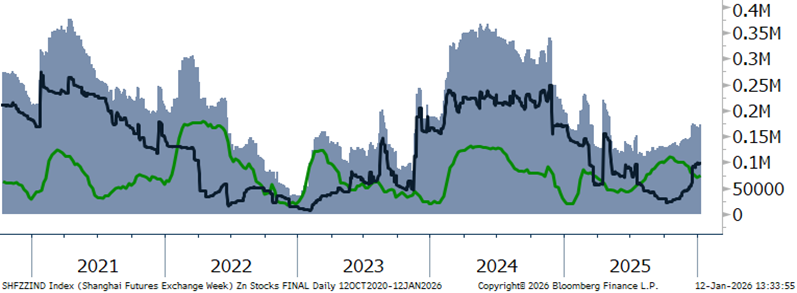

Visible Exchange Stocks

Source: Bloomberg

LME & SHFE Net Positions

Source: Bloomberg

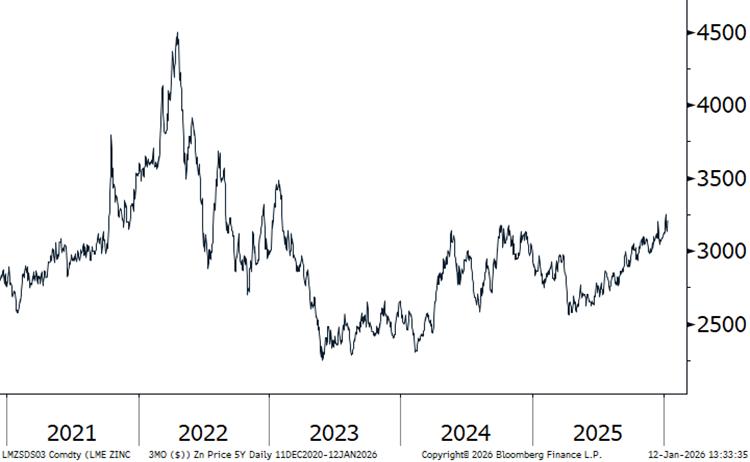

Zinc closed 2025 as the second weakest performing base metal (+4.7%), with price softness versus the rest of the suite driven by frail demand dynamics with the outlook for zinc’s largest end-use in galvanizing steel (e.g. contruction), under pressure from an ailing property market in China and downgrades to global growth due to tariff implementation, limiting advanced economy demand. In addition, robust mine supply has negatively impacted investor sentiment for zinc, easing a significantly tight supply profile over the 2022-2024 period. We forecast that zinc will transition out of a deficit market this year to post building surpluses in the years ahead with upward momentum in Q1 to face headwinds from global stock rebalancing, and an expected conclusion on the EO investigation under Section 232 into critical minerals, holding the potential to prevent further imports of refined material into the US.

