Dollar to reflect US economic data, geopolitical tensions in the Middle East, US tariffs, and Brazil's electoral scenario

- Bullish

- The escalation of geopolitical tensions in the Middle East increases investors' risk perception and hampers the performance of assets considered risky, such as stocks, commodities, and currencies of emerging countries.

- The imposition of US tariffs on Brazilian products could harm Brazilian exports and raise the risk perception for domestic assets, weakening the real.

- The release of voter intention polls in Brazil could increase the perception of political risks for domestic assets by investors, weakening the BRL.

- Bearish

- US CPI and PPI to indicate lower inflationary pressures, which is likely to reduce bets on Federal Reserve rate hikes, devaluing the dollar globally.

The week in review

- Geopolitical tensions escalate again in the Middle East after the United States and Iran exchanged military attacks and Donald Trump stated that the ceasefire agreement is "over."

- IPCA surprised by rising 0.16% in June, below the median estimate of 0.32% and the reading of 0.58% in May.

- The minutes of the June Federal Reserve meeting showed a Fed more concerned about inflation but still divided on the next steps for monetary policy.

- Technology stocks fell globally amid concerns over the profitability of investments in artificial intelligence.

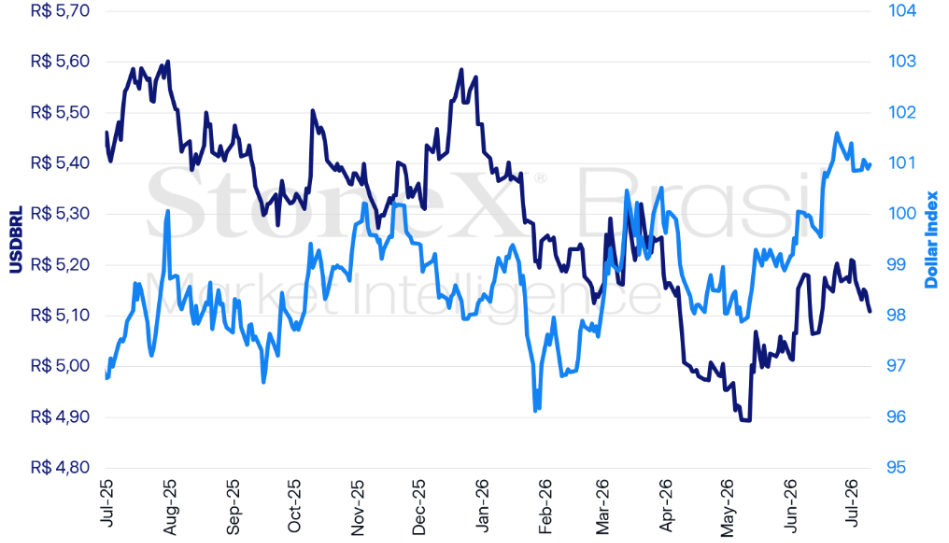

USDBRL and Dollar Index (points)

Source: StoneX cmdtyView. Design: StoneX.

USDBRL Variations | Daily: -0.29% | Weekly: -1.17% | Monthly: -1.10% | Annual: -6.72% | In 12 months: -7.81%

Dollar Index Variations | Daily: +0.07% | Weekly: +0.11% | Monthly: -0.23% | Annual: +2.70% | In 12 months: +3.46%

