USDBRL Expected to Reflect Copom Minutes and U.S. Economic Data

- Bullish

- U.S. economic data is likely to signal a stronger economy, reducing bets on interest rate cuts by the Federal Reserve and supporting the dollar's global strength.

- Bearish

- The Copom minutes are expected to reinforce the Brazilian Central Bank’s cautious stance amid challenging inflation dynamics, reducing bets on interest rate cuts in Brazil and supporting the real.

Th week in review

- The week’s focus was on interest rate decisions in the U.S., Brazil, and other major global economies.

- In the U.S., the Federal Open Market Committee (FOMC) chose to keep the policy rate steady in the range of 3.50% to 3.75% annually.

- In addition to the decision, markets reacted to signals that Jerome Powell may remain on the Board of Governors after his term ends, until he feels confident that government attacks on the Federal Reserve’s independence and his leadership have ceased.

- In Brazil, the Monetary Policy Committee cut the policy rate (Selic) by 0.25 percentage points, lowering it from 14.75% to 14.50% annually. The accompanying statement hinted at potential adjustments to the pace of Selic changes.

- On the geopolitical front, the ongoing impasse between the U.S. and Iran continued to fuel uncertainty in financial markets. The lack of progress kept oil premiums and geopolitical risk perceptions high.

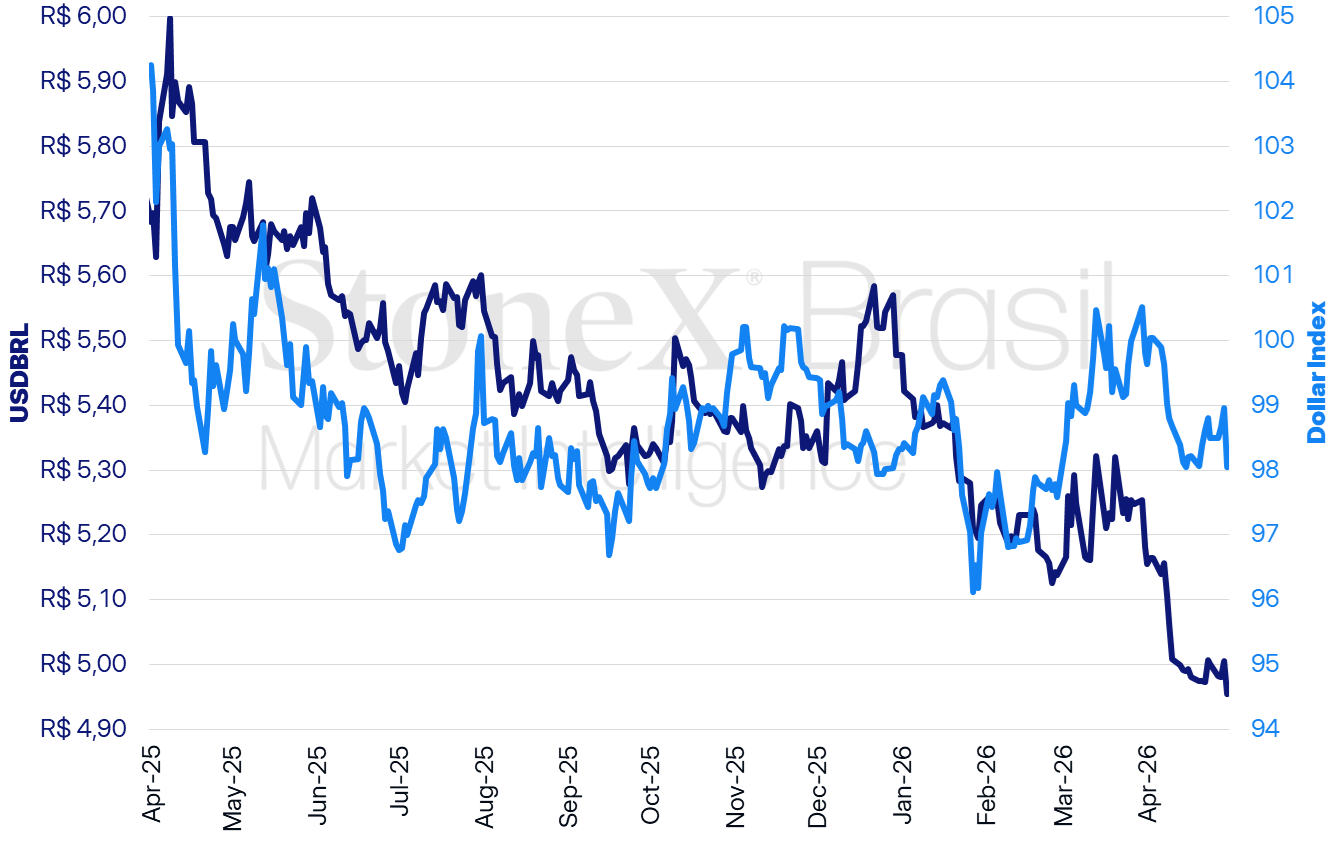

USDBRL and Dollar Index (points)

Source: StoneX cmdtyView. Prepared by: StoneX.

USDBRL Variations | Daily: -1.00% | Weekly: -0.94% | Monthly: -4.38% | Annual: -9.54% | Over 12 Months: -12.71%

Dollar Index Variations | Daily: -0.92% | Weekly: -0.45% | Monthly: -1.77% | Annual: -0.27% | Over 12 Months: -1.49%

KEY EVENT: U.S. Economic Data

Expected Impact on USDBRL: Bullish

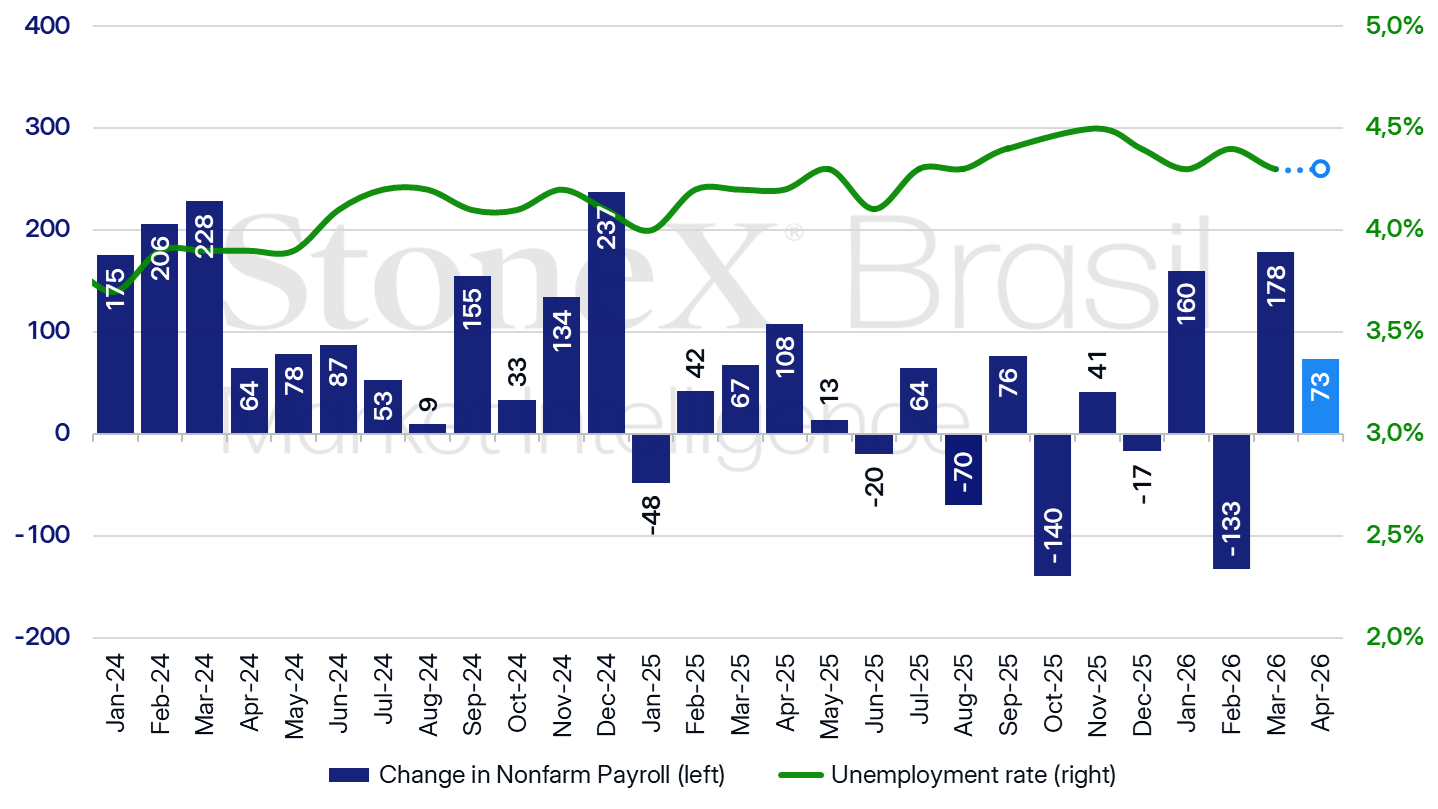

Changes in Nonfarm Payroll (thousands) and Unemployment Rate (%) in the United States

Source: U.S. Bureau of Labor Statistics (BLS), Federal Reserve Bank of St. Louis. Design: StoneX.

This week’s packed agenda includes the release of key U.S. economic indicators, particularly the Employment Situation Report and April’s Services Purchasing Managers’ Index (PMI).

Why It Matters: These indicators are likely to continue signaling a robust U.S. economy, which, combined with inflationary pressures stemming from global oil supply constraints, may reduce the odds of Fed interest rate cuts.

- This would, in turn, boost U.S. Treasury yields and contribute to global dollar strength.

What to Expect: The median forecast for the Employment Situation Report predicts net job creation of 73,000 in April, exceeding the six-month average of 15,000.

- Additionally, the unemployment rate is projected to remain steady at 4.3%, reinforcing a healthy labor market outlook.

- The median forecast for ISM’s Services PMI in April stands at 54.0 points, matching March’s result and signaling moderate expansion in the largest segment of the U.S. economy.

- Strong labor market performance and productive activity suggest financial conditions in the U.S. are not restrictive, negating the need for short-term Fed rate cuts.

- These interpretations align with last week’s preliminary Q1 GDP data, which indicated stronger-than-expected annualized household consumption growth of 1.6%, driven by demand for services like healthcare and financial services.

Copom Minutes

Expected Impact on USDBRL: Bearish

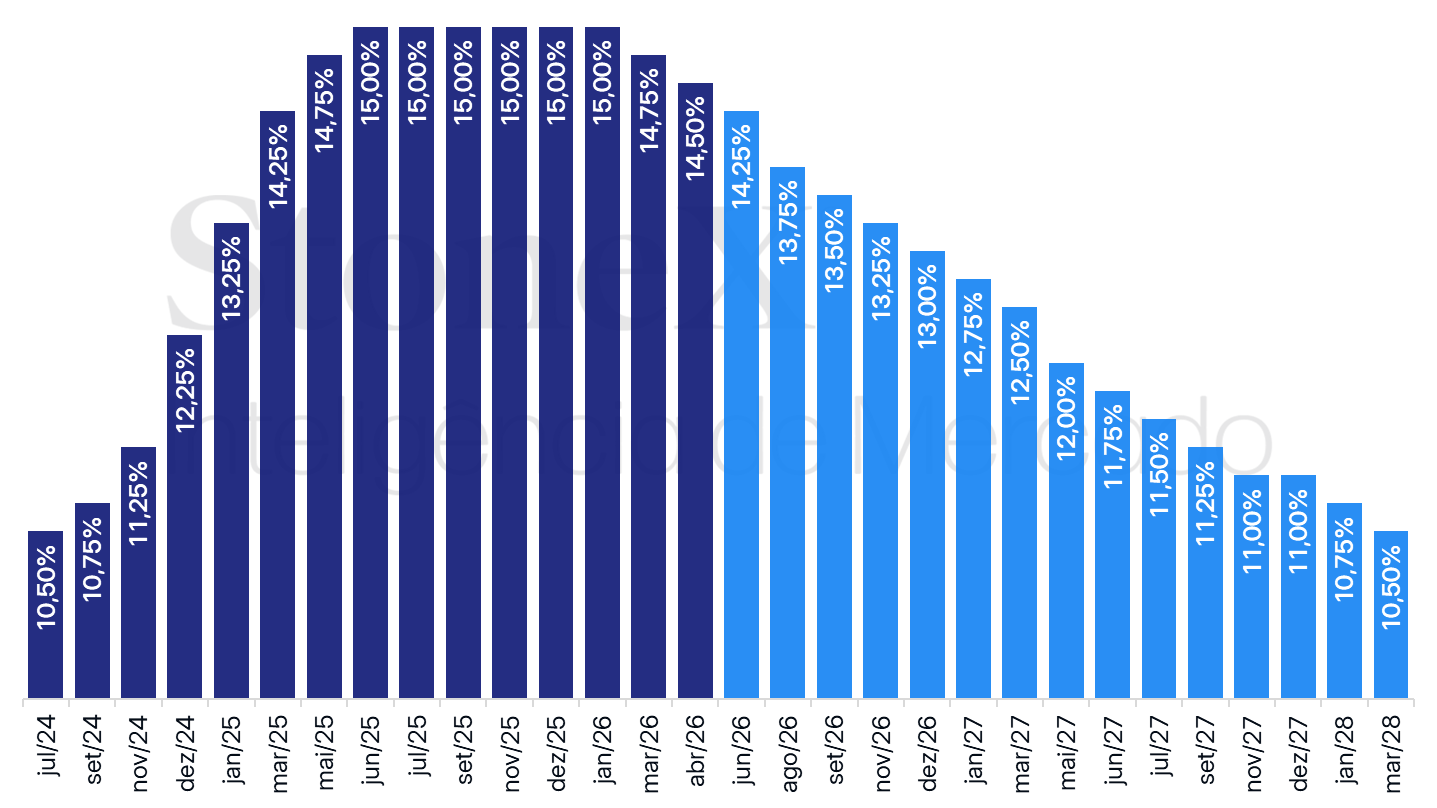

U.S.: Historical and Projected Interest Rate Trends – Updated April 24, 2026

Source: Brazilian Central Bank. Design: StoneX.

Investors are closely monitoring the release of minutes from the Brazilian Central Bank’s latest Copom meeting, where the Selic rate was reduced from 14.75% to 14.50% annually.

- In its statement, the monetary authority raised inflation projections and indicated potential adjustments to the pace of Selic movements, pending further information on the conflict’s impact on domestic prices.

- The minutes may offer deeper insights into policymakers’ current economic assessments and outlooks, helping investors refine their expectations.

Why It Matters: Signals of greater caution and a potential slowdown in Selic rate cuts could lead to higher interest rate expectations, strengthening the real.

Shifting Expectations: Since the onset of the Middle East conflict in late February, inflation expectations for the 2026 year-end IPCA have risen from 3.91% to 4.61%, exceeding the target ceiling.

- As a result of anticipated inflationary pressures from oil price shocks, year-end Selic rate projections have climbed from 12.00% to 13.00% annually.

- This suggests financial institutions are recalibrating their forecasts, particularly given the lack of resolution in the geopolitical impasse.

- Consequently, near-term bets on further Selic cuts have diminished.

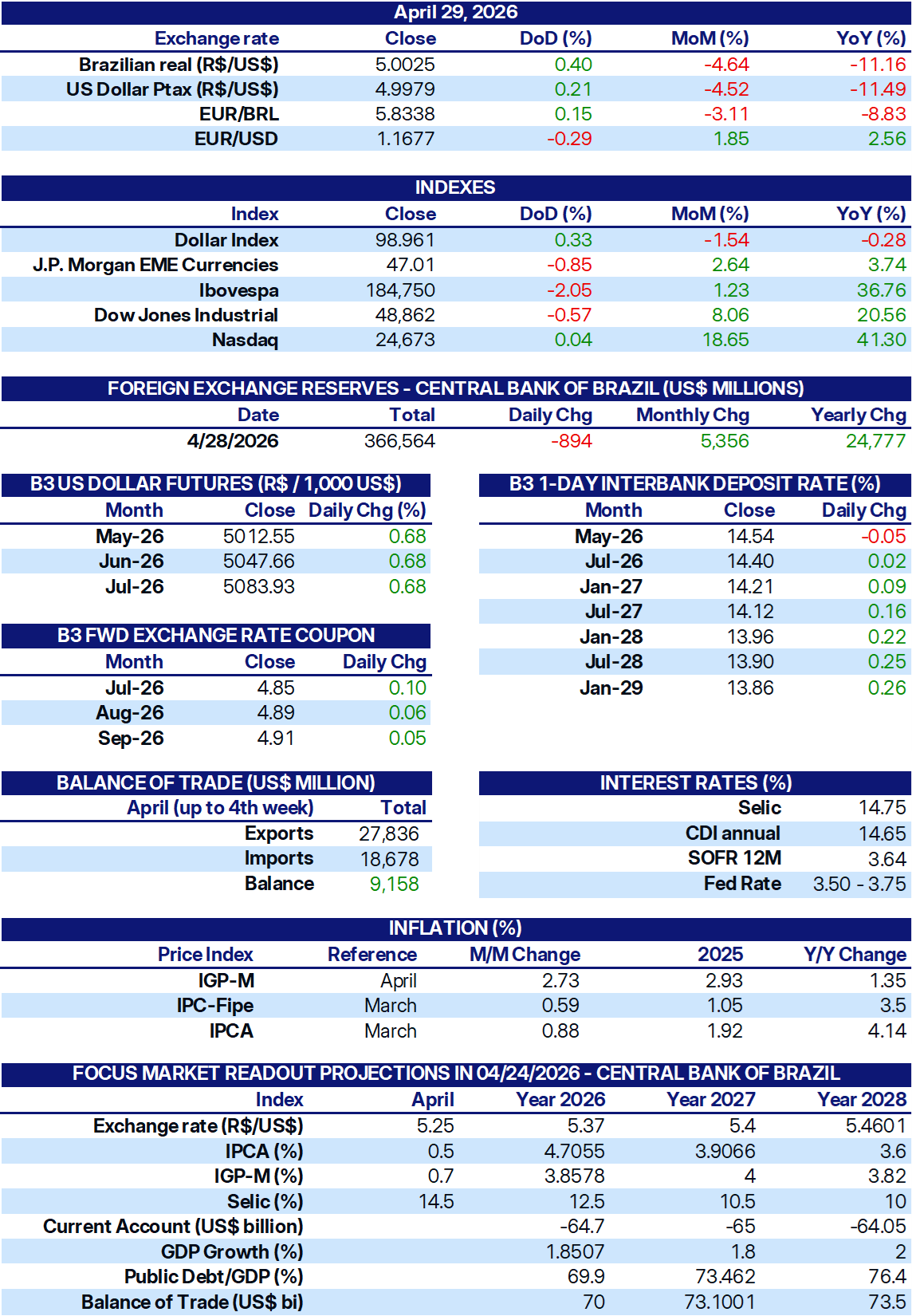

INDICATORS

Sources: Brazilian Central Bank; B3; IBGE; Fipe; FGV; MDIC; IPEA; and StoneX cmdtyView.