FX Weekly Overview (Brazil Issue)

Dollar to Reflect Inflation Data in Brazil and the US, Copom Minutes, Geopolitical Uncertainties in the Middle East, and the Brazilian Electoral Scenario

Leonel Mattos

- Currencies

By: John Kicklighter, Head of Market Research

Benchmark risk assets are still climbing to record highs, but the progress remains stunted and conviction is increasingly coming under scrutiny. Has the calculus changed after last weeks’ NFPs miss and/or in advance of this week’s CPI update?

Talking Points:

Risk appetite was on a solid course through this past week with fresh record highs from the likes of the Dow and S&P 500 until Friday’s August nonfarm payrolls data crossed the wires. When the jobs report crossed the wires well short of expectations (22K versus 75K expected), it triggered a conflict in speculative expectations and priorities. On the hand, the trend to flat job growth – and likely eventual net losses – and the uptick in the jobless rate would be a strong catalyst for the Fed to pursue the rate cuts that President Trump has demanded. On the other, the economy was in a seemingly more vulnerable course that stimulus was likely ill-prepared to offset to the point of justifying a sustained drive to record highs. The modest swell in volatility offered a timely reminder that we are at threshold of the typical seasonal activity shift, the ‘summer doldrums’ to more active fall trade.

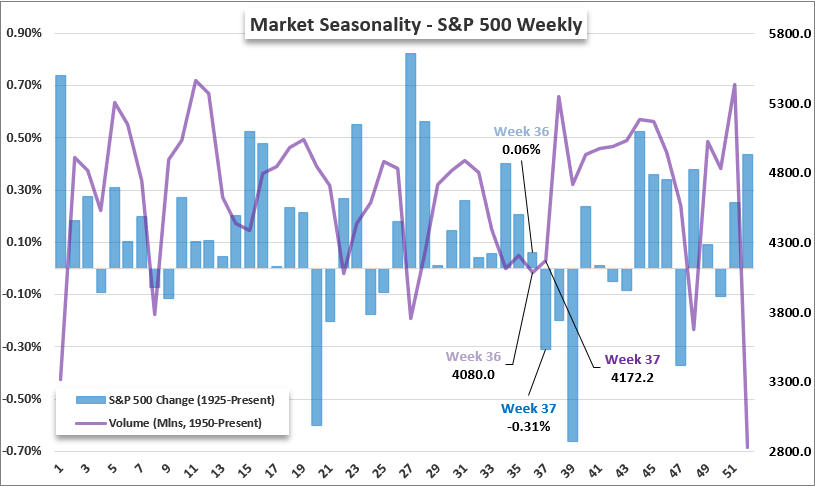

S&P 500 and Volume Calendar Week Averages over 100 and 75 Years

Source: John Kicklighter, Standard & Poor’s

We don’t always have to follow that norm, but the groundwork seems to be in place to charge the markets back into that mold. As we head into this 37th week of the year, it is worth reflecting on typical trends of volume and volatility. The former is more consistent and the latter open to the circumstances underlying our current course. Should fundamental awareness pick up and rouse volatility potential, it is likely that the markets start to treat this period as the ‘week before the FOMC decision’. But that isn’t the only theme that is circling outside the fading light of the speculative fires. Trade pressures, financial deficits and general economic health are all matters that could be spurred to life with a targeted headline.

