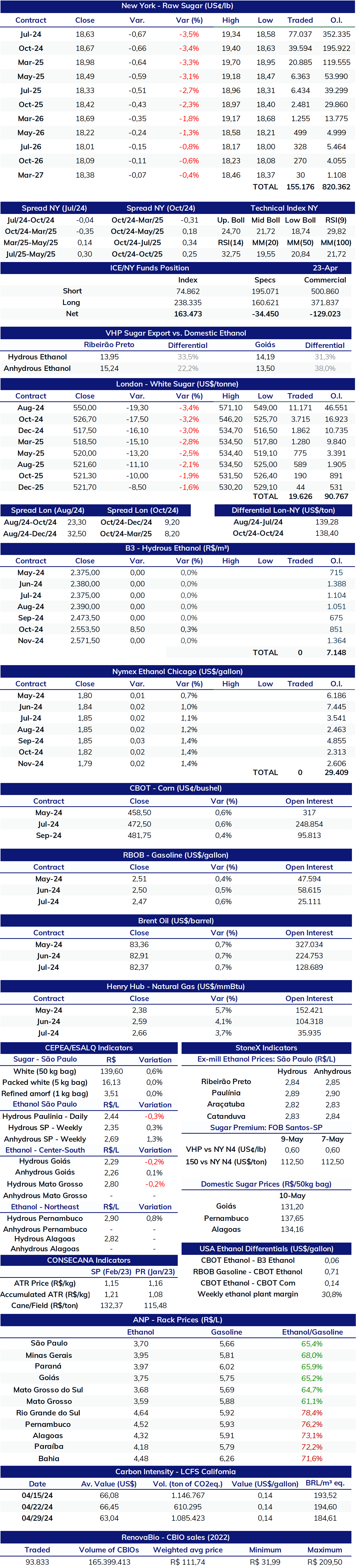

Hydrous ethanol prices on the physical market in the state of São Paulo maintained their support amid competitive parity and strengthened demand. After rising sharply since the beginning of April, last week saw stability, maintaining the values traded in the previous week, with the fuel ranging from BRL 2.80/liter to BRL 2.85/liter.

Ex-mill hydrous ethanol price - Ribeirão Preto/SP - (BRL/liter)

