We have put together the top five questions that we have been asked over the last six months regarding the copper market:

-

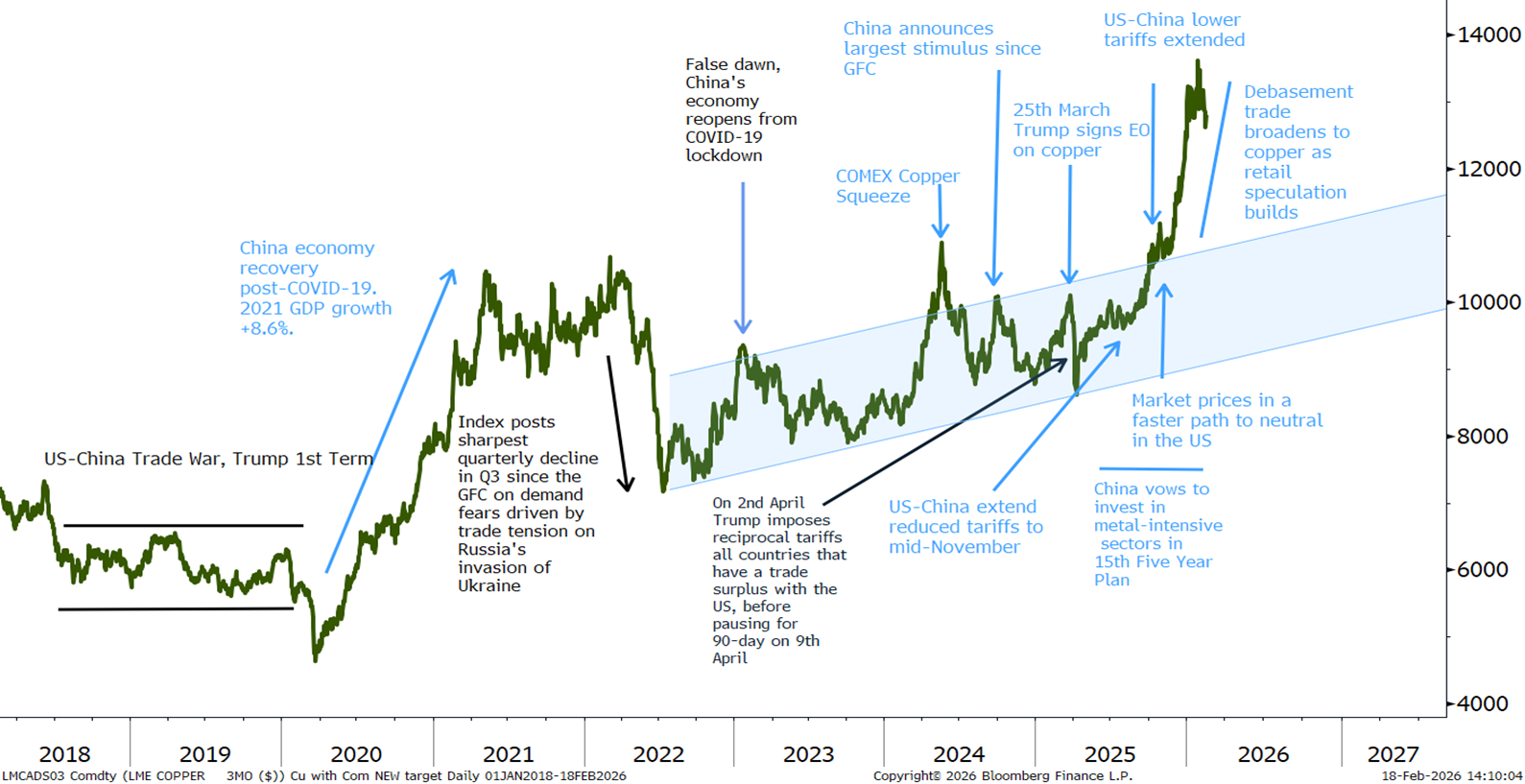

What is driving the current rally?

In the most simplistic terms, the copper market is benefiting from two main drivers.