Calendar of Top Global Macro Event Risk

Source: John Kicklighter

Sign Up

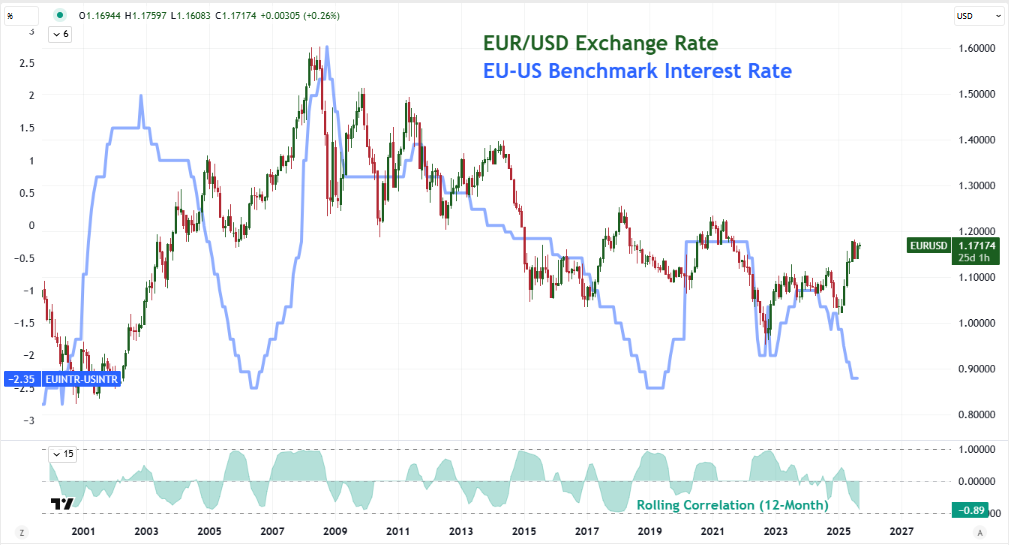

While a case can be made for stirring the deep fundamental waters of a handful of systemic fundamental themes, it isn’t a stretch to suggest that attention will be the most pronounced around monetary policy leading into the Federal Reserve rate decision on September 17th. That focus will draw out some interesting attention for different scheduled events on the docket over the coming week. While the New York Federal Reserve’s consumer inflation expectation figure on Monday, NFIB US business confidence survey and NFPs annual revision on Tuesday are all closely associated to US monetary policy; the contrast in perspective from the European Central Bank (ECB) on Thursday should not be overlooked.

Considering the US is currently sporting a 210 basis point (bp) premium to its European counterpart, there is a wide gap in rates between the developed world’s two largest central banks. Was the ECB just ahead of the curve or is this a fundamental gap that will be retained? This question will be answered more by the Fed next week, but a holding pattern for the ECB and insight on their forecasts will certainly factor into the equation of ‘the US versus the world’.

Chart of EURUSD Overlaid with the ECB-Fed Benchmark Rate Spread (Monthly)

