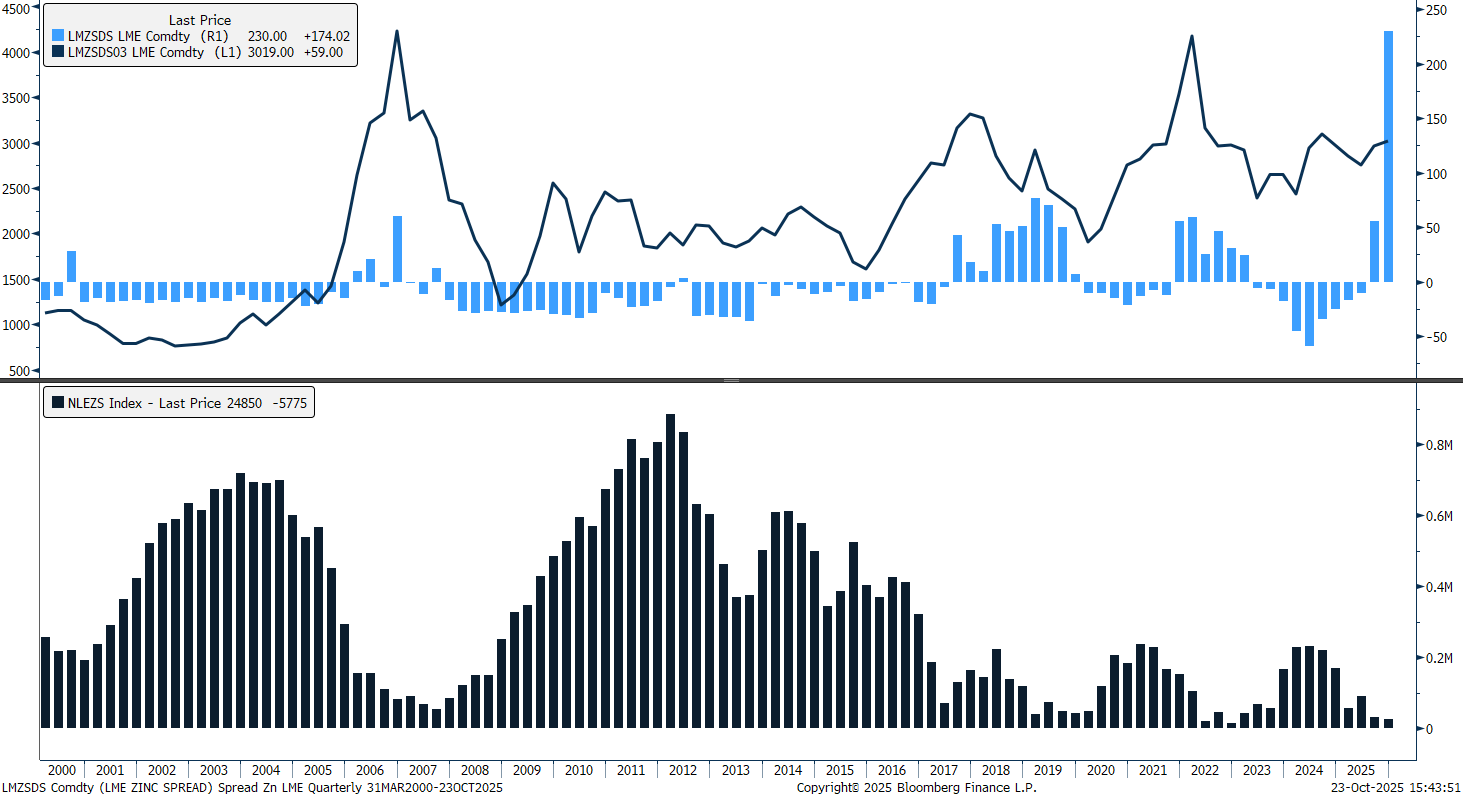

Until very recently, zinc has held the positions as the weakest performing base metal in 2025, with loosening fundamentals and low investor interest limiting price gains on a global basis. However, over the last quarter, the outlook for zinc has altered, and it was the best performing base metal in Q3. This is being driven by regional parameters, with a sacristy of units in Europe, steady demand in Asia-Ex-China and a high premium for units in the US (ahead of potential US tariffs), drawing zinc from Asian LME warehouses. As it stands, LME zinc’s forward curve is posting a widening backwardation out to Dec-26, with the LME-3M spread having jumped to its largest backwardation on record at $320/t. In turn creating a building divergence in global zinc prices, muddying a clear market trend. In this article we address the outlook for zinc in the months and year ahead.

