The swoon in liquidity through the Thanksgiving holiday period helped to stall a larger turn in speculative markets. Can its restoration revive the bulls or are conditions systemically shifted?

Talking Points:

Expectations for participation and volatility are constrained by December and Week 50 norms which align to the so-called ‘Santa Claus’ rally

Top event risk for the coming week is undoubtedly the FOMC rate decision where a -25bp cut is heavily expected, but the outlook for 2026 remains open to speculation

A range of developed and developing central banks will see interest in their own policy updates amplified by the Fed and China will offer a run of important data

A Santa Claus Rally That Will Be Difficult to Override

There will be a hearty run of event risk over the coming week – topped by the closely watched FOMC (Federal Open Market Committee) rate decision and updated forecasts into 2026. However, what is likely to exert a greater influence on the market’s level of volatility and ability to establish any meaningful momentum is the backdrop liquidity conditions. While the US central bank’s decision on whether or not to cut rates and insight into its plans moving forward taps into a broader fundamental interest for both US and global markets, a suppressed foundation of participation colored by strong seasonal expectations can dramatically alter how that - and other - event risk ultimately impacts the markets.

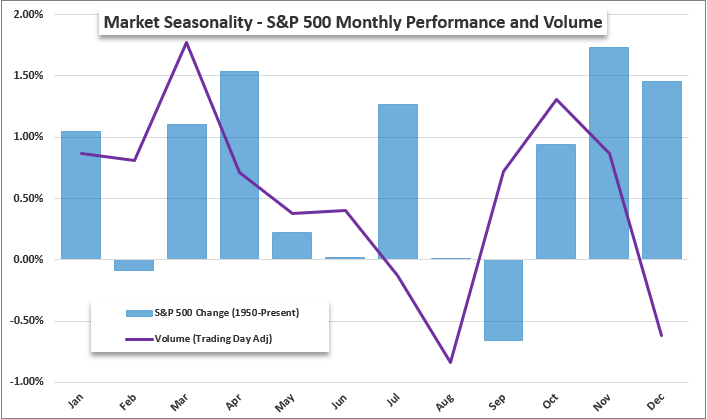

The month of December is has averaged the second lowest volume of the calendar year for the S&P 500 stretching back over the past 75 years, while the bias in market performance has been bullish. The range of possibilities for direction is broader and far more dependent on what the prevailing themes are in any given year. Volume, on the other hand, is far more consistent in its drop in turnover – and that in turn contributes to a more steadfast norm of lower volatility, as measured by the VIX index.

Historical Average S&P 500 Change and Volume by Calendar Month Source: John Kicklighter, Standard & Poor’s

On a lower time frame, the 50th week of the year does offer a skew towards a modest decline averaged out over the decades. Whether we actually see a gain or loss from year to year is still dependent on what themes are pervading investors’ collective concerns and what event risk is available to hit the nerve. Typically, this period of the year aligns to a last run of major event risk and a concentration of monetary policy updates from the large central banks. There is a run of major developed and emerging market central banks set to update on their policy strategy, but most of the biggest players are seen near the end of their dovish regimes. The Fed is the outlier, and it will certainly stand as test for the market’s capacity to discount any meaningful changes in outlook.

That said, the market has been actively adjusting its expectations for the world’s largest central bank with financial media and politicians weighing in with their own takes. There is a saturation in awareness and expectation that is likely reflected in positioning and hedges. If we take this particular event out of the equation, what would our expectations for trend and volatility look like? Most likely it would be an easing into the year-end complacency that has turned into the seasonal norm of the ‘Santa Claus Rally.’ While that does typically come with a presumed bullish bias, it is also hallmarked by a material downshift in progress commensurate to the reduction in participation. This is arguably the strongest market force over the coming weeks, so expectations of meaningful volatility or productive trend should account for this factor first and foremost.

