USDBRL to reflect Trump tariffs ruling, Middle East tensions, Brazilian data, and Lagarde’s potential exit from the ECB

- Bullish

- Should the IPCA‑15 and labor market data point to slowing inflation and weakening economic activity, expectations for a larger Selic rate cut in March may grow, reducing the interest rate differential and pressuring the Brazilian real.

- Rumors surrounding a potential early departure of ECB President Christine Lagarde are likely to heighten uncertainty over European monetary policy, which could weaken the euro against the dollar in the coming days and indirectly impact the real.

- Bearish

- The U.S. Supreme Court’s decision to invalidate reciprocal tariffs imposed under Trump’s administration increases uncertainty over U.S. economic policy and could lead to significant fiscal costs, which may negatively impact the dollar.

- While escalating tensions between the U.S. and Iran have heightened global risk aversion, the recent rise in oil prices has supported Brazilian assets tied to the sector and may continue to bolster the real.

The week in review

- The week’s most anticipated data, U.S. GDP and Personal Consumption Expenditures (PCE) Price Index, presented mixed signals.

- The first reading of Q4 GDP indicated weaker-than-expected growth, pointing to a faster economic slowdown in the U.S. On the other hand, December’s PCE showed a higher-than-expected price increase compared to the previous month.

- On the political front, the highlight came on Friday (20) with the U.S. Supreme Court ruling that tariffs imposed by President Donald Trump without Congressional approval were illegal. This decision weakened the dollar globally throughout the session, though some practical issues remain unresolved.

- The unexpected escalation of tensions between the U.S. and Iran heightened geopolitical risk perceptions during the week, driving oil futures higher. Despite this, the real benefited from the rise in domestic oil sector stocks.

- On the domestic agenda, the focus was on the Central Bank of Brazil’s Economic Activity Index (IBC-Br), which pointed to a slight weakening in economic activity and reinforced expectations of a faster cycle of Selic rate cuts.

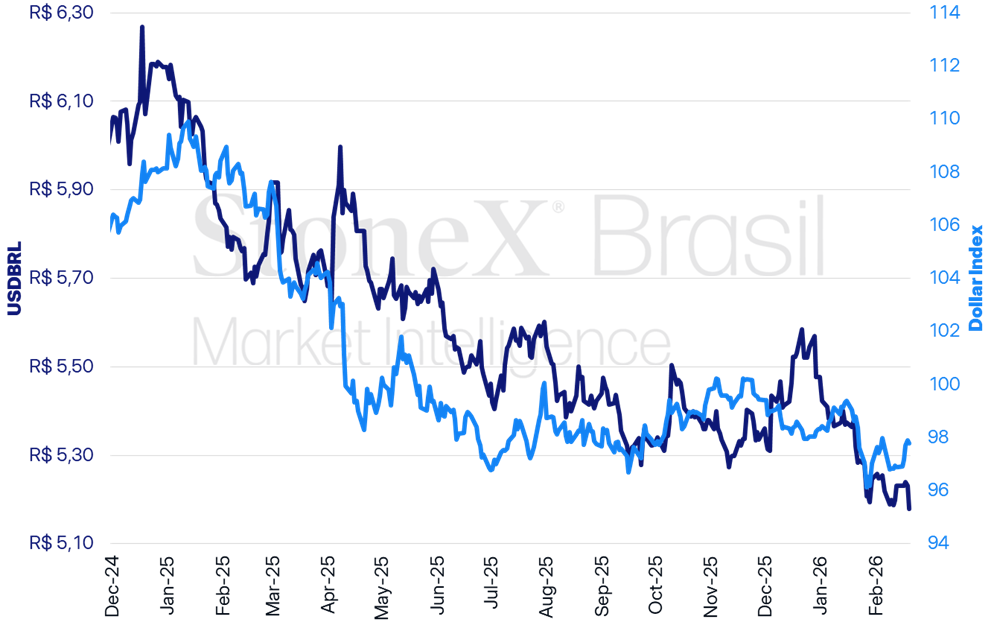

USDBRL and Dollar Index (points)

Source: StoneX cmdtyView. Prepared by: StoneX.

USDBRL Variations

Daily: -1.00% | Weekly: -1.00% | Monthly: -1.31% | Yearly: -16.18% | 12 Months: -9.23%

Dollar Index Variations

Daily: -0.13% | Weekly: +0.90% | Monthly: +0.76% | Yearly: -9.58% | 12 Months: -8.08%

KEY EVENT: U.S. Supreme Court declares Trump tariffs illegal

Expected Impact on USDBRL: Bearish

On Friday (20), the United States Supreme Court issued its decision on the case involving the so-called “reciprocal tariffs” imposed by President Donald Trump’s administration.

- By a vote of 6 to 3, the Court concluded that the use of IEEPA to implement these tariffs exceeded the authority granted to the president, aligning with three lower courts that had already deemed the measure improper.

- As a result, the reciprocal tariffs are to be immediately suspended.

- The controversy began last April when President Donald Trump unilaterally decided to impose reciprocal tariffs without Congressional approval, as is typically required for such measures.

- In a press conference following the Supreme Court’s decision, Donald Trump announced plans to maintain an active tariff policy by introducing general tariffs of 10% starting Monday (23).

- These new tariffs would be imposed under Section 122 of the Trade Act of 1974, which allows them to last for a maximum of 150 days, requiring Congressional approval for any extension.

- Trump also advocated for investigations by the U.S. Trade Representative to enable tariff implementation under other provisions of the Trade Act of 1974, such as Sections 301 and 201.

Why It Matters: By reigniting uncertainties around fiscal and economic policy under the current U.S. administration, the ruling is expected to exert downward pressure on the dollar internationally, potentially benefiting the real.

- Trade policy has been a cornerstone of the government’s economic strategy, and the ruling undermines its political position and planning, raising questions about potential compensatory measures.

- Notably, by declaring reciprocal tariffs illegal, the Supreme Court opens the door for affected parties to seek reimbursement for payments made to U.S. customs. This process could result in a fiscal outlay exceeding $130 billion, which, if realized, would exacerbate the country’s growing fiscal challenges.

IPCA-15 and Employment Data in Brazil

Expected Impact on USDBRL: Bullish

In Brazil, the week’s agenda includes key indicators for investors to recalibrate their expectations regarding the Central Bank’s monetary policy direction.

- The highlight will be the release of the National Consumer Price Index 15 (IPCA-15), scheduled for Friday (27).

- On the same day as the IPCA-15 release, investors will also monitor December’s formal employment data through CAGED’s Monthly Employment Evolution.

Why It Matters: If the data reinforces the perception of slowing inflation and a weakening labor market, expectations for a broader interest rate cut by the Central Bank’s Monetary Policy Committee (Copom) in March may increase, which could weaken the real.

Outlook: The most recent inflation data, January’s Broad Consumer Price Index (IPCA), showed a 0.33% rise in prices, steady compared to the previous month.

- Over the past 12 months, however, the index accelerated to 4.44%, still within tolerance margins.

- In the labor market, December’s CAGED data showed a net balance of 618,160 layoffs. However, December is seasonally a month with more layoffs than hires.

- In 2025 overall, 1.28 million new formal jobs were created. Despite the positive figure, the total is the lowest since the pandemic in 2020.

Signs of Weakening: Over recent weeks, other indicators of Brazilian economic activity have pointed to a slowdown.

- December’s IBC-Br – a GDP proxy – indicated a 0.18% decline in Brazil’s economy.

- The latest readings of the Monthly Services Survey (PMS) – Brazil’s largest economic sector – and the Monthly Trade Survey (PMC) showed declines of 0.4%.

Looking Ahead to Rate Cuts: Since its last rate decision, the Copom has signaled that if the trend of inflationary slowdown and economic cooling persists, it may begin a rate-cutting cycle at its next meeting, albeit cautiously.

- While a rate cut has been signaled for the next meeting, its magnitude remains uncertain.

- Currently, most investors are betting on a 0.50 percentage point cut. Clearer signs of price stability could solidify expectations for a broader cut.

Tensions Between the U.S. and Iran

Expected Impact on USDBRL: Bearish

Despite an optimistic start to the week regarding a potential U.S.-Iran nuclear deal, the second half of the week saw escalating military tensions between the two countries, intensifying global risk aversion and driving oil futures prices higher.

- Among developments reported during the period was the U.S. military’s increased troop presence and the deployment of an aircraft carrier to the Middle East, raising fears of a possible attack in the region.

- Additionally, on Thursday (19), during a Peace Council meeting, President Donald Trump indicated he would decide “within the next 10 days” whether to order intervention in the country.

- Over the last two days, fears of conflict in the region and its impact on global oil supply contributed to rising Brent crude prices, though the commodity saw slight declines on Friday’s session.

Why It Matters: On one hand, increased geopolitical tensions tend to heighten risk aversion among investors, potentially hurting riskier assets and currencies of emerging markets, such as the Brazilian real.

- Conversely, last week’s rise in oil prices supported shares of national oil-related companies, boosting the real over several sessions.

Potential Departure of Lagarde from ECB

Expected Impact on USDBRL: Bullish

Last Wednesday (18), reports emerged suggesting ECB President Christine Lagarde might be considering leaving her role before her term ends in April 2027.

- According to the Financial Times, the decision would allow Emmanuel Macron to influence the choice of her successor ahead of France’s next elections.