LME Cash-3M Spread

Source: Bloomberg, StoneX

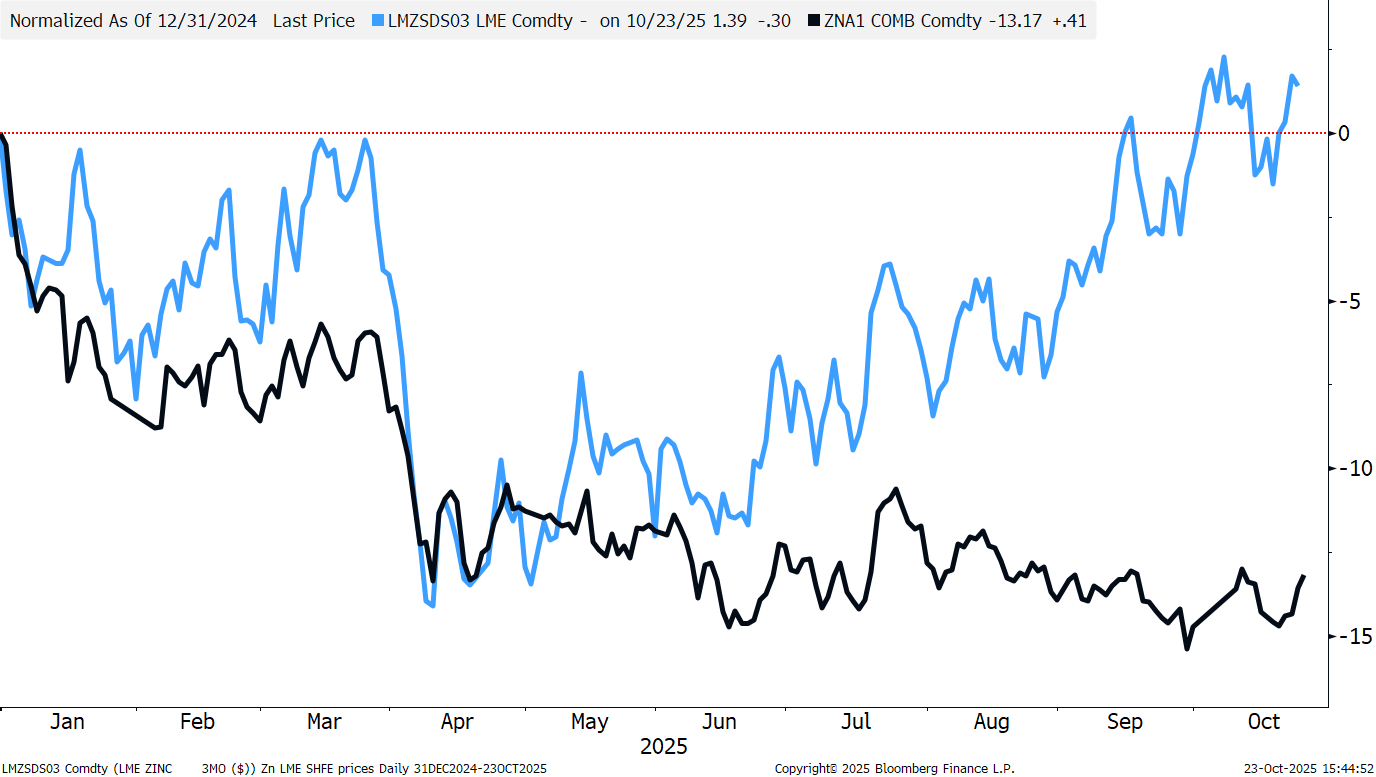

LME Versus SHFE Zinc Prices YTD

Source: Bloomberg, StoneX

LME Zinc’s Predicted Squeeze Has Materialised

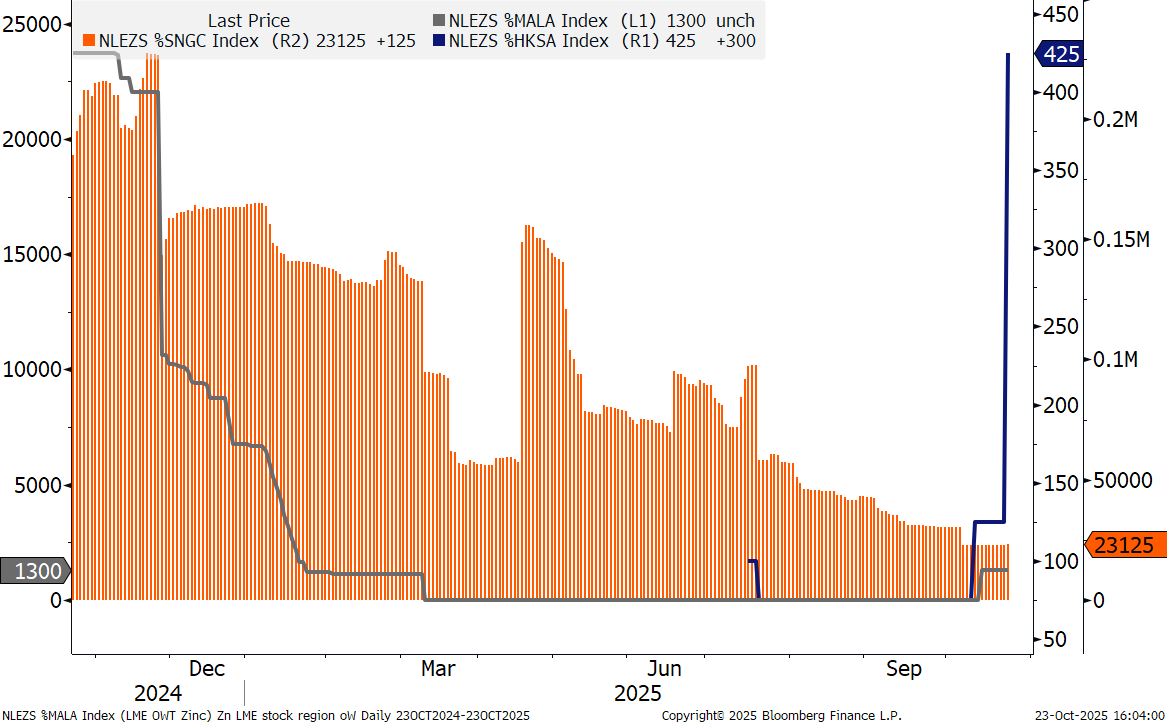

At the time of writing (22nd October), LME zinc closing stocks stand at just 35,300t, their lowest level since March 2023, having fallen by 85% YTD, covering less than one days’ worth of demand. Since mid-April, stocks have been moving consistently lower, with outflows largely stemming from Singapore warehouses, feeding real world demand in Europe and ex-Asia as smelters’ margins suffer from high energy prices and/or lack of ore availability (following three years of global mine production having been in decline over 2022-2024).

In addition to this, units are also being drawn into the US, with concerns that the outcome of the Section 232 investigation into Critical Minerals (launched in April) could result in import tariffs on zinc, in which the US has the highest import reliance on of any refined base metal, standing at 75%). With the investigation having 180 days to run, the markets are expecting an announcement this month, accelerating the desire of market participants to take advantage of highest domestic premiums, altering historical trade flow patterns.