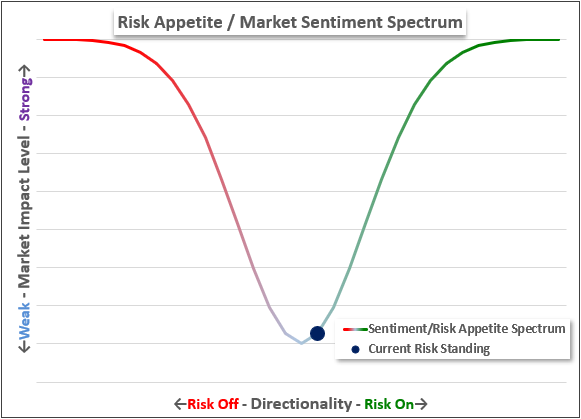

Risk Appetite or Market Sentiment Spectrum of Bullish to Bearish, Strong to Weak

Source: John Kicklighter

High Profile Events with a Questionable Impact Potential

Just because market conditions are not conducive to fostering systemic momentum or mounting large scale reversals – which denotes a consideration of follow through as confirmation – does not mean that we don’t face potential for volatility in certain areas of the market. When broader conditions are more restrained, there are two considerations I like to consider when seeking out relatively high levels of activity: assets that are directly in the crosshairs of scheduled (and capable) event risk and assets are located at the extreme of the risk spectrum.

For scheduled event risk, the docket ahead has plenty; but the scale of fundamental importance of the listings does not necessarily translate one-for-one into productive market movement. For one, the more liquid a market, the more profoundly the seasonal liquidity lull will stunt reaction. Where the line is between pursuing smaller markets where traditional event risk analysis expectations are distorted in pursuit of volatility depends on the individual’s risk profile. I prefer sticking to the deeper markets and either identifying exceptional event risk armed with the capacity to generate temporary bouts of unseasonal movement or switch to a longer time frame or strategy aimed at congestion which is more aligned to broader conditions.

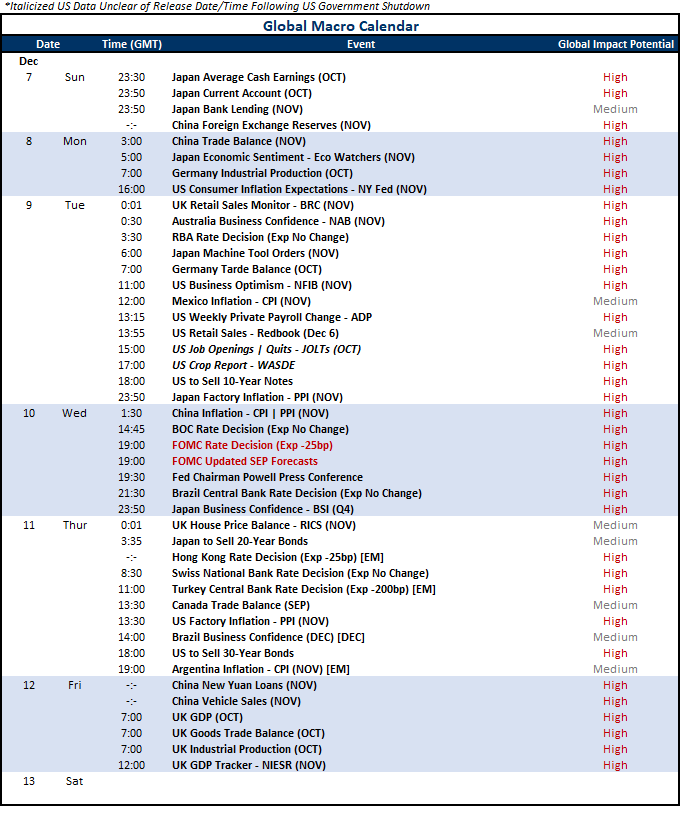

Calendar of Top Global Macro Event Risk Source: John Kicklighter

China’s Trade Balance Reminds of a Key Fundamental Undercurrent

In the range of themes that have waxed and waned over the past months, 2025's top volatility charge followed the Trump administration's introduction of unilateral and intense tariffs against many of the United States' largest trade partners. The most aggressively targeted country was China which engaged in an escalating reciprocal trade war before the two countries called a cease fire. The latest of these pauses is set to last an entire year, but the economic coordination between the two largest economies looks far from encouraging. For the more immediate purposes of China's economic health, trade remains a critical - perhaps the critical - engine behind the world's second largest economy.

China's official GDP figures remain firmly in the green, but a moderate pace of positive growth for the Asian giant is not the same thing as a commensurate pace for a major economy in the West. With the housing market and high leverage of the past decade still being worked down and Chinese consumer not ready to carry the economy, an extended decline in trade will increasingly weigh...but large jumps in surplus run the risk of reviving trade disputes.

