Markets Focus on US Growth and Interest Rates Amid Tariffs and Trade Wars

Talking Points:

- The top macro calendar looks to throttle back somewhat after a run of major central bank rate decisions and amid tariff headline fatigue

- Global growth will be a matter of greater prominence after the recent FOMC growth downgrades and troubling US consumer confidence data

- Rate policy will also be up for grabs in the US as the Fed’s hold looks uneasy between rising inflation threats and floundering growth trends, the PCE will be key

Sentiment seemed to stabilize this past week following an incredibly-weighty round of high profile macro event risk. With anticipation steadying the market’s hand heading into the FOMC rate decision and Chairman Powell managing to avoid any definitive outlook for what was next, the market was left to question what would be the next active macro theme to carry us forward. Despite the uncertainty surrounding unpredictable economic themes like the progress of the trade wars, there seems a reticence – perhaps a calcifying skepticism – to run on speculative interpretation alone.

Calendar of Top Global Macro Event Risk

Source: John Kicklighter

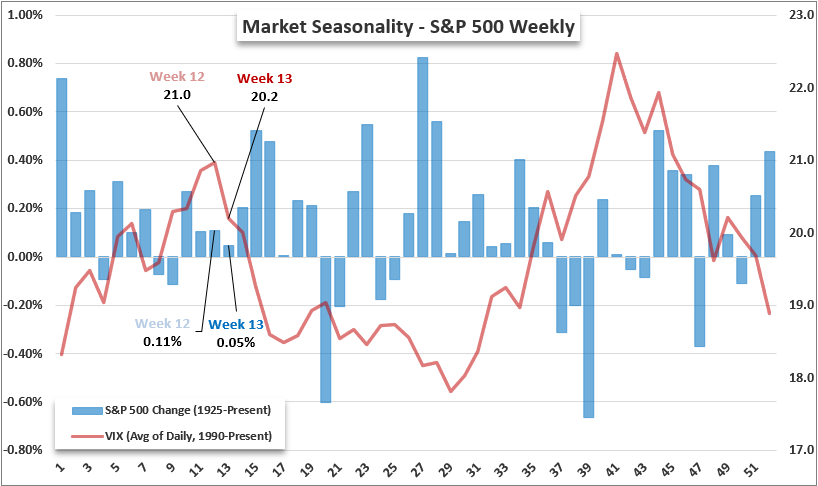

If it is indeed the case that the market will move from the headlines of reciprocal tariffs to waiting for tangible economic consequences, it would seem that we would shift attention to the more common and predictable macroeconomic themes. Those themes – like growth, monetary policy and systemic risk appetite – play out over longer periods of time. With that course, it becomes more probable that the market reverts to norms such as the seasonality trends we have seen in the past. That would be interesting given volume and volatility (at least via the benchmark S&P 500) move past their peak for the first half in the 13th week of the year.

Chart of S&P 500 Calendar Week Seasonality for Performance and Volatility, VIX (Weekly)

Source: John Kicklighter, Standard & Poor’s

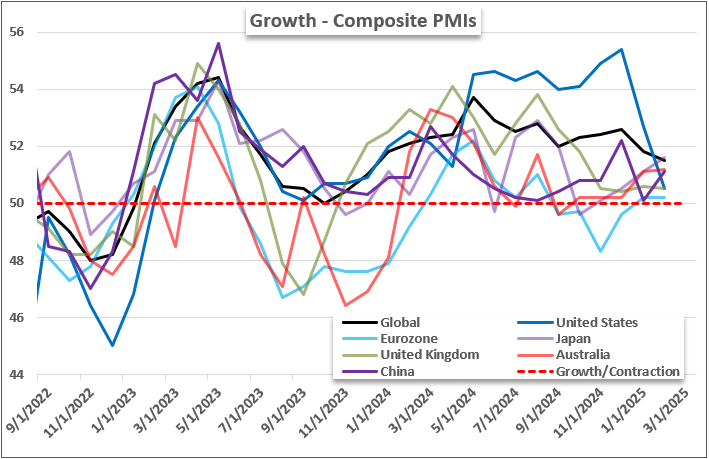

If the attention shifts back towards more traditional fundamental matters, then what should we be watching over the coming week’s docket? Economic activity seems to be at the forefront of concern as the markets weight the impact of tariffs and following the FOMC’s downgrade of US GDP. As it happens, we are due a timely update on economic activity from the largest developed economies for the month of March via the PMI.

Through the past two months, the most dramatic change came on behalf of the US economy whose composite reading dropped from above 55 as a leading powerhouse at multi-year highs to a 50.5 that was barely cracking the growth threshold. Should the reading for United States slip below the 50 threshold, there will naturally remain skepticism as to the representative easing, but the implications will be difficult to miss. Overall, output should be monitored across the spectrum. Should all of the economies move close to – much less – the 50 mark, it is far more likely that genuine risk aversion start to take hold.