Source: TradingView, Federal Reserve Economic Database

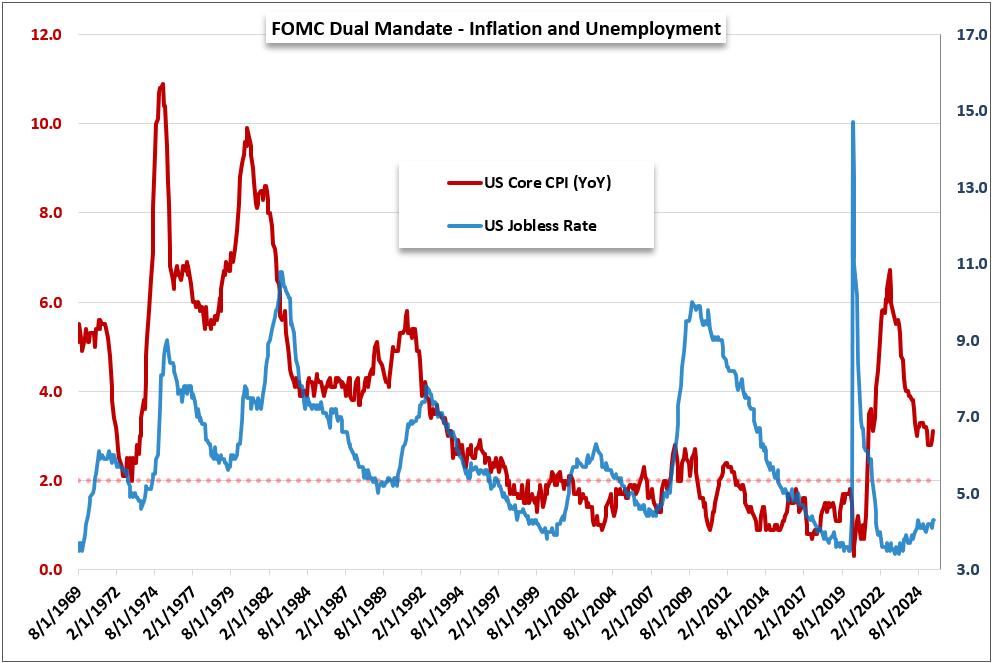

If you are looking for the US perspective on monetary policy, however, the update to the country’s August consumer inflation report (CPI) Thursday shortly after the ECB decision will carry far more weight with dictating Fed action – which is likely to register more distinctly in general risk trends. The consensus forecast from economists for headline CPI acceleration from a 2.7 to 2.8 percent clip and for the core tempo to hold at 3.1 percent would see both measures firmly above the 2.0 percent stated target for inflation that the FOMC maintains as its dual mandate to anchor policy in data rather than feeling. With the disappointing showing in the jobs report this past week, the focus on the counterbalance to the central bank’s focus (inflation vs labor) will be intensified moving forward.

If price pressures soften, it will likely make a case for a rate cut, and further easing after this month, a much easier proposition. Then again, if inflation were to pick up while the jobless rate is also creeping higher, the discussion around policy course will become much more intense. If price pressures do indeed climb, the surety of meaningful rate cuts through the end of 2025 and beginning of 2026 will start to falter to some measure. This may ultimately prove a complicated and nuanced update, so it will be important not to assume the traditional, basic analysis that weaker inflation leads to less rate potential and thereby a weaker currency. This chain is not always the reality.

Chart of US Consumer Price Index YoY Change and US Jobless Rate (Monthly)