Table of US Import Reliance of Refined Base Metals

| |

US Imports as & of Demand

|

|

Aluminium

|

82%

|

|

Zinc

|

75%

|

|

Tin

|

73%

|

|

Nickel

|

48%

|

|

Copper

|

45%

|

|

Lead

|

28%

|

Source: Bloomberg, USGS, StoneX

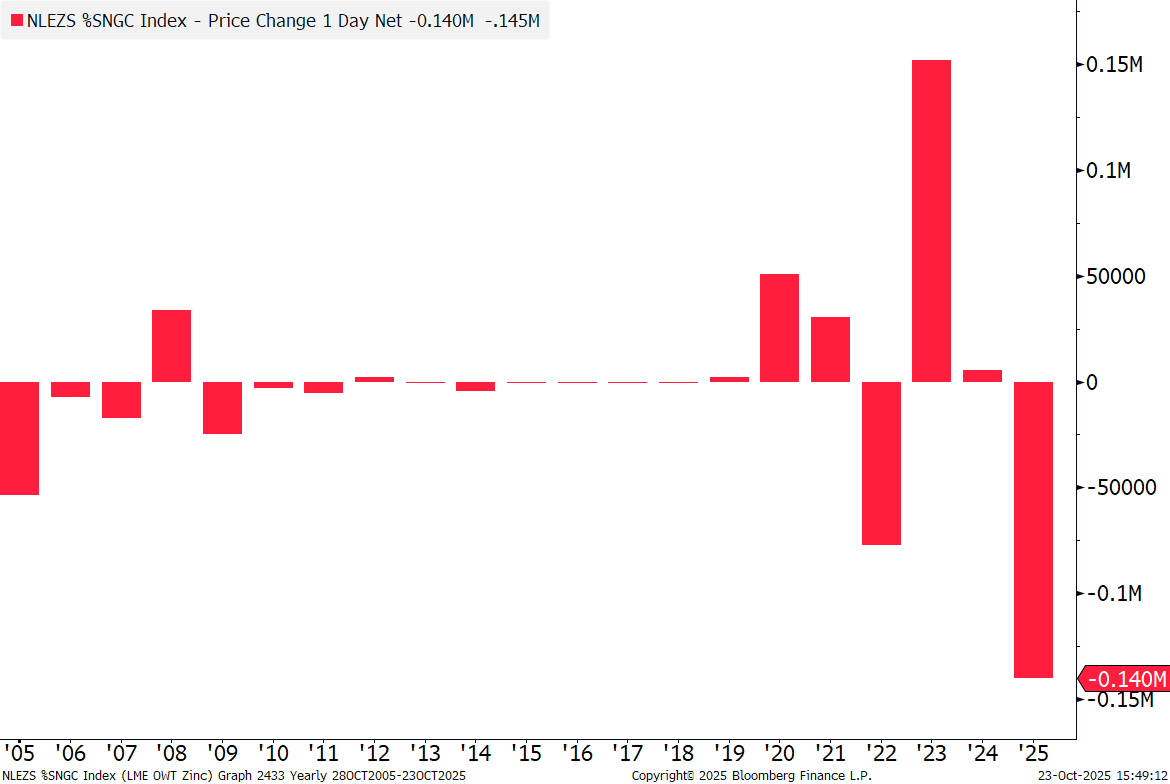

Volatile stock movements are often recorded in the zinc market, why is this time around different?

Unlike in 2024, when we saw whipsaw movements in material being cancelled and then re-warranted in LME warehouses (Singapore), in which trading houses and warehouses would engage in rent-share deals. This time around, material which has been cancelled appears not to be coming back. For example, on a YTD basis, Singapore on-warrant stocks are down 140,175t, versus a net import of 26,875t during the same period in 2024.

Zinc LME Singapore Warehouse Annual On-Warrant Stocks (Change t)