Chart of Major Economy Composite PMIs (Monthly)

Source: John Kicklighter, Standard & Poor’s

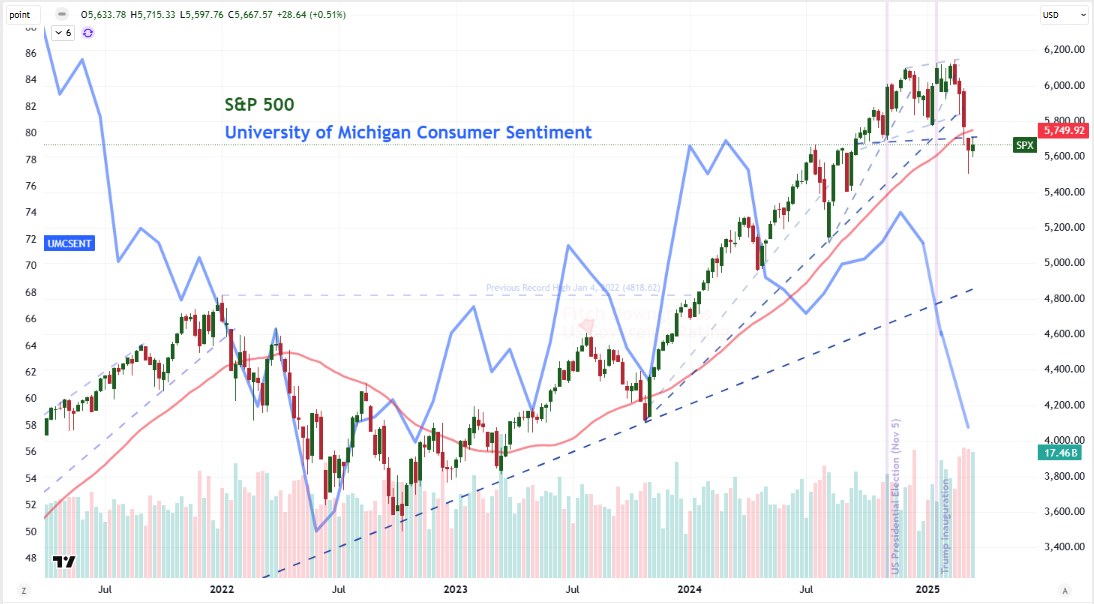

While there is plenty of global pertinent fundamental event risk on tap, the US seems to be distinctly in the crosshairs. Following on Monday’s US PMIs, Tuesday consumer sentiment survey from the Conference Board should carry great consequence. After the University of Michigan (UofM) sentiment survey offered up a dramatic extension of its confidence collapse by hitting a multi-year low from its benchmark reading, the Dollar and US risk assets were set on borrowed time. As the largest aggregate consumer in the world, the us consumer is a bellwether for both US growth and the health of the global economy.

There have been prominent divergences between the UofM and Conference Board measures, and more of that contrast can keep skepticism from sinking the S&P 500. However, if it falls in line with the earlier release, this week’s reading could trigger more serious concerns, Beyond the headline number, the components should be monitored closely for structural guidelines that weight the dollar.

S&P 500 Overlaid with the University of Michigan Consumer Confidence Survey (Weekly)

Source: John Kicklighter, TradingView

Monitoring the headlines for trade war developments and weighing the balance of growth won’t be the only fundamental guidelines through the week ahead. Monetary policy will be another distinct point of contention. Aside from like the Mexican Central Bank’s rate decision (which should be interesting against the backdrop of trade wars and sharp US fiscal cuts), it is worth watch the upstream criteria for FOMC policy determination. Last week, the Fed offered a steady course on its relatively high benchmark rate range with a caution of the uncertainty that is ahead. So long as the jobless rate continues to hold near such historically low levels and inflation pressures don’t grow out of hand, the group will be able to keep to a wait-and-see approach that intends to track the Trump administration’s actions and impact.

That said, price pressures have been bubbling up once again – as employment concerns grow with waves of federal government layoffs. With NFPs the following week, the attention in the immediate term should be the Fed’s favorite inflation reading, the PCE deflator. Should there be a big shift, the market will very likely pay significant mind to the move. Then again, the weight of the event risk could also work to curb activity in the lead up to the release, just like the FOMC’s presence did this past week.

Chart of DXY Dollar Index Overlaid with US CPI and UofM Consumer Inflation Expectations (Weekly)

Source: John Kicklighter, TradingView, BLS, University of Michigan

-- Written by John Kicklighter, Global Head of Content