LME 3M Lead Price Performance 5Y

Source: Bloomberg

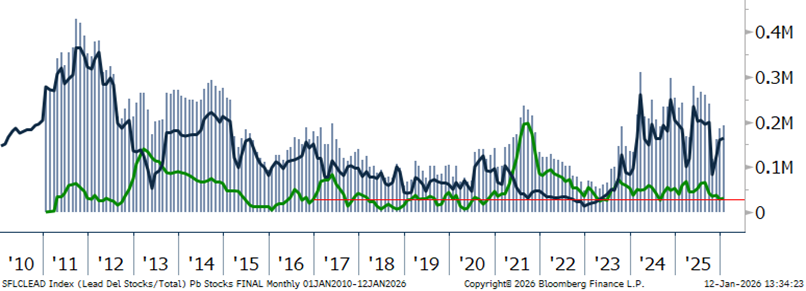

Visible Exchange Stocks

Source: Bloomberg

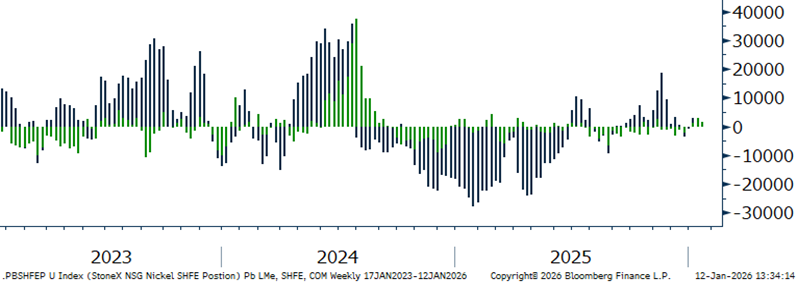

LME & SHFE Net Positions

Source: Bloomberg

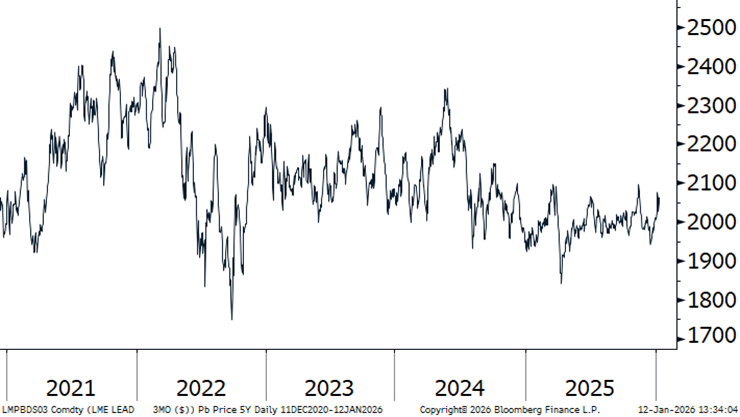

Lead ended 2025 up 3.0% Y/Y, reflecting a moderate backdrop for traditional industrial metal demand, set against a somewhat protected supply outlook, given lead’s unique fundamentals in which two-thirds of supply comes from secondary sources. Looking at Q1, with global stocks remaining at levels over the last two years, in addition to a building a global surplus, lead is likely to remain within its annual trading range, with upward momentum associated to moves in copper.

This material should be construed as market commentary and represents the opinions and viewpoints of the author, and does not reflect tailored advice associated with any specific account.

The views are current only through the date stated and are subject to change at any time based upon market or other conditions, and StoneX Group Inc. (“SGI”) disclaims any responsibility to update such views. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. Past performance does not guarantee future results.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided.

References to certain OTC products or swaps are made on behalf of StoneX Markets, LLC (SXM), a member of the National Futures Association (NFA) and provisionally registered with the U.S. Commodity Futures Trading Commission (CFTC) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ and who have been accepted as customers of SXM.

StoneX Financial Inc. (SFI) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (SEC) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Advisor. StoneX Financial (Canada) Inc. (SFCI) is registered in Canada and is a member of CIRO and CIPF. References to certain securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to certain exchange-traded futures and options are made on behalf of the FCM Division of SFI. Wealth Management is offered through SA Stone Wealth Management Inc., member FINRA/SIPC, and SA Stone Investment Advisors Inc., an SEC-registered investment advisor, both wholly owned subsidiaries of SGI.

R.J. O’Brien & Associates, LLC (RJO) is registered with the CFTC as a Futures Commission Merchant and is a member of NFA.

StoneX Financial Ltd (SFL) is registered in England and Wales, company no. 5616586. SFL is authorized and regulated by the Financial Conduct Authority (FCA) (registration number FRN:446717) to provide services to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorized to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorized and regulated by the FCA under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorized by the FCA.

This communication is issued in the European Economic Area by StoneX Financial Europe GmbH (SFEG). StoneX is the trade name used by STONEX GROUP INC. and all its associated entities and subsidiaries. StoneX Financial Europe GmbH (“SFEG”) is a securities trading firm registered in Germany under Company No. HRB 80844.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism. SAP is an “Approved International Trading Company” authorized to act as a “Spot Commodity Broker” under the Commodity Trading Act.

StoneX Financial Pte Ltd (Co. Reg. No 201130598R) (“SFP”) is regulated by the Monetary Authority of Singapore and is a Capital Markets Service Licence holder (for dealing in capital market products), an Exempt Financial Adviser (for advising on investment products and issuing or promulgating analyses/ reports on investment products) and a Major Payment Institution (for domestic and cross-border money transfer services).

SFP may distribute analysis/report produced by its respective foreign affiliates within the StoneX Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations Recipients should contact SFP at (65) 6309 1000 for any matters arising from, or in connection with, this webinar.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism.

StoneX Financial (HK) Limited (CE No.: BCQ152) (“SHK”) is regulated by the Hong Kong Securities and Futures Commission for Dealing in Securities and Dealing in Futures Contracts.

StoneX Financial Pty Ltd (ACN 141 774 727) holds an Australian Financial Service License (AFSL: 345646) for Dealing in Securities, Exchange-Traded Derivatives Contracts, OTC Derivatives Contracts and Foreign Exchange Contracts, and is regulated by the Australian Securities and Investments Commission.

StoneX Securities Co., Ltd. (“SSJ”) (Co. Reg. No 010401047199) is regulated by the Japanese Financial Services Agency as a Type-I Financial Instruments Business Operator (Kanto Local Finance Bureau (FIBO)No.291’), is a member of the Financial Futures Association of Japan for dealing and broking FX and FX Option transactions, and is a member of the Japan Securities Dealers Association for dealing and broking stock indices and option transactions.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

The report/analysis herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

© 2026 StoneX Group Inc. All Rights Reserved.