USDBRL should reflect the interest rate decision by the FOMC and the Copom, data from Brazil and the US, and the possibility of retaliation by the White House

- Bullish

- Conviction of former president Jair Bolsonaro by the Supreme Federal Court may worsen commercial and diplomatic relations between Brazil and the United States and result in new retaliations by the White House, which would increase the perception of risks for national assets and harm the performance of the real.

- Bearish

- The Federal Reserve is expected to cut the U.S. interest rate by 0.25 p.p. this week and signal further cuts in the coming months, which reduces the outlook for U.S. bond yields and tends to depreciate the dollar globally.

- Monetary Policy Committee (Copom) is expected to keep the basic interest rate (Selic) unchanged and signal its stability for a prolonged period, which supports the outlook for Brazil's interest rate differential and the strengthening of the real.

The week in review

- American inflation remained moderate and showed no signs of significant impacts from import tariffs.

- US employment data revised downward, reinforcing fears of an economic slowdown.

- The European Central Bank keeps its interest rates stable and projects optimism for the bloc's economy and inflation, reducing bets on new interest rate cuts.

- Brazil's IPCA showed deflation in August, but continued to record significant increases in its core index and in service prices.

- Former President Jair Bolsonaro is convicted by the Supreme Court, raising concerns of a worsening in trade and diplomatic relations between Brazil and the United States.

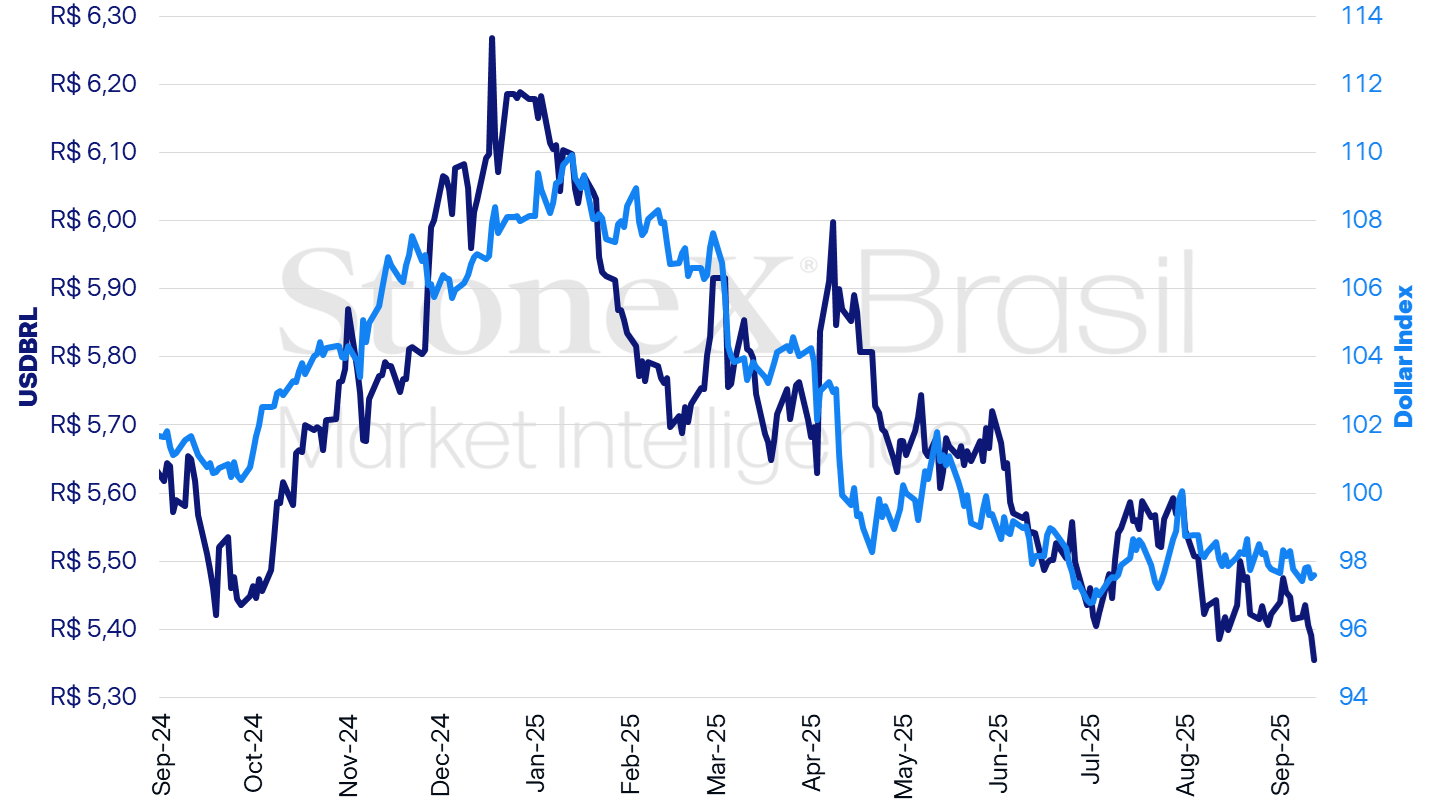

USDBRL and Dollar Index (points)