Firstly, we have a backdrop of supportive structural fundamentals, which are being exaggerated on the back of global policy moves towards strategic stockpiling.

Secondly, we are seeing copper benefit from a wider financial market move, in the form of a debasement trade, in which we can see a growing appetite to hold precious metals, spilling over into copper.

Copper LME 3M Long-Term Chart & Key Drivers

Source: Bloomberg, StoneX

So, if we break down these two main drivers:

Starting with copper’s supportive structural fundamentals

Copper has an attractive long-term outlook. On the supply side, a lack of investment in mining over the last decade, coupled falling ore grades, social and political unrest and the reality that its takes ~17 years to bring on a copper mine from first discovery to first metal production, has left the copper supply outlook highly constrained, with risks to the upside. Meanwhile, copper’s demand outlook continues to grow legs, with copper historically already known for its universal application in the industrial world, it is now a leading metal utilized in the transition to green energy and electrification. As a result of this, copper is set to face a building deficit market in the future.

Source: Bloomberg, StoneX

Source: Bloomberg, StoneX

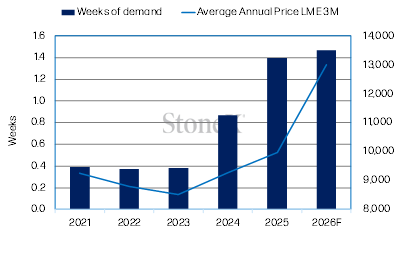

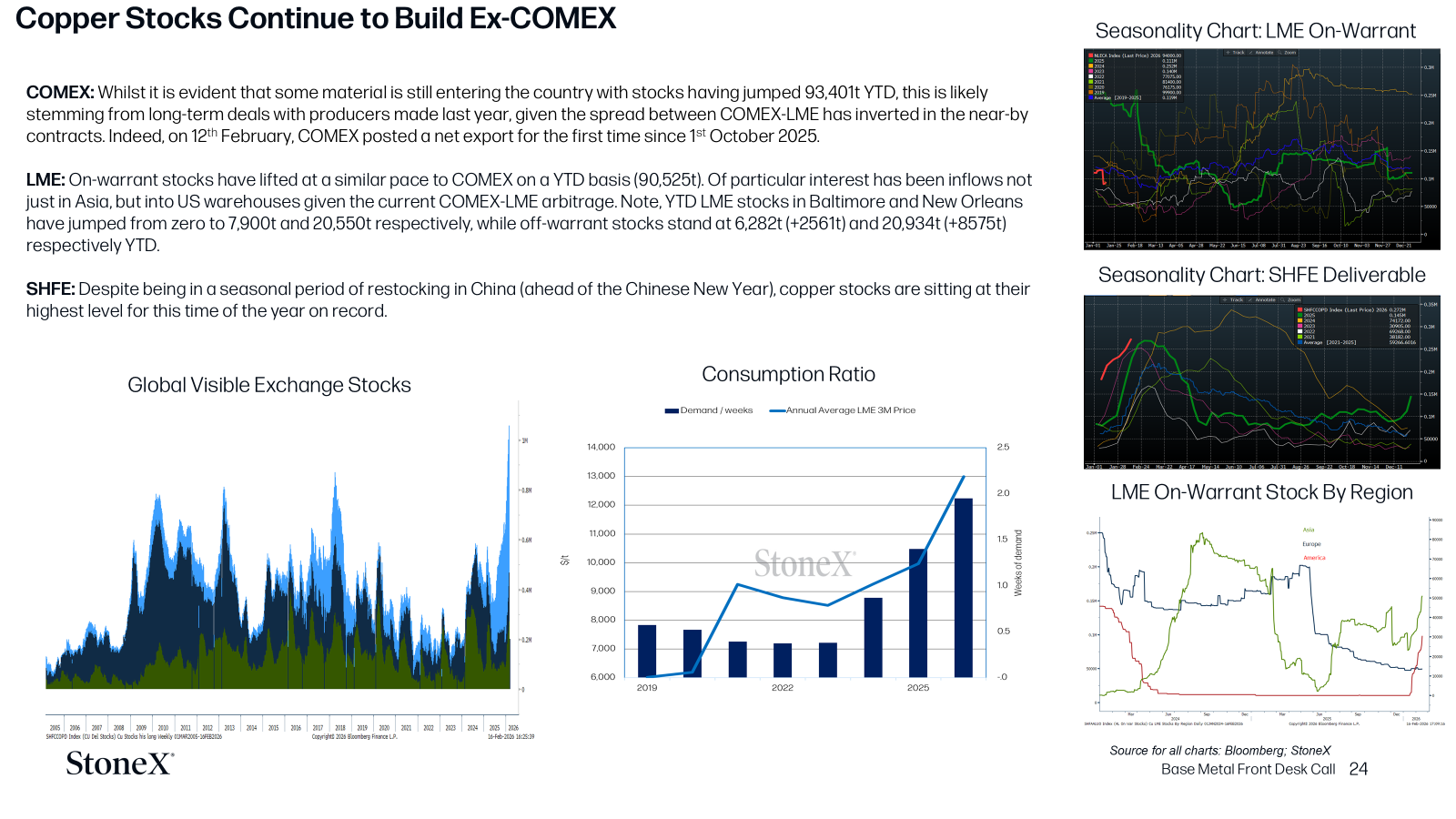

Market Balance

Source: Bloomberg, StoneX

Consumption Ratio

Source: Bloomberg, StoneX

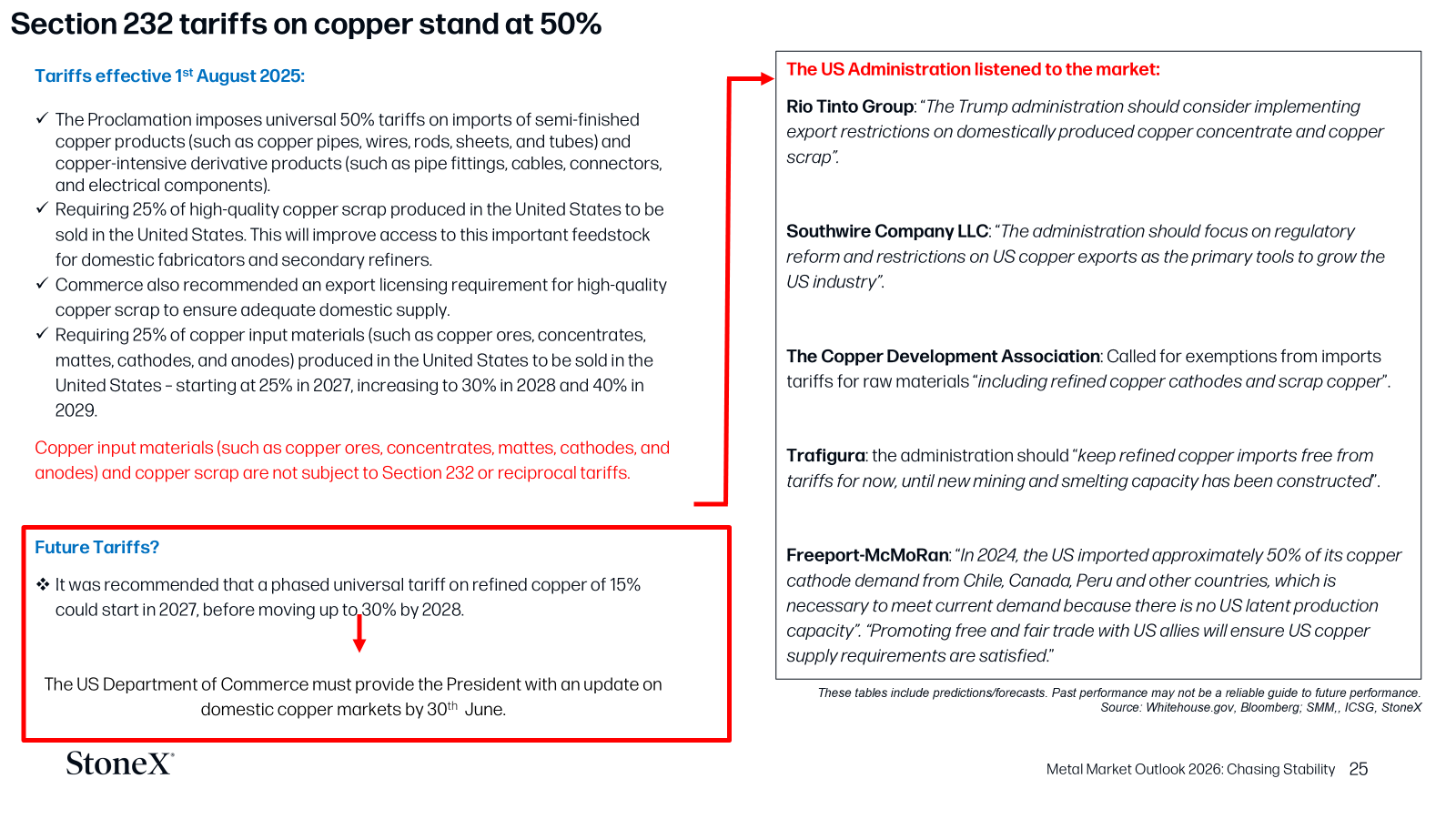

In addition to this backdrop, the last 14 months have introduced another bullish parameter to the fundamentals, in the form of policy-driven strategic stockpiling. Front and center to this has been the US, which imposed 50% tariffs on semi-finished and finished copper products entering the country from 30th June, while a decision over tariffs on refined copper (to start in 2027) is set to be decided this year. Speculation over the timing and type of tariffs up-ended the copper market in 2025, with more than 1.1Mt of copper entering the US, tightening available above-ground supplies ex-US, with material still being sent into the country at the start of this year.

Source: Bloomberg, StoneX

Looking at the second key bullish driver for copper at present, it is coming from the spill over to hold alterative hard assets like gold.

Now here, the copper market is no stranger to being influenced at times by the speculative market, in which market participants can bet on copper’s price direction across the exchanges. Indeed, we have a perfect example of this type of involvement in the copper market in H1 2024, when investors piled into copper gross long positions on the LME and COMEX, taking COMEX net longs to a record high, and in turn prices (at that time). The reasoning during this period was attached once again to copper’s long-term fundamental outlook but was further encouraged by a series of mine supply disruptions and headlines surrounding copper’s use in AI. However, the speed of price gains and this sudden FOMO in positioning pointed to the reality that copper prices at $11,000/t were unjustifiable simply on a macroeconomic and fundamental basis at that time and it was no surprise that this market move was short-lived with copper prices averaging just $9,390 over H2.

However, this time around, we are in a different situation, in which a building debasement trade is making physical alternative hard assets like gold and silver highly attractive, and we are seeing a spill over into copper, with all three metals posting a nominal high in the same calendar year (2025) for the first time since 1980.

-

Are we in a metal Supercycle?

