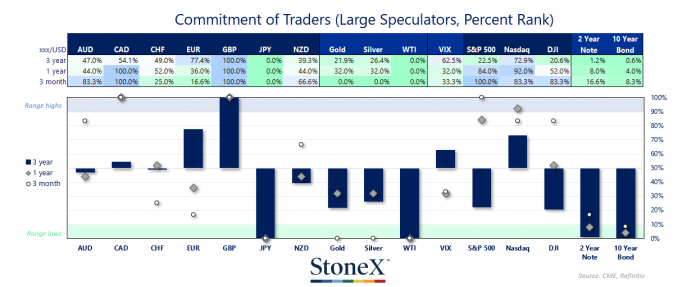

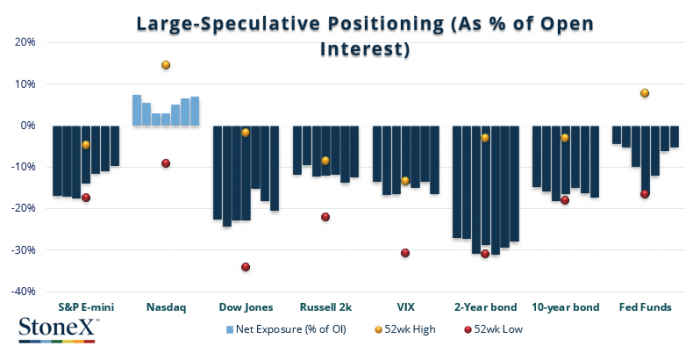

A glance at the percent rank (PR) table show us that traders remain relatively bearish on JPY, WTI and 2/10-yer bond futures markets over the 3-month, 1-year and 3-year timeframes. A further reduction of gross shorts on the S&P 500 has helped push the 1-year PR positioning towards the top of its range (traders remain net-short but the exposure if less bearish). And for a second week running, GBP is at the op of its range across all three time horizons as net-long exposure has risen to a near 9-year high. A reduction of gross shorts on AUD futures has also seen the 1 and 3-year PR move to the centre of its range and push the 3-month closer to its highs. Whilst we saw strong buying on CAD futures, subsequent CPI data likely saw any of those bets reversed as traders now favour the BOC to pause at their next meeting.

• Net-long exposure to GBP/USD rose to its most bullish level in nearly nine years

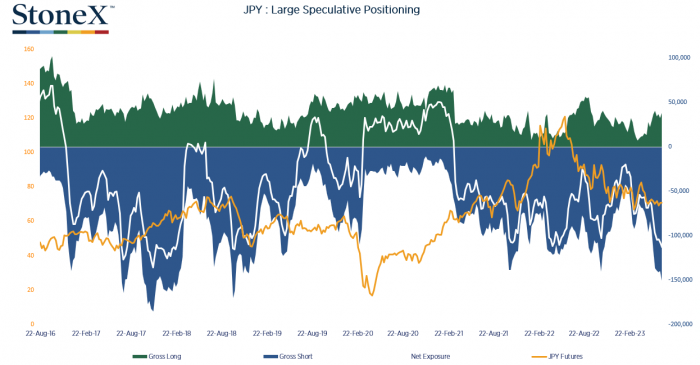

• Traders were their most bearish on JPY futures since October 2018

• Gross shorts for AUD futures were trimmed for a fourth consecutive week

• Net-long exposure to USD index futures (DXY) rose to a 4-month high

• Traders increased gross-long exposure to CAD futures by 78.5% (22.1k contracts) and reduce gross shorts by -13.9% (-8.6k contracts)