Source: Bloomberg, StoneX

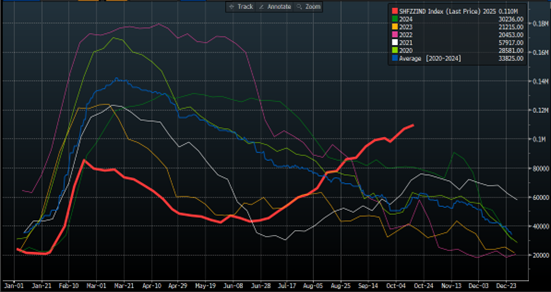

China’s View on Zinc is More Muted

The domestic view on zinc in China is more measured, with plentiful inventory (SHFE stocks well above five-year averages) and robust production (up 3.9% YTD Y/Y versus 0.8% in 2024), set against a weak outlook for zinc’s largest end-use, the contruction market. Indeed here, an acceleration in global mine production has resulted in net imports of zinc ore into China jumping to their highest level on record in September <500,000t. While imports from the US were almost non-existent given the 10% retaliatory tariffs imposed by China on US imports (impacting trade from the largest zinc mine in the world, Teck Resources Red Dog), we can see exports have risen from Australia, likely with shipments having been switched to avoid tariffs.

Seasonality Chart: SHFE On-Demand Stocks

Source: Bloomberg, StoneX

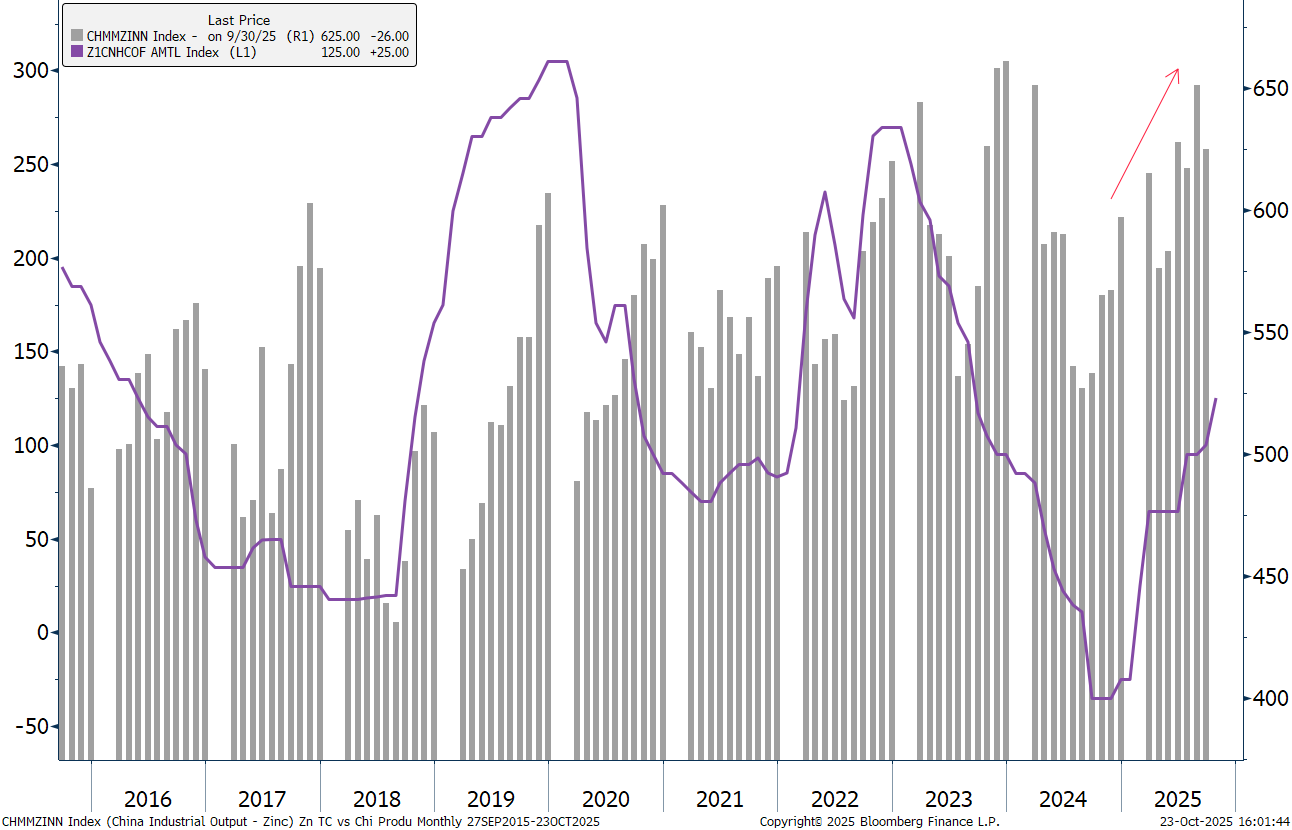

Chinese Refined Zinc Production Versus International RCTCs

Source: Bloomberg, StoneX

What would it take for the LME Zinc backwardation to soften?

- On the LME, there are six long holders with cumulative cash positions amounting to three times the quantity of stock available, if profit taking occurs, we could see material come back onto the exchange.

- Chinese smelters find the arbitrage attractive to ship material into the LME, most likely with the LME Hong Kong warehouse the first port of call (with 425t having entered warehouses at the time of writing).

- A ruling on Section 232 investigation into critical minerals, resulting in an unwinding trade to send material into the US.

In our view, we expect the tightness in the zinc market to remain until we start to see one or multiple of the above scenarios unfold, likely to keep LME prices in a tightly higher trading range ~$3,000/t.

Zinc LME Asian On-Warrant Stocks in Asian Warehouses

Source: Bloomberg, StoneX

Given this background what are our expectations for zinc prices in 2026?

Over the course of 2026, we see zinc prices pulling back from these <3,000/t levels, with increasing supply and still a modest demand outlook allowing global stock to return to more balanced levels.

Will China become a net exporter of zinc in 2026?

The last time we saw meaningful volumes of zinc exports was in 2022, in the aftermath of Russian invasion of Ukraine (where high energy prices resulted in smelter closures). In May 2022, exports spiked to 35,000t, this year they’ve averaged 1,200t a month. We do not anticipate that China will become a net exporter of refined zinc this year, especially given risks to domestic supply with country-based RCTCs weakening. Here, expanding smelting capacity set against weak domestic zinc prices (given high inventory levels and weak demand), means we could see some smelters go on care and maintenance. However, this is unlikely to be significant enough to destabilizing raw material supply chains as a whole.

Please see below our Fundamental Outlook for Zinc in 2026

Global mine supply is on track to rebound in 2025 and 2026, following three years of prior declines. This will be supported by double-digit growth in Africa (DRC’s Kipushi mine) and increasing output in Peru, China, and across Europe, Bosnia & Herzegovina (Vares operation), Ireland (resumption of operations at Tara mine in October 2024) and Russia (commission on of Ozernoye mine in September 2024).

Record Low Benchmark RCTCs to Recover on Increasing Ore Supply

In turn, this will allow refined output globally to recover in our forecasts after posting a decline in 2024. We see gains concentrated in China, in which increasing availability of zinc ore (up 45% over January-July versus a 22% decline over the same period Y/Y), is expected to help lift annual record low RCTCs this year ($80/t) towards $160/t in 2026, with current zinc prices no longer challenging smelter profitability. Note, Chinese production in August rose to a 17-month high, with the domestic market forecast to enter a surplus to year-end. In addition, the ramp up of operations in Q4 2025 of China’s Kunlun smelter is expected to add 560,000t/y of production (almost equivalent to the annual level of net imports of refined zinc into the country), although we do not expect China to become a net exporter of material.

Higher Prices Dependent on Sustained Demand, Prospects are Modest

Zinc’s significant exposure to the galvanising industry (~50%) leaves a recovery in demand vulnerable to future investment plans, particularly in major demand countries like China, Europe and the US, with demand growth in China on a deaccelerating track in traditional demand areas. With this in mind, we expect consumption to by led by demand ex-China (India and Asia Ex-China), however, uncertainty and a lack of investment decisions given a new trading landscape will remain a headwind.