- However, the day after the news broke, Lagarde denied plans for an early exit, stating that consolidation requires completing her term.

- Next week, Lagarde is set to deliver two speeches, one on Monday (23) and another on Thursday (26). Investors will closely monitor her remarks for clearer signals regarding the ECB’s leadership future.

Why It Matters: Lagarde is widely regarded as having successfully controlled inflation in the eurozone over the past few years. Therefore, any potential change in ECB leadership could heighten uncertainty regarding the EU’s monetary policy direction.

- Uncertainty surrounding the ECB tends to weaken the euro against the dollar, which could indirectly impact the real’s value against the U.S. currency.

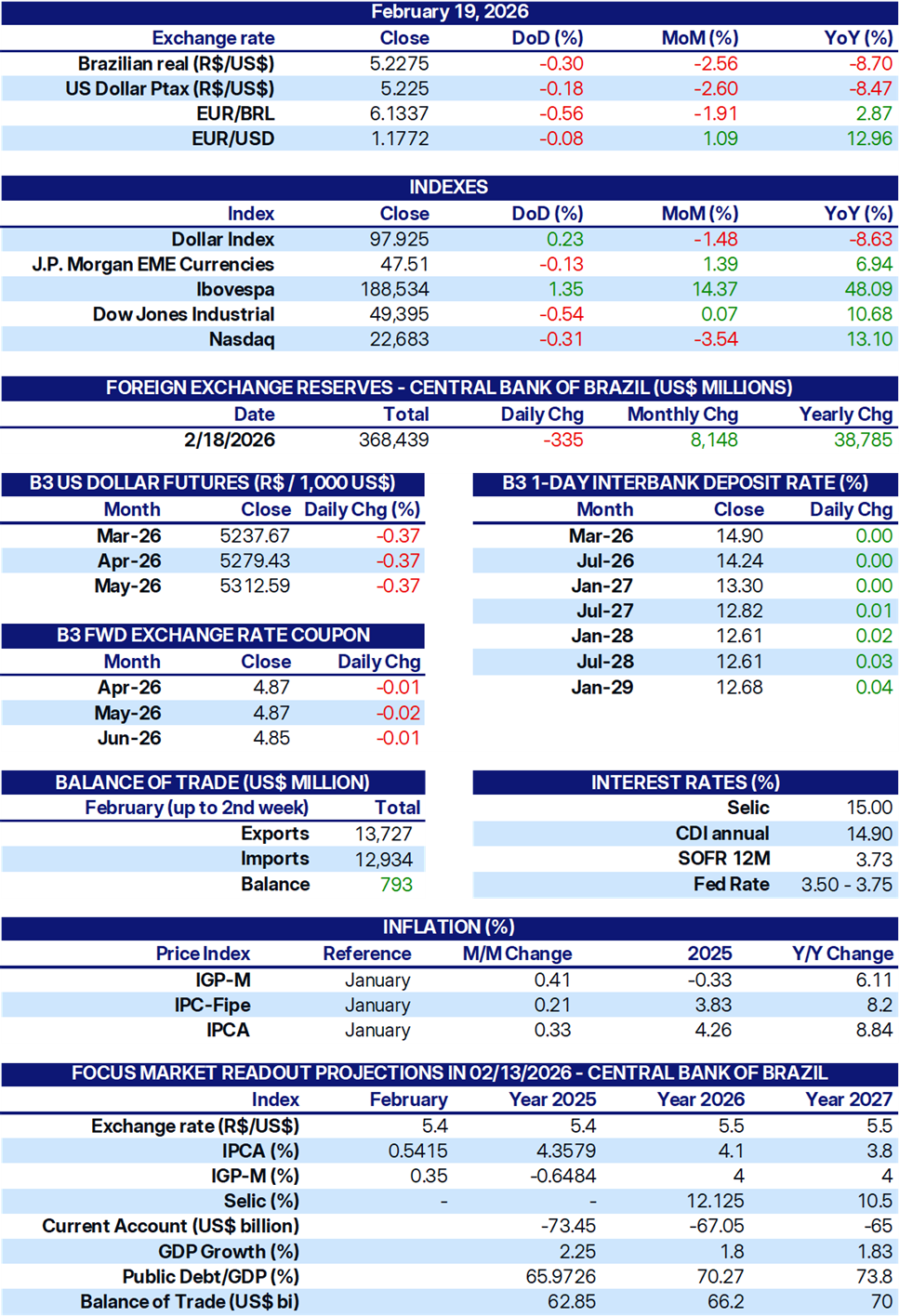

INDICATORS

Sources: Central Bank of Brazil; B3; IBGE; Fipe; FGV; MDIC; IPEA; and StoneX cmdtyView.