Source: John Kicklighter, US Bureau of Labor Statistics

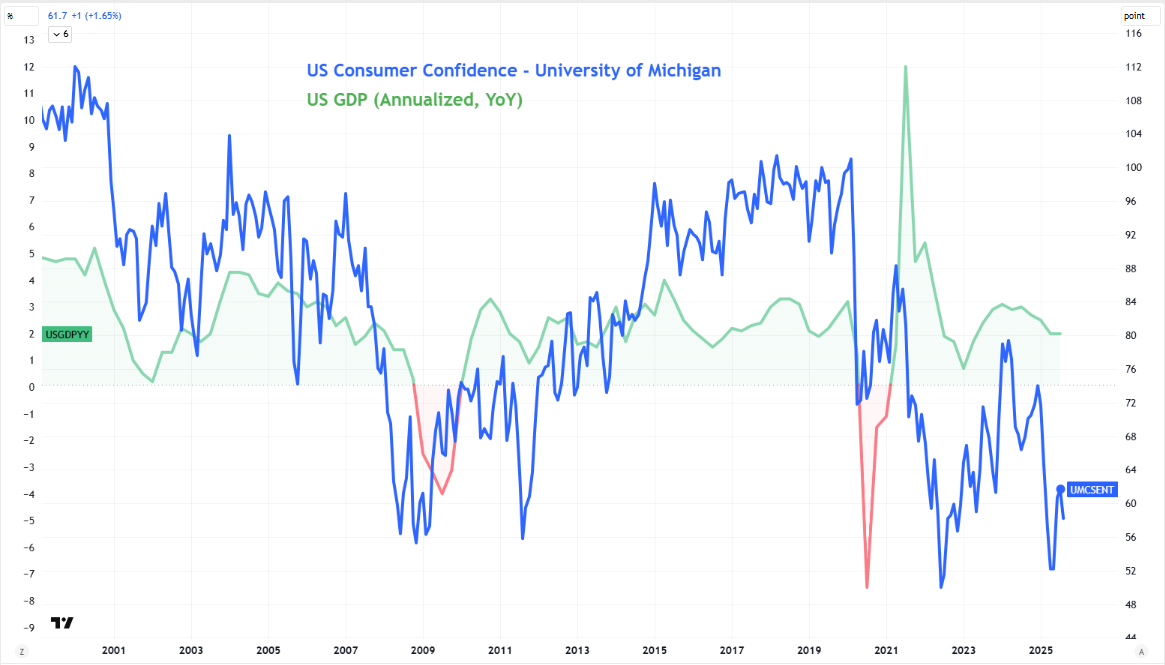

The third of the top events to monitor over the coming week is another Friday release: the University of Michigan’s consumer sentiment survey for September. The consumer sector is the largest aggregate contributor to growth in the world’s largest economy. The help of this wealthy cadre matters when it comes to general underlying themes like monetary policy and economic potential. US sentiment has meandered near multi-decade lows in past months, so a renaissance of enthusiasm would be a welcome conviction for an uncertain market. While President Trump attacks data collection methods and partisan interpretations of data, readings like the UofM surveys still carry serious weight in core themes.

If this reading is to post a strong bounce, it can help offset underlying concerns about a stalling economy, and it could also throttle the Fed’ sense of urgency to lower rates owing to a shifted inflation forecast. Alternatively, if sentiment drops sharply, the data will feed simultaneously support expectations of Fed support while also painting a sour picture of underlying economic health. As the President aims to control the veracity of data and laments the urgency to cut rates sharply while feeding the capital market’s elevated, a sentiment survey like this one could catch the speculative masses off guard.

Chart of US Consumer Confidence from University of Michigan Over US Annualized GDP (Monthly)

Source: TradingView, US Bureau of Economic Analysis, University of Michigan

What are the major events and indicators on tap for the global economy that could charge volatility in markets and reshape deeper fundamental themes? Sign up for the updated Global Macro Calendar updated each week with a two week look ahead of the top events!

Sign Up

--- Written by John Kicklighter, Global Head of Content

The subsidiaries of StoneX Group Inc. provide financial products and services, including, but not limited to, physical commodities, securities, clearing, global payments, risk management, asset management, foreign exchange, and exchange-traded and over-the-counter derivatives. These financial products and services are offered in accordance with the applicable laws in the jurisdictions in which they are provided and are subject to specific terms, conditions, and restrictions contained in the terms of business applicable to each such offering. Not all products and services are available in all countries. The products and services offered by the StoneX Group of companies involve risk of loss and may not be suitable for all investors. Full Disclaimer. This content is not intended for residents of any particular country, and the information herein is not advice nor a recommendation to trade nor does it constitute an offer or solicitation to buy or sell any financial product or service, by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Please refer to the Regulatory Disclosure section for entity-specific disclosures. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc. The information herein is provided for informational purposes only. This information is provided on an ‘as-is’ basis and may contain statements and opinions of the StoneX Group of companies as well as excerpts and/or information from public sources and third parties and no warranty, whether express or implied, is given as to its completeness or accuracy. Each company within the StoneX Group of companies (on its own behalf and on behalf of its directors, employees and agents) disclaims any and all liability as well as any third-party claim that may arise from the accuracy and/or completeness of the information detailed herein, as well as the use of or reliance on this information by the recipient, any member of its group or any third party.

© 2026 StoneX Group Inc. all rights reserved.

Our subscribers have access to comprehensive market analysis from StoneX spanning commodities, equities, currencies and more.

Dollar to Reflect Inflation Data in Brazil and the US, Copom Minutes, Geopolitical Uncertainties in the Middle East, and the Brazilian Electoral Scenario

Interest rate expectations are becoming a more powerful driver of currency markets than the policy decisions themselves. As investors rapidly reprice the path of U.S. interest rates, the U.S. dollar is gaining momentum while currencies linked to more cautious central banks face growing pressure.

WTI crude's return to the low $70s has introduced a fresh variable into the USD/CAD macro story, connecting oil prices directly to the Federal Reserve rate hike expectations driving dollar strength. With Kevin Warsh delivering his first press conference as Fed Chair, a softer signal on inflation could stall the pair's six-week advance at a critical resistance level.

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bi-lateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve; our financials and record of accomplishment are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform, to “boots on the ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.