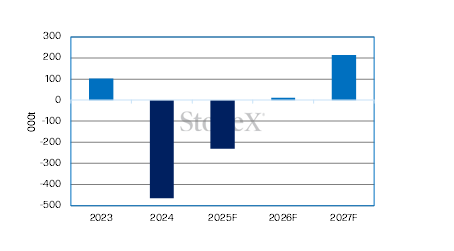

Market Balance

Source: Bloomberg, StoneX

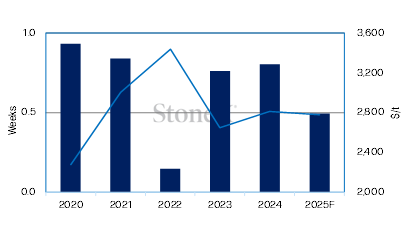

Consumption Ratio

Light blue line: LME 3M Annual Average Zinc Price. Dark Blue Bars: Consumption Ratio (total visible exchange stocks/annual demand in days).

Source: Bloomberg, StoneX

This material should be construed as market commentary and represents the opinions and viewpoints of the author, and does not reflect tailored advice associated with any specific account.

The views are current only through the date stated and are subject to change at any time based upon market or other conditions, and StoneX Group Inc. (“SGI”) disclaims any responsibility to update such views. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. Past performance does not guarantee future results.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided.

References to certain OTC products or swaps are made on behalf of StoneX Markets, LLC (SXM), a member of the National Futures Association (NFA) and provisionally registered with the U.S. Commodity Futures Trading Commission (CFTC) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ and who have been accepted as customers of SXM.

StoneX Financial Inc. (SFI) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (SEC) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Advisor. StoneX Financial (Canada) Inc. (SFCI) is registered in Canada and is a member of CIRO and CIPF. References to certain securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to certain exchange-traded futures and options are made on behalf of the FCM Division of SFI. Wealth Management is offered through SA Stone Wealth Management Inc., member FINRA/SIPC, and SA Stone Investment Advisors Inc., an SEC-registered investment advisor, both wholly owned subsidiaries of SGI.

R.J. O’Brien & Associates, LLC (RJO) is registered with the CFTC as a Futures Commission Merchant and is a member of NFA.

StoneX Financial Ltd (SFL) is registered in England and Wales, company no. 5616586. SFL is authorized and regulated by the Financial Conduct Authority (FCA) (registration number FRN:446717) to provide services to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorized to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorized and regulated by the FCA under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorized by the FCA.

This communication is issued in the European Economic Area by StoneX Financial Europe GmbH (SFEG). StoneX is the trade name used by STONEX GROUP INC. and all its associated entities and subsidiaries. StoneX Financial Europe GmbH (“SFEG”) is a securities trading firm registered in Germany under Company No. HRB 80844.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism. SAP is an “Approved International Trading Company” authorized to act as a “Spot Commodity Broker” under the Commodity Trading Act.

StoneX Financial Pte Ltd (Co. Reg. No 201130598R) (“SFP”) is regulated by the Monetary Authority of Singapore and is a Capital Markets Service Licence holder (for dealing in capital market products), an Exempt Financial Adviser (for advising on investment products and issuing or promulgating analyses/ reports on investment products) and a Major Payment Institution (for domestic and cross-border money transfer services).

SFP may distribute analysis/report produced by its respective foreign affiliates within the StoneX Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations Recipients should contact SFP at (65) 6309 1000 for any matters arising from, or in connection with, this webinar.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism.

StoneX Financial (HK) Limited (CE No.: BCQ152) (“SHK”) is regulated by the Hong Kong Securities and Futures Commission for Dealing in Securities and Dealing in Futures Contracts.

StoneX Financial Pty Ltd (ACN 141 774 727) holds an Australian Financial Service License (AFSL: 345646) for Dealing in Securities, Exchange-Traded Derivatives Contracts, OTC Derivatives Contracts and Foreign Exchange Contracts, and is regulated by the Australian Securities and Investments Commission.

StoneX Securities Co., Ltd. (“SSJ”) (Co. Reg. No 010401047199) is regulated by the Japanese Financial Services Agency as a Type-I Financial Instruments Business Operator (Kanto Local Finance Bureau (FIBO)No.291’), is a member of the Financial Futures Association of Japan for dealing and broking FX and FX Option transactions, and is a member of the Japan Securities Dealers Association for dealing and broking stock indices and option transactions.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

The report/analysis herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

© 2026 StoneX Group Inc. All Rights Reserved.