Chart of USDCNH Overlaid with Difference of US-China Trade Balances (Weekly)

Source: TradingView; Forex.com; US BEA; China NBS

It’s Not Just About a Heavily Discounted Fed Cut

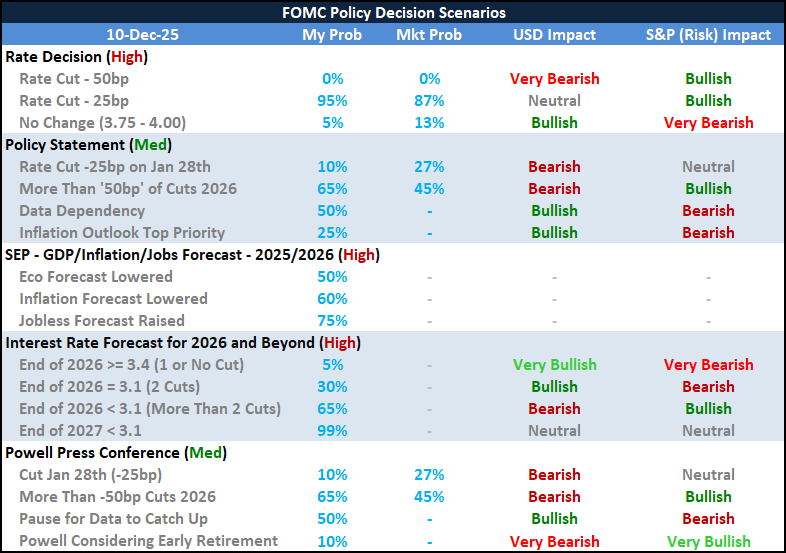

For top event risk this week, the FOMC rate decision would be important even if taken out of the context of the year-end time frame and the expectations the broader market would heap on its speculative charge. The confidence of the central bank’s course moving forward is highly debated with a clear split in beliefs among its members and with Fed Chairman Powell’s retirement in sight amid heavy criticism coming from the White House. What the path for the central bank looks like into 2026 represents the greater range of possibilities for the market and thereby the larger capacity for market influence in the form of volatility and trend development – whether kicked off in these final weeks or forming the foundation for movement in the early part of the new year.

As such, come 19:00 GMT on Wednesday, the focus should be less on the heavily discounted -25bp rate cut (to a range of 3.50 – 3.75 percent) and more on the simultaneous release of the quarterly Summary of Economic Projections (SEP). The group’s forecasts for growth, employment and inflation are important; but the principal focus will be on the outlook for the interest rate at the end of 2026. In the September SEP, the 2026 median forecast for the US rate was lowered to 3.4 percent (3.375 percent or the midpoint of 3.25 – 3.50 percent). It is unlikely that that prediction holds as it would mean only one rate cut in 2026 if the group were to cut this week. If they did hold that forecast, it would be highly market moving itself – a significant boost to the Dollar and weight on risk-dependent benchmarks like the S&P 500 – so the benchmark question is: how sharply will the rate forecast be lowered?

FOMC Decision and Market Impact Scenario Table

Source: John Kicklighter

There are a Host of ‘Other’ Central Bank Decisions on Tap

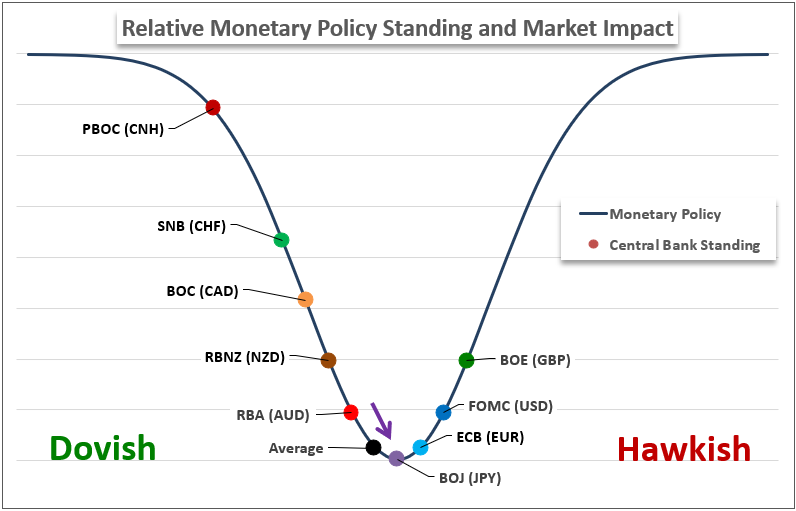

Finally, a consideration for fundamental potency should be afforded to the range of ‘other’ central bank rate decisions that we have on tap over the week. With the backdrop of the Fed’s decision rousing interest in the monetary policy in general and the variability of the cycle that the different authorities find themselves (most in the middle or end of their dovish epochs), the divergences matter particularly in the movement of capital across boarders seeking higher rates of return on comparable risk assets. On tap we have:

Reserve Bank of Australia (RBA): Tuesday morning, the developed central bank is not expected to change its benchmark rate, which would put its 3.60 percent key rate essentially on par with the Federal Reserve’s which can prompt a flip in the carry appeal which the currency had seen flag in recent years.