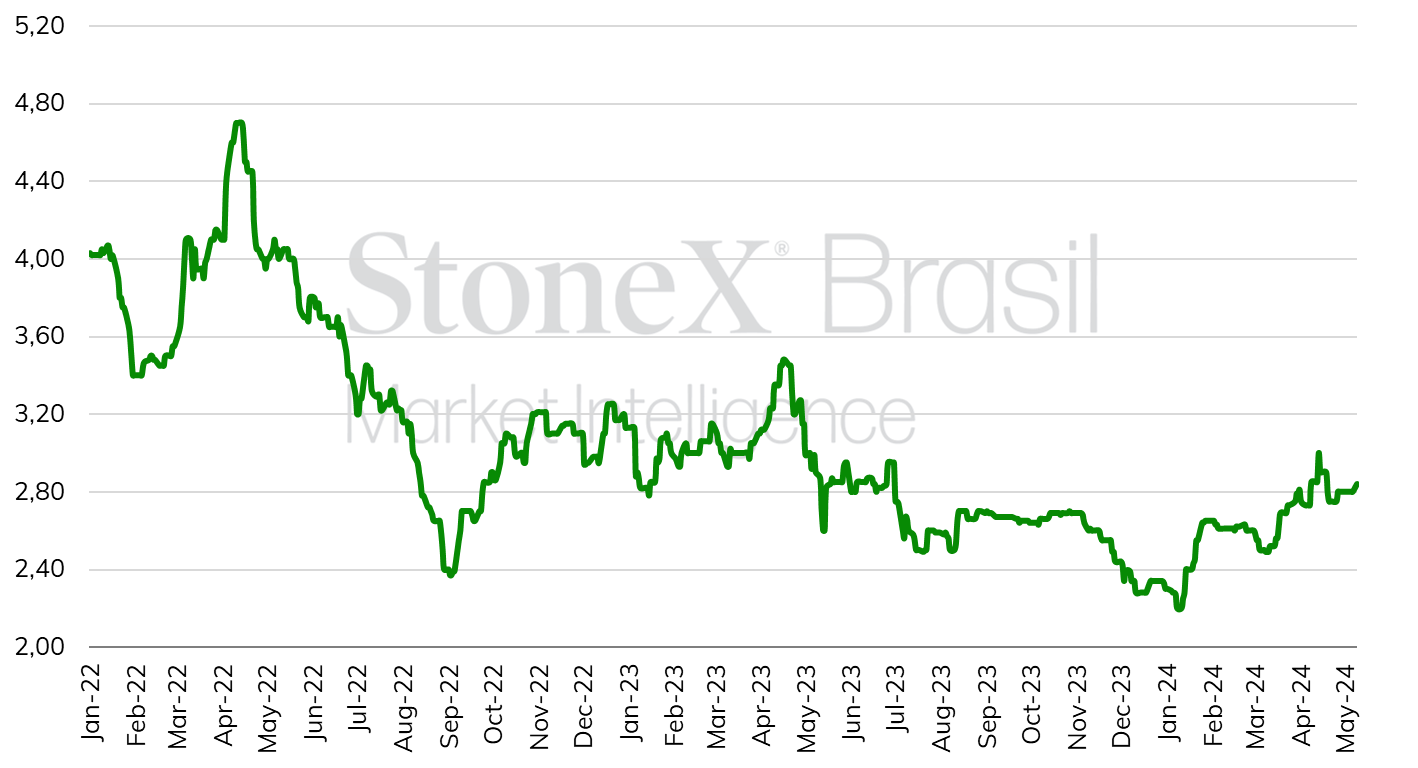

On the resale side, the biofuel also did not register a significant variation in the weekly average, closing at BRL 3.70/liter in São Paulo, therefore maintaining a parity of around 65%. Within the Center-South states, the ones with parity below 70% are: Minas Gerais (67.9%), Mato Grosso (61.6%), Goiás (65.7%), Paraná (66%) and Mato Grosso do Sul (65.1%).

Parity between ethanol and gasoline in the state of São Paulo (%)

Source: ANP. Design: StoneX.

Source: ANP. Design: StoneX.

Despite the strengthening of demand due to the start of the 2024/25 crop (Apr-Mar) in the Brazilian Center-South continuing to increase the biofuel supply, prices should remain under downward pressure, limiting further increases by the mills. This is because stocks ended the harvest at high levels and there is an expectation of a still voluminous crop, albeit smaller. StoneX estimates point to a crushing volume of 602.2 million tonnes during the 2024/25 cycle (Apr-Mar) in the Center-South.

Analyzing the outlook for ethanol pricing, it is estimated that the parity in the state of São Paulo should continue to favor ethanol in the coming months, remaining between 64% and 66% until August. After this period, with a reduction in sugar cane crushing and consequently a drop in ethanol supply under still strong consumption, the parity should gradually increase until it exceeds the 70% mark in November/24.

As a result, consumption is expected to remain high until September. StoneX estimates that the hydrous share should grow by around 3.0 percentage points in the 2024/25 crop compared to the previous season, totaling 29%. As a result, consumption is estimated at 18.4 million m³ in the Center-South, an annual increase of 13.6%. Anhydrous consumption is expected to total 8.5 million m³, an annual decrease of 2.7%.

Daily recap

On Monday (13), the prices of raw and white sugar recorded a day of retraction on the futures markets. The most active contract for raw #11 SBN4 ended the day at US¢ 18.63/lb (-3.47%), while the equivalent contract for white #5 ended at US$ 550.0/t (-3.39%). Directing the market, it is worth mentioning the influence of a more abundant outlook on the supply side. StoneX estimates a global sugar surplus of 3.9 million tonnes in 2023/24 (Oct-Sept) and, for the next cycle, the outlook is that the scenario will remain at positive levels, which would lead to a 2024/25 balance of 2.5 million tonnes with a recovery in production by international players and a still high supply of sugar in the Brazilian Center-South.