If we just start with the definition of a Supercycle?

A commodity Supercycle, refers to a long-lasting phase (often decades) in which commodity prices, particularly metals and energy, stay significantly above their long-run trend, driven by sustained global demand outpacing supply capacity. These prolonged movements are identified through historical price cycles and reflect deep structural shifts in the global economy rather than short-term market fluctuations.

So given this, in our view the answer here is no, we are more likely in a structural tightening regime, with current metal price peaks being financially driven, with retail investors amplifying the move on the back of uncertain US policy.

In the case of copper, there are arguments to support long term higher prices, given its use in the energy and digital transition, underinvestment in mining and the fact that copper has become a strategic alternative asset, on the back of it being included as a critical mineral in the US. We cannot ignore the reality that global growth projections are mediocre at best, we are facing a structural slowdown in Chinese growth (the world’s largest consumer of copper) in addition to the reality that current global stock levels for copper are at multi-decade highs.

-

What risks are contained in the outlook for copper?

Looking across the year, we see prices for copper above $13,000/t as unsustainable with downwards pressure likely to come from

- The very real potential that no tariffs are imposed on refined copper from the US. The CME-LME arbitrage is pricing in only a 3% chance for tariffs by year-end. Therefore, in the absence of an attractive premium, we do not expect the same level of inflow as last year. Having said this, it is evident some material is entering the country still, likely to stem from long-term deals with producers made last year.

- We see speculative positioning overdone and unrelated to the realities in the market, especially given the influx of retail investors.

- The seasonally late start to the Chinese New Year has negatively impacted demand while allowing healthy restocking.

- Meanwhile, the high price of copper is directly hurting consumption, with the Yangshan premium having touched an 18-month low in January, while deliverable stocks on SHFE are at their highest level for this time in the year on record. Furthermore, even Chinese scrap is facing weak demand, despite the significant economic advantages given its price differential.

- Taking a step back, Chinese demand is forecast to slow in the year ahead, with front-loading ahead of the end of the 14th Five Year plan (in 2025) set to see only a few growth areas this year. Note, demand from the four largest sectors of demand (accounting for 81% of total demand) power, transportation, home appliances and contruction will only lift 0.7% in 2026, down from 2.6% in 2025. China accounts for 58% of global demand.

- Finally, we cannot ignore that the macro-economic outlook is full of risks with ongoing conflicts in the Middle East, no end in sight for the Russian-Ukraine war and the unpredictable nature of US policy and regulations, which continue to inflame tensions with China. Note, historically we see an elevation in geopolitical tensions as holding a net negative for base metals.

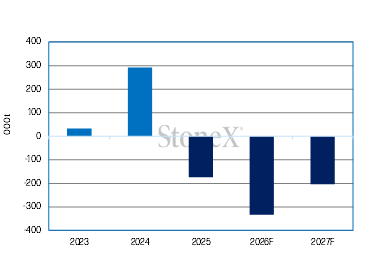

Overall, while there is no denying copper is facing significant risks to supply, with the market in a building deficit of 333,000t in 2026 from 174,000t in 2025, this is still not enough to justify copper prices at these levels and when prices correct, we expect it to be sharp and significant. Investor positioning will by the key area to watch – and profit taking is already taking place.

Source: Bloomberg, StoneX

-

How significant is AI demand on copper in reality?

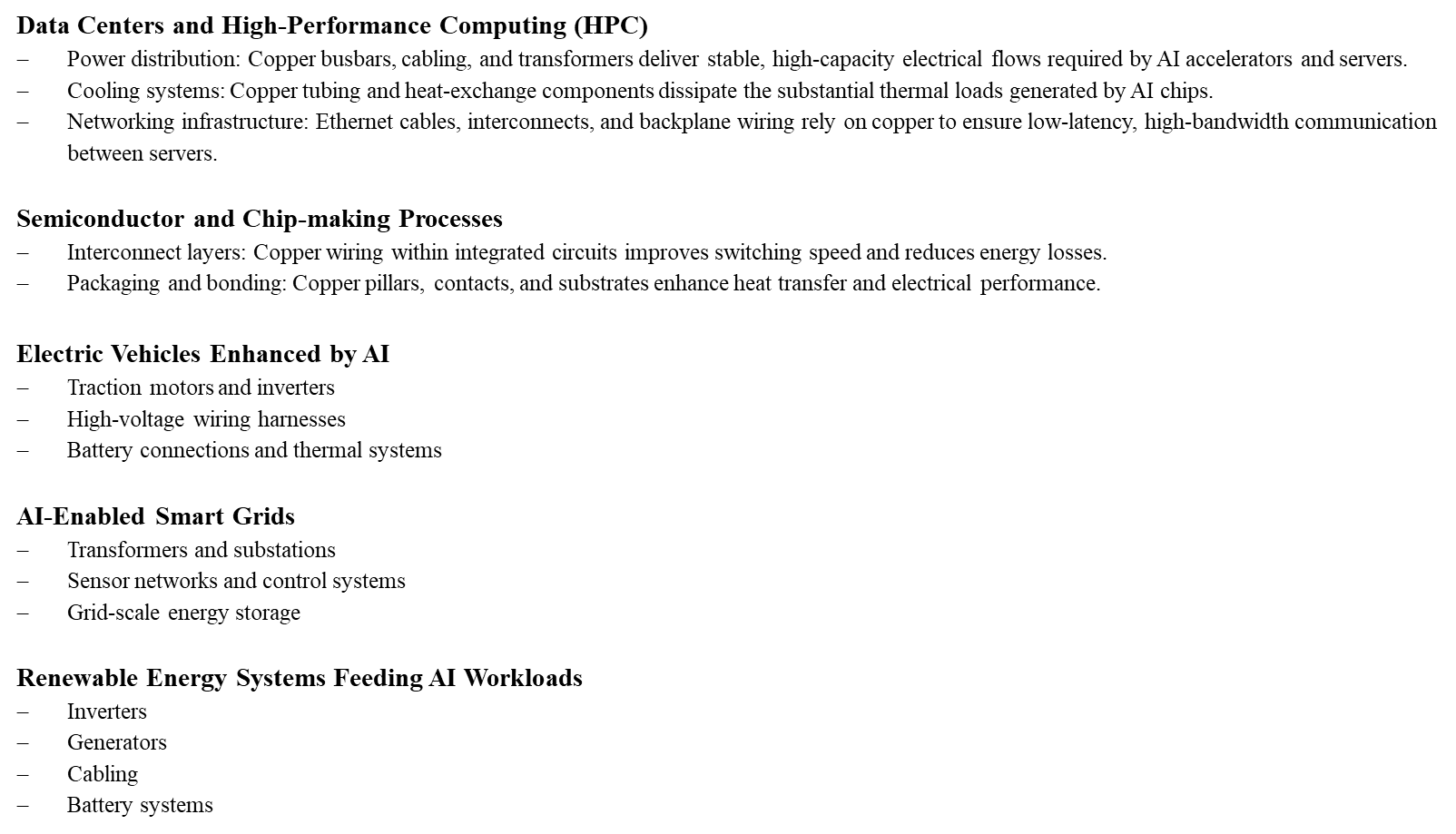

So, all in all, copper’s use is deeply embedded in AI demand, and its ecosystem in infrastructure build outs, electrification of transport and modernization of power grids (renewable energy).

However, we the % of copper demand is very small by end-use market.

The most bullish case is for 1-2Mt of copper demand a year from AI by 2030, while lower estimates range from 500-600,000t. As it stands its less than 1.5% of total copper demand in 2026.

Copper Uses in Artificial Intelligence

Source: Bloomberg, StoneX

-

What is the technical picture showing us?