Source: StoneX cmdtyView. Design: StoneX.

USDBRL variations | Daily: -0.67% | Weekly: -1.10% | Monthly: -1.24% | YTD: -13.32% | In 12 months: -4.67% |

Dollar index variations | Daily: +0.07% | Weekly: -0.19% | Monthly: -0.18% | YTD: -9.75% | In 12 months: -3.73% |

KEY EVENT: FOMC interest rate decision

Expected impact on USDBRL: bearish

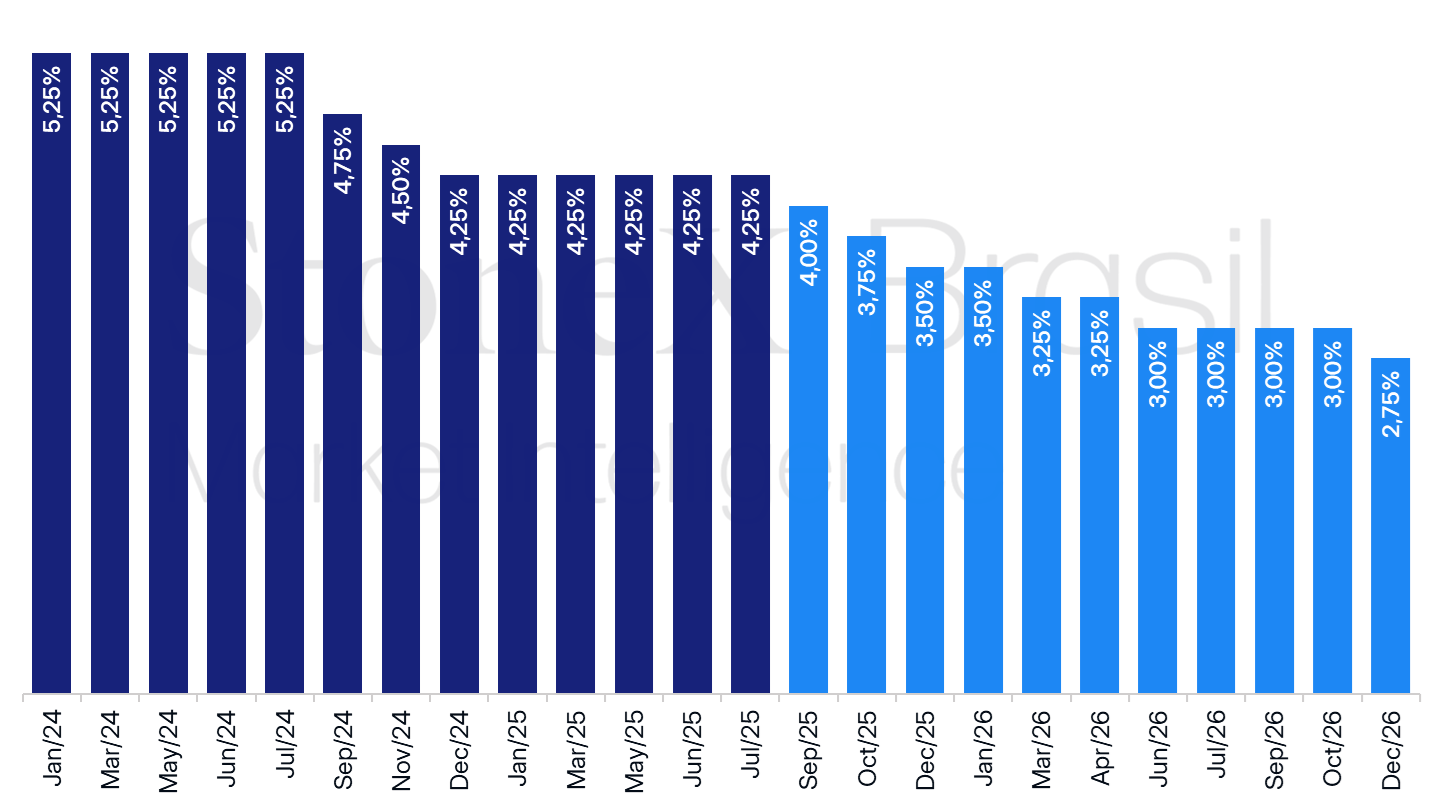

USA: History and expectation for the interest rate – updated on September 12, 2025

Source: CME FedWatch Tool. Design: StoneX. Refers to the bet with the highest probability in the future interest rate market on the indicated date.