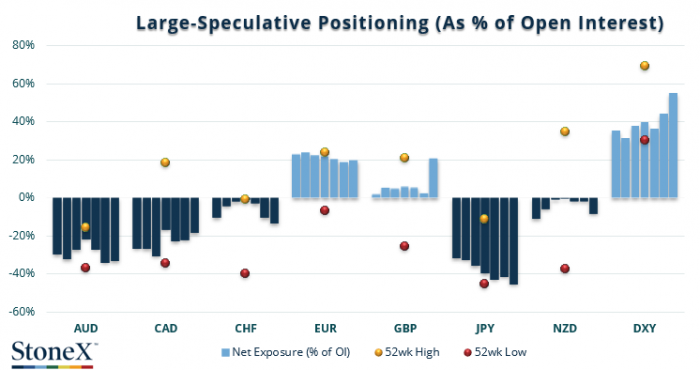

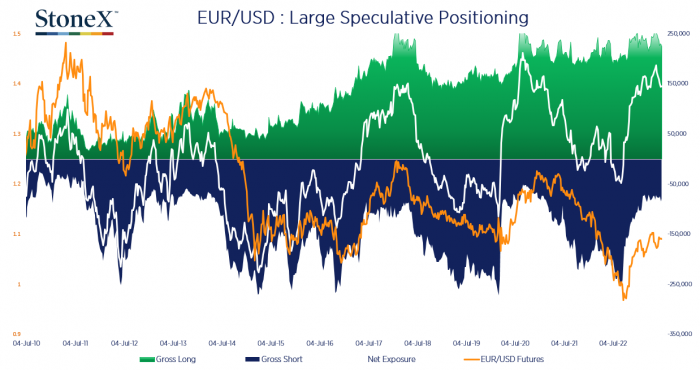

Net-long exposure to EUR futures fell for a fifth week after hitting a sentiment extreme. However, this has been caused by a closure of longs. We saw gross shorts rose at their fastest pace in 23-weeks the prior week, yet around half of these were trimmed last week and gross-short exposure has effectively been flat overall since February. And that suggests that traders are not quite ready to bet against the euro or a hawkish ECB, even if they felt the need to lighten up their long holding in recent weeks.

EUR/USD appears to be forming a base above 1.0800, and last week’s Doji alongside a weak inflation report for the US suggests there could be some upside for EUR/USD over the near-term.

Large speculators were their most bearish on JPY futures since October 2018, which adds further concerns that USD/JPY’s rally could be at or near a sentiment extreme. In recent history we have seen the BOJ or MOF intervene in the currency market between 145 and 150, so it came as no surprise to see USD/JPY pull back almost immediately once it probed 145 on Friday during Asian trade. So whilst the hawkish Fed and dovish BOJ is supportive of a higher USD/JPY, we urge caution at these highs as mere rumours of an intervention can spark bouts of volatility which could send USD/JPY materially lower.

• Large speculators were their least bearish on the 30-day Fed fund futures in…. which implies reduced bets for further Fed hikes

• Bearish bets on the 2-year bond bill were also trimmed further from their record high

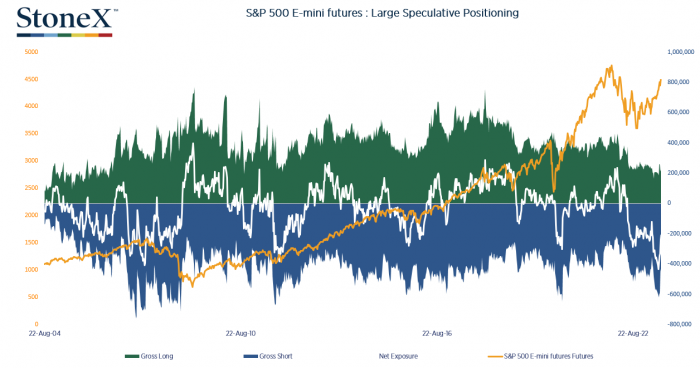

• Traders continued to trim their net-short exposure to S&P 500 futures

• Net-long exposure to Nasdaq 100 futures rose to a 6-week high

• Increased net-short exposure to the VIX

We warned of a sentiment extreme in May for S&P 500 bears, before net-short exposure rose to a record high five weeks ago. Since then, bears have trimmed their gross positioning for four weeks, and gross longs have risen slightly (but not with too much confidence). The break above the August high likely forced more bears to liquidate and further support a rally. And the fact that the S&P 500 printed a bullish engulfing candle and found support at the August high (and closed to a 14-molnth high last week) likely means that more shorts have capitulated. And that suggest there could be further upside potential, with bulls now eyeing a break of 4500.

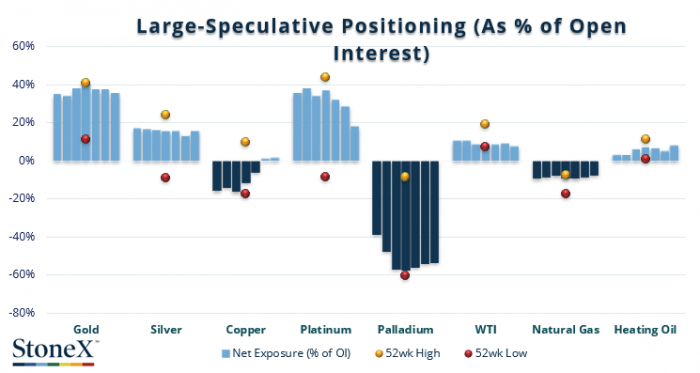

• Large speculators were net-long copper futures for a second week

• Large speculators were their least bullish on WTI futures in nearly 13 years

• Traders were their most bearish on palladium futures by a record amount

• Gross short exposure to platinum futures rose for a third week and net-long exposure was its lowest in 13-week