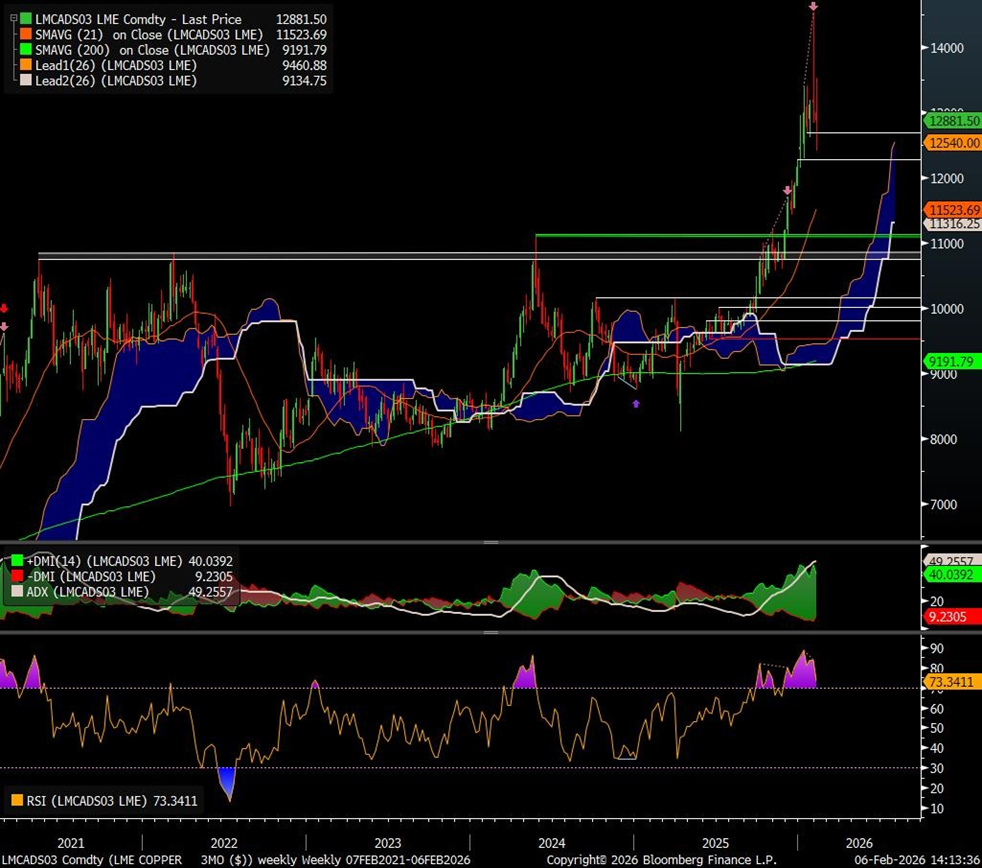

On a weekly basis, copper remains firmly bullish from a technical perspective. Price continues to trade above all major moving averages, with the broader structural uptrend intact. The first key area of support is located around $12,300/t; a decisive break below this level would likely open the door for a deeper retracement toward $11,500/t.

While the price holds above the $11,000t region, the broader bullish bias remains unchanged. A sustained selloff below $10,100/t would be required to materially challenge the bullish outlook and shift the technical view to bearish.

That said, momentum indicators are currently elevated, and historical studies suggest this increases the probability of a corrective pullback in the near term. As such, while the medium-to-long term trend remains constructive, price action is consistent with a developing corrective phase rather than trend reversal.

Copper LME 3M Price

Source: Bloomberg, StoneX

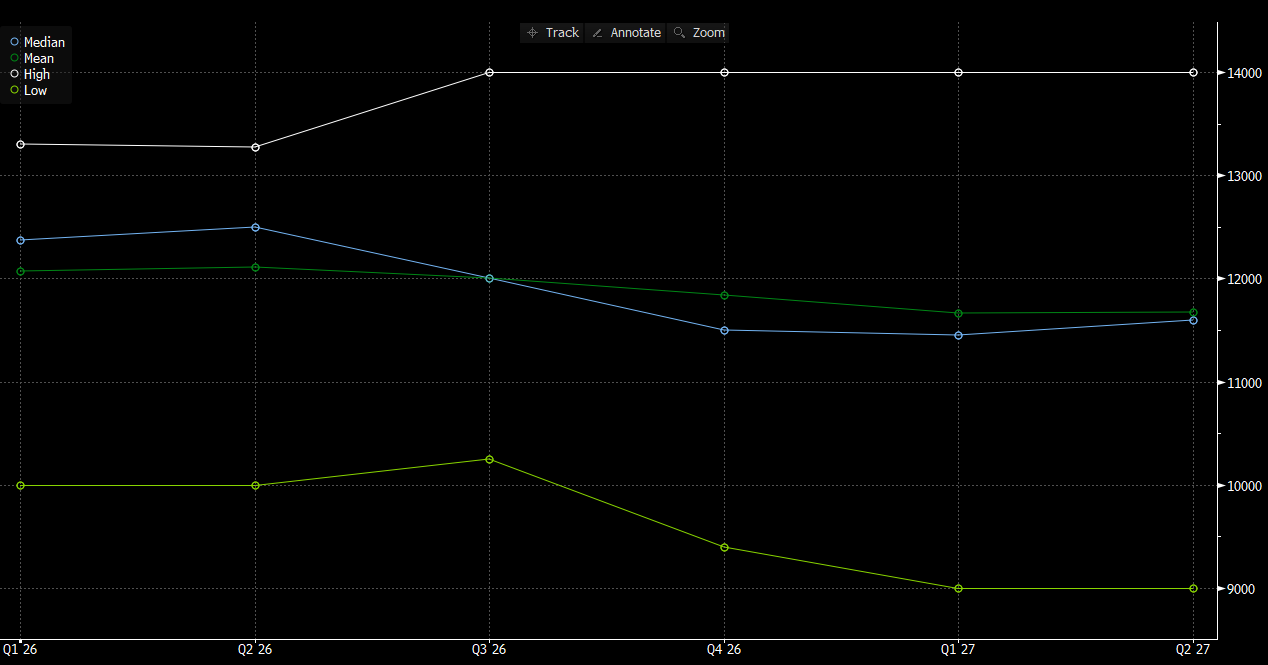

LME 3M Copper Price Forecasts - Industry Averages

Source: Bloomberg, StoneX

This material should be construed as market commentary and represents the opinions and viewpoints of the author, and does not reflect tailored advice associated with any specific account.

The views are current only through the date stated and are subject to change at any time based upon market or other conditions, and StoneX Group Inc. (“SGI”) disclaims any responsibility to update such views. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. Past performance does not guarantee future results.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided.

References to certain OTC products or swaps are made on behalf of StoneX Markets, LLC (SXM), a member of the National Futures Association (NFA) and provisionally registered with the U.S. Commodity Futures Trading Commission (CFTC) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ and who have been accepted as customers of SXM.

StoneX Financial Inc. (SFI) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (SEC) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Advisor. StoneX Financial (Canada) Inc. (SFCI) is registered in Canada and is a member of CIRO and CIPF. References to certain securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to certain exchange-traded futures and options are made on behalf of the FCM Division of SFI. Wealth Management is offered through SA Stone Wealth Management Inc., member FINRA/SIPC, and SA Stone Investment Advisors Inc., an SEC-registered investment advisor, both wholly owned subsidiaries of SGI.

R.J. O’Brien & Associates, LLC (RJO) is registered with the CFTC as a Futures Commission Merchant and is a member of NFA.

StoneX Financial Ltd (SFL) is registered in England and Wales, company no. 5616586. SFL is authorized and regulated by the Financial Conduct Authority (FCA) (registration number FRN:446717) to provide services to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorized to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorized and regulated by the FCA under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorized by the FCA.

This communication is issued in the European Economic Area by StoneX Financial Europe GmbH (SFEG). StoneX is the trade name used by STONEX GROUP INC. and all its associated entities and subsidiaries. StoneX Financial Europe GmbH (“SFEG”) is a securities trading firm registered in Germany under Company No. HRB 80844.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism. SAP is an “Approved International Trading Company” authorized to act as a “Spot Commodity Broker” under the Commodity Trading Act.

StoneX Financial Pte Ltd (Co. Reg. No 201130598R) (“SFP”) is regulated by the Monetary Authority of Singapore and is a Capital Markets Service Licence holder (for dealing in capital market products), an Exempt Financial Adviser (for advising on investment products and issuing or promulgating analyses/ reports on investment products) and a Major Payment Institution (for domestic and cross-border money transfer services).

SFP may distribute analysis/report produced by its respective foreign affiliates within the StoneX Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations Recipients should contact SFP at (65) 6309 1000 for any matters arising from, or in connection with, this webinar.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism.

StoneX Financial (HK) Limited (CE No.: BCQ152) (“SHK”) is regulated by the Hong Kong Securities and Futures Commission for Dealing in Securities and Dealing in Futures Contracts.

StoneX Financial Pty Ltd (ACN 141 774 727) holds an Australian Financial Service License (AFSL: 345646) for Dealing in Securities, Exchange-Traded Derivatives Contracts, OTC Derivatives Contracts and Foreign Exchange Contracts, and is regulated by the Australian Securities and Investments Commission.

StoneX Securities Co., Ltd. (“SSJ”) (Co. Reg. No 010401047199) is regulated by the Japanese Financial Services Agency as a Type-I Financial Instruments Business Operator (Kanto Local Finance Bureau (FIBO)No.291’), is a member of the Financial Futures Association of Japan for dealing and broking FX and FX Option transactions, and is a member of the Japan Securities Dealers Association for dealing and broking stock indices and option transactions.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

The report/analysis herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

© 2026 StoneX Group Inc. All Rights Reserved.