There is virtually consensus that the Federal Open Market Committee (FOMC) of the Federal Reserve (Fed) will lower its interest rate in its decision on Wednesday (17), from the range between 4.25% and 4.50% p.a. to the range between 4.00% and 4.25% p.a.

Why this is important: The expectation of a series of interest rate cuts by the Federal Reserve in the coming months lowers the outlook for returns on American bonds and hurts the attraction of foreign investment, which tends to devalue the dollar globally.

Balance of risks: The release of recent economic data showed a more intense slowdown in the American labor market, while no broader effects of import tariffs on inflation were observed.

- Therefore, the FOMC should justify its interest rate cut based on the shift in the balance of risks, that is, lower risks of a resurgence in inflation and higher risks of a weakening labor market.

Focus on projections: As there should be no surprise with the Committee's decision, the focus of investors falls on the press conference of Fed Chairman Jerome Powell and, mainly, on the release of the Summarized Economic Projections.

- These projections provide estimates from all FOMC members for economic growth, unemployment, inflation, and interest rates in the US between 2025 and 2027.

- Right now, investors are betting that the Federal Reserve will make three consecutive interest rate cuts this year and another three throughout 2026.

- However, it is possible that the members of the FOMC see, in their median projection, a slower path of interest rate cuts, given the concern with the inflation scenario mentioned in previous decisions.

- In the projection released in June, the document indicated the expectation of two cuts in the interest rate in 2025 and only one in 2026.

- If, indeed, the projections suggest more gradual interest rate cuts, investors may reduce their bets on rate cuts and favor a global recovery of the dollar.

Differences: Although there is practically a consensus that the FOMC will cut its interest rates by 0.25 p.p. this Wednesday, it is likely that the decision will not be unanimous.

- On the one hand, it is possible that some members, such as Christopher Waller and Michelle Bowman, members of the Fed's Board of Governors, will vote for a larger cut, of 0.50 p.p.

- It is also possible that Jeffrey Schmid will vote to maintain the interest rate.

Indicators of the week: Additionally, investors should follow the release of indicators to calibrate their expectations for the evolution of the American economy in the coming months.

- Retail sales: Amid this context of a slowdown in the American labor market, retail sales are expected to temper their pace of expansion in August, with a monthly increase of 0.3% for both the headline index and the metric that excludes automobile sales, suggesting a gradual slowdown in consumer demand.

- Manufacturing: American manufacturing is expected to have remained stable in August, hindered by a scenario of rising input costs and a slowdown in consumer demand.

Copom interest rate decision

Expected impact on USDBRL: bearish

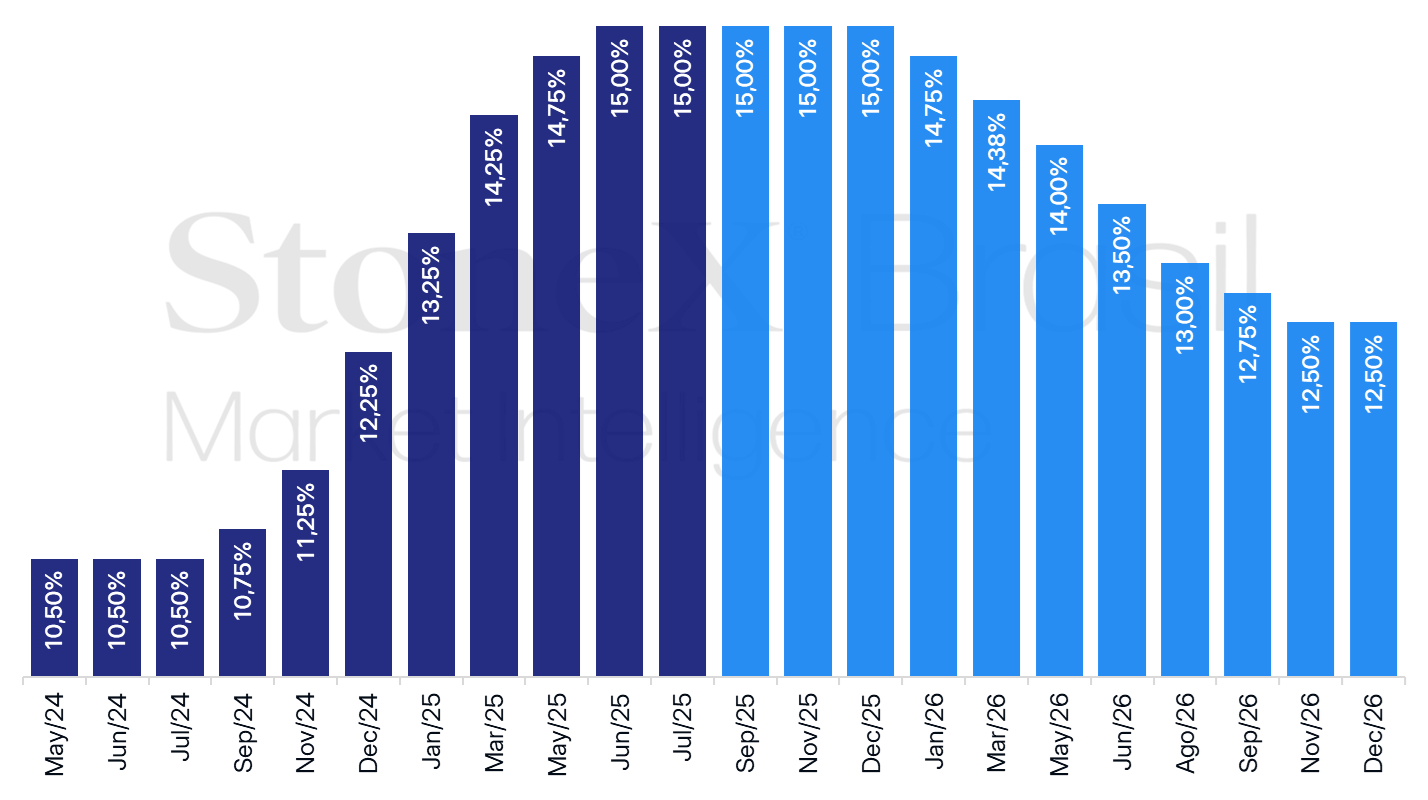

Brazil: History and expectation for the interest rate – Focus bulletin for September 5, 2025

Source: Central Bank of Brazil. Design: StoneX.

There is consensus among investors that the Central Bank's Monetary Policy Committee (Copom) will keep the basic interest rate (Selic) unchanged at next Wednesday's (17) meeting, maintaining it at 15.00% per year.

Why this is important: The maintenance of the Selic at a high level, accompanied by a likely new signal of stability for a "prolonged period," tends to raise the return projections for Brazilian treasuries.

- This movement should favor the attractiveness of domestic assets, especially when it coincides with the likely beginning of the interest rate cut cycle in the United States, widening the interest rate differential and contributing to the appreciation of the real.

Overview: At the July 30 meeting, the Copom statement highlighted the indication that the rate would remain at the current level for a "very prolonged period."

- This stance was justified by inflation still being above the Central Bank’s target and by the perception that the labor market remained moderately heated.

- In the last few weeks, however, the release of more moderate inflation figures has increased bets that the start of the rate-cutting cycle could be brought forward.

- In a recent interview, the president of the Central Bank, Gabriel Galípolo, however, pointed out that, although inflation projections are being revised downward, they remain above the target for the next two years and convergence is happening slowly.

- According to him, this would justify the maintenance of the restrictive monetary policy and reinforces that the "Central Bank cannot be moved by punctual data."

Monitoring the economy: Additionally, the evolution of the effects of monetary tightening on productive activity and employment should also influence the future conduct of monetary policy.

- In this sense, investors will be watching for the release of labor market data on Tuesday (16) and the Central Bank’s Economic Activity Index (IBC-Br) for July on Monday (15), considered a preview of GDP.

White House retaliation

Expected impact on USDBRL: bullish

Investors should also monitor the possibility of further retaliation by the White House against Brazil after the conviction of former President Jair Bolsonaro by the Supreme Court last week.

Why this is important: Investors fear that Bolsonaro’s conviction could worsen commercial and diplomatic relations between Brazil and the United States, which would increase the perceived risks of domestic assets and weaken the real.

Overview: The White House explicitly linked the imposition of tariff and sanctions on Brazil to dissatisfaction with court proceedings in the country, particularly those against former President Jair Bolsonaro and social media platforms.

- Shortly after the conviction, U.S. Secretary of State Marco Rubio said the U.S. "will respond appropriately to this witch hunt," while Donald Trump said the conviction was "surprising" and "terrible for Brazil."

- Even if the United States does not impose any new sanctions or tariff on Brazil, which is uncertain at this time, the conviction should hinder a diplomatic and commercial rapprochement between the two countries.

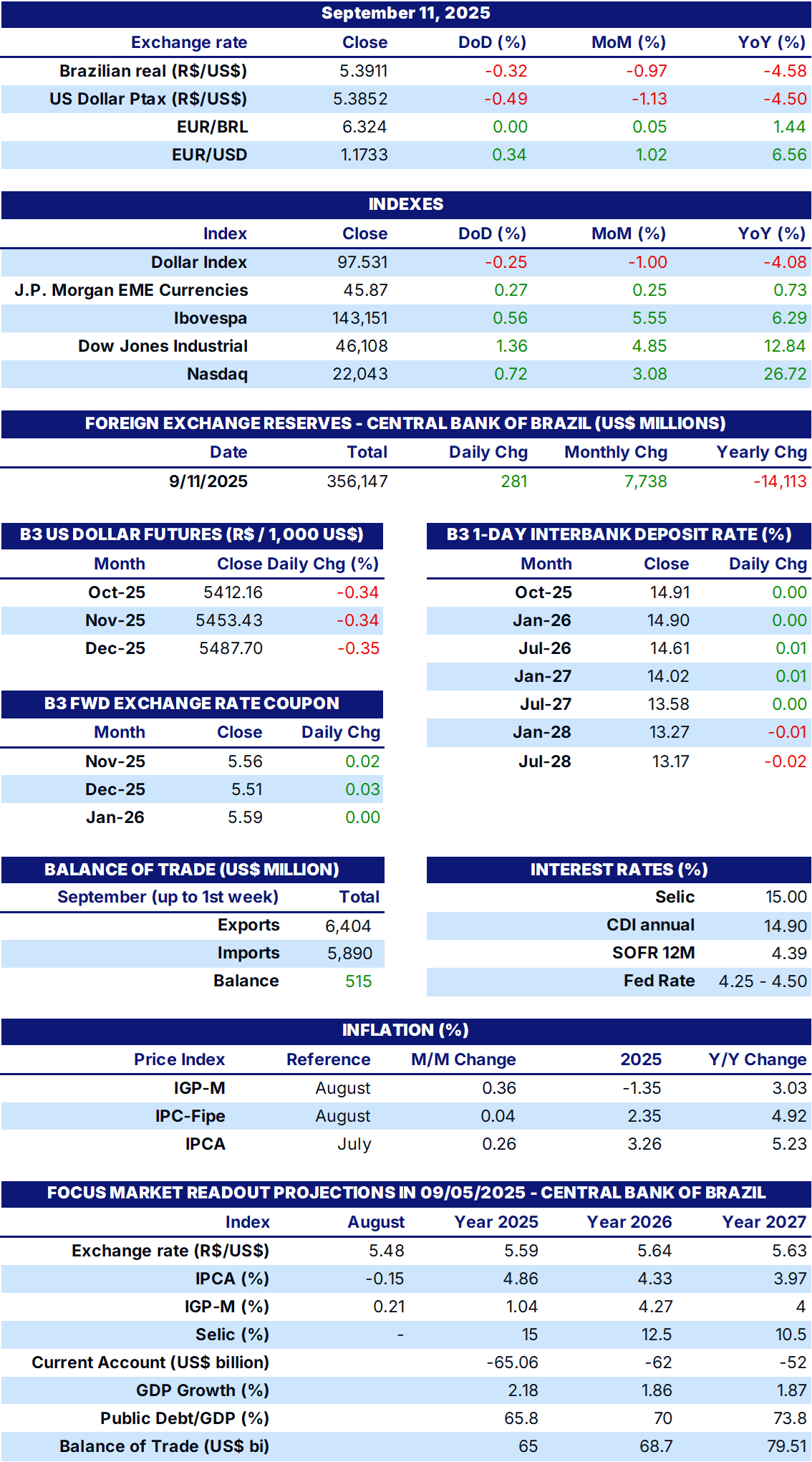

INDICATORS

Sources: Central Bank of Brazil; B3; IBGE; Fipe; FGV; MDIC; IPEA and StoneX cmdtyView.