Bank of Canada (BOC): Wednesday approximate 7 hours before the Fed announces its own decision, the BOC is expected to hold at 2.25 percent for a second meeting. The group has lowered from its peak last year by -275 bps and is seen at the end of its phase.

Brazil Central Bank (BCB): In contrast to the cuts that the Fed, RBA and BOC have pursued, the BCB has been tightening over the past year. The group is seen holding at 15 percent Wednesday at this meeting which keeps it at a near two-decade high – but that differential has not added much carry appetite to the Real.

Hong Kong Monetary Authority (HKMA): The HKMA more or less follows its US counterpart which insinuates a -25bp cut Thursday to 4.00 percent should the Fed move. This is an interesting dynamic as Hong Kong is a ‘Special Administrative Region’ of China, yet its benchmark rate and exchange rate are very different from China’s.

Swiss National Bank (SNB): The SNB is seen holding its benchmark rate Thursday at 0.00 percent – a level that already creates abnormal conditions between Switzerland, Europe and the rest of the world. Capital flow is important to the country and the zero bound rate has exacted its consequences.

urkey Central Bank (CBRT): Finally on Thursday, expectations for the Turkish authority have ranged broadly; but the prevailing economist forecast now sits at a -100 bp cut to 38.5 percent. Despite the extreme level of this benchmark relative to other countries of its size, there has been little-to-no curb of the USDTRY’s climb.

Relative Monetary Policy Standing Spectrum – Current Level and Anticipated Change

The subsidiaries of StoneX Group Inc. provide financial products and services, including, but not limited to, physical commodities, securities, clearing, global payments, risk management, asset management, foreign exchange, and exchange-traded and over-the-counter derivatives. These financial products and services are offered in accordance with the applicable laws in the jurisdictions in which they are provided and are subject to specific terms, conditions, and restrictions contained in the terms of business applicable to each such offering. Not all products and services are available in all countries. The products and services offered by the StoneX

Group of companies involve risk of loss and may not be suitable for all investors. Full Disclaimer.

This content is not intended for residents of any particular country, and the information herein is not advice nor a recommendation to trade nor does it constitute an offer or solicitation to buy or sell any financial product or service, by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Please refer to the Regulatory Disclosure section for entity-specific disclosures.

No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc. The information herein is provided for informational purposes only. This information is provided on an ‘as-is’ basis and may contain statements and opinions of the StoneX Group of companies as well as excerpts and/or information from public sources and third parties and no warranty, whether express or implied, is given as to its completeness or accuracy. Each company within the StoneX Group of companies (on its own behalf and on behalf of its directors, employees and agents) disclaims any and all liability as well as any third-party claim that may arise from the accuracy and/or completeness of the information detailed herein, as well as the use of or reliance on this information by the recipient, any member of its group or any third party.

Currencies

The subsidiaries of StoneX Group Inc. provide financial products and services, including, but not limited to, physical commodities, securities, clearing, global payments, risk management, asset management, foreign exchange, and exchange-traded and over-the-counter derivatives. These financial products and services are offered in accordance with the applicable laws in the jurisdictions in which they are provided and are subject to specific terms, conditions, and restrictions contained in the terms of business applicable to each such offering. Not all products and services are available in all countries. The products and services offered by the StoneX Group of companies involve risk of loss and may not be suitable for all investors. Full Disclaimer. This content is not intended for residents of any particular country, and the information herein is not advice nor a recommendation to trade nor does it constitute an offer or solicitation to buy or sell any financial product or service, by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Please refer to the Regulatory Disclosure section for entity-specific disclosures. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc. The information herein is provided for informational purposes only. This information is provided on an ‘as-is’ basis and may contain statements and opinions of the StoneX Group of companies as well as excerpts and/or information from public sources and third parties and no warranty, whether express or implied, is given as to its completeness or accuracy. Each company within the StoneX Group of companies (on its own behalf and on behalf of its directors, employees and agents) disclaims any and all liability as well as any third-party claim that may arise from the accuracy and/or completeness of the information detailed herein, as well as the use of or reliance on this information by the recipient, any member of its group or any third party.

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bi-lateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve; our financials and record of accomplishment are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform, to “boots on the ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.