KEY EVENT: US economic data

Expected impact on the BRL exchange rate: bearish

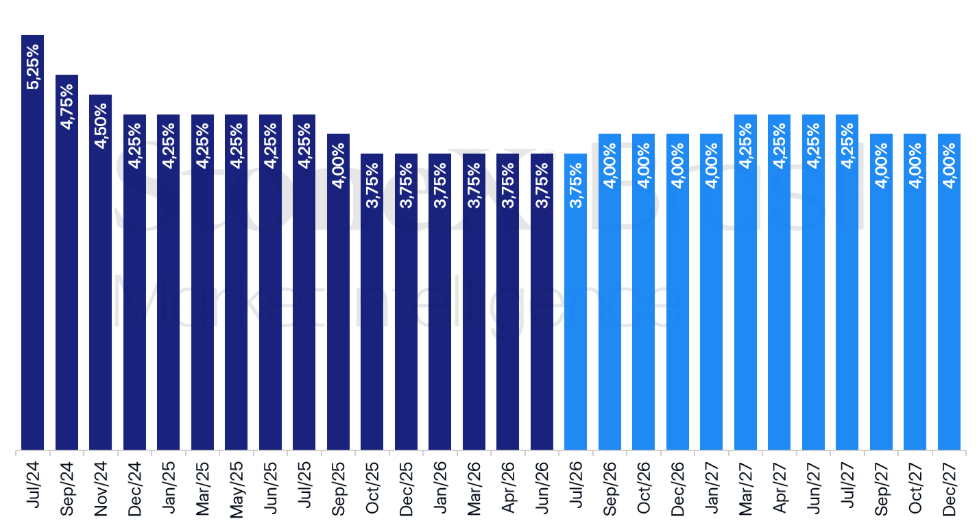

US historical and expected interest rates – updated on July 10, 2026

Source: CME FedWatch Tool. Desing: StoneX. Refers to the most likely outcome in the interest rate futures market on the specified date.

The foreign exchange market is expected to react to the release of US economic data on inflation and economic activity for June.

Why this matters: The easing of inflationary pressures in June is expected to reduce expectations of interest rate hikes by the Federal Reserve, which would hurt the yields on US Treasuries and make it harder to attract foreign capital to the country, thereby weakening the greenback globally.

Forecasts: The median forecast for the Consumer Price Index (CPI) indicates that its monthly change will drop from 0.5% in May to -0.1% in June, driven by the decline in petroleum product prices over the past month.

- The core index, which excludes the volatile food and energy components, is expected to rise from 0.2% to 0.3% over the same period, driven by certain effects of the World Cup, such as higher prices for airline tickets and lodging.

- The median estimate for the Producer Price Index (PPI) also points to a sharp decline in the headline index, from 1.1% in May to 0.2% in June, and to the core index remaining at 0.4%.

- The median estimate for US retail sales, meanwhile, is expected to have declined from a monthly increase of 0.9% in May to 0.3% in June, weighed down by falling fuel prices.

- The indicator’s control group—which excludes sales of automobiles, fuel, office supplies, and construction materials—is expected to show a more modest decline over the period, from 0.7% to 0.5%.

Bets on interest rate hikes: Last week, the renewed escalation of geopolitical tensions in the Middle East led investors to increase their bets on interest rate hikes by the Federal Reserve, anticipating a hike in September and another in March of next year.

- However, the likely easing of inflationary pressures in June may temper those expectations somewhat.

- This cooling trend could help the new Federal Reserve chairman, Kevin Warsh, convince other Fed members to keep interest rates steady for the rest of the year.

- Similarly, the weaker reading earlier this month from the June Employment Situation Report should also ease concerns about a possible overheating of the US economy.

Warsh's Testimony: This week, Kevin Warsh will participate for the first time in the Federal Reserve Chair's semiannual testimony before the US Congress (Tuesday in the House, Wednesday in the Senate).

- Given Warsh’s enigmatic style thus far—refusing to offer any kind of forward guidance or to comment on the economic outlook—the event may provide further clues as to how the Fed chair views the economy and the trajectory of interest rates for the country.

A divided FOMC: Last week, the minutes from the Federal Reserve’s most recent Federal Open Market Committee (FOMC) meeting showed that the Committee was divided on the future of monetary policy.

- While one group believed that inflation could accelerate and that an interest rate hike would be necessary at some point, another group believed that inflation would remain stable or might even slow down, paving the way for future interest rate cuts.

Subtle changes to the minutes: Unlike the Statement, the minutes of the FOMC’s interest rate decision underwent only subtle changes compared to the standard followed under the previous Fed Chair, Jerome Powell.

- The main change was in the wording of the section on the outlook for monetary policy: rather than discussing the most likely trajectory for the US economy—and, consequently, for the country’s interest rates—it now presents a scenario-based approach, that is, identifying which scenarios would lead to a decline in inflation and interest rates and which scenarios would lead to a rise in inflation and interest rates.

- This change is in line with Warsh’s view on “forward guidance,” moving away from a more specific assessment of economic developments and keeping the discussion in broader, more comprehensive terms.

Resurgence of tension in the Middle East

Expected impact on the BRL exchange rate: bullish

On the global geopolitical stage, the Middle East has returned to the spotlight following the escalation of military tensions in the region and US President Donald Trump’s statement last Wednesday (8) that the Memorandum of Understanding between the US and Iran was “over.”

Why this matters: Signs of a possible escalation of military tensions in the region tend to increase investors' perception of risk, hurting the performance of assets considered risky, such as stocks and currencies from emerging markets.

- In addition, the possibility of disruptions to oil flows through the Strait of Hormuz tends to drive up oil premiums, which could lead to global inflationary pressures.

Fears of a supply shock: At the moment, the biggest concern is the possibility of a resurgence in the global energy supply shock and resulting pressures on inflation and key interest rates.

- Since the recent escalation of military tensions in the region, Brent crude has already posted a weekly gain of more than 5%. At certain points during the week, the commodity was trading above $80 per barrel.

- However, it is worth noting that the conflict’s impact on prices appears more contained compared to the early months of the conflict, when Brent reached as high as $120 per barrel.

- In any case, the new rise in oil prices could generate global inflationary pressures, which could hinder the Brazilian Central Bank’s ongoing cycle of interest rate cuts and increase expectations of a more hawkish Federal Reserve.

Low investor sensitivity: In the foreign exchange market, investors appear less sensitive to the renewed escalation of tensions compared to the first few months of the conflict, with the focus shifting to US monetary policy.

- During the week, the dollar index (DXY) rose by nearly 0.1%, a very modest increase compared to the gains recorded in the first weeks of the conflict.

- In this context, the main factors driving the dollar in recent trading sessions appear to be the adjustment of expectations regarding US monetary policy in light of economic data and statements by Kevin Warsh.

Overview: The Memorandum of Understanding signed in June provided for a 60-day window for negotiations on a permanent diplomatic agreement, but the indirect talks in Qatar ended last week without any progress.

- The military escalation began when Iran attacked three oil tankers in the Strait of Hormuz last Tuesday (July 7).

- In response, the United States carried out strikes against more than 80 Iranian targets, including more than 60 small vessels belonging to the Iranian Revolutionary Guard.

- Washington also revoked the license allowing Iran to sell oil, which had been granted on June 22. Iran has until July 17 to complete ongoing transactions.

- Iran, in turn, attacked US military facilities in Bahrain and Kuwait and claimed to have shot down a US drone.

Possibility of tariffs on Brazilian products

Expected impact on the BRL exchange rate: bullish

Investors may also react to announcements of new US tariffs on certain Brazilian products.

- The deadline for determining and imposing tariffs as a result of the recent investigation by the Office of the United States Trade Representative (USTR) is this Wednesday (15).

Why this matters: The imposition of tariffs on Brazilian products could severely harm Brazilian exports, given that the US is the second-largest destination for Brazilian exports.

- This, in turn, would lead to a reduction in foreign currency inflows and cause the real to depreciate.

- Furthermore, this tax increases unpredictability and the perception of risk for investments in Brazilian assets, which deters foreign investment and also tends to cause the Brazilian real to depreciate.

Trade Investigation: The Office of the United States Trade Representative (USTR) announced on June 1 that it had concluded its investigation into Brazil’s “unfair” trade practices affecting US trade.

- These practices are reportedly related to e-commerce, preferential tariffs, anti-corruption measures, intellectual property, access to the ethanol market, and policies to combat deforestation.

- The investigation was requested by US President Donald Trump on July 15, 2025, when he announced 50% import tariffs on Brazilian products.

- As a result, the USTR proposed imposing a 25% surcharge on about one-third of Brazilian exports.

- The proposal includes 73 pages of exemptions for products such as informational materials, donations, certain meats, fruits, coffee, tea, grains, seeds, minerals, rare earth elements, Brazilian aircraft and aircraft parts, as well as organic chemicals, pharmaceuticals, and fertilizers.

- Under US law, the deadline for determining and imposing retaliatory measures is July 15 of this year.

Legal basis: In February of this year, the US Supreme Court ruled that most of the import tariffs imposed by the Trump administration were illegal, as they lacked a legal basis under the International Emergency Economic Powers Act (IEEPA).

- However, this did not apply to sector-specific tariffs based on Section 232 of the Trade Act of 1974, nor to remedial measures supported by an investigation into “unjustified or discriminatory practices” against US trade, based on Section 301 of the same law.

- Last year, the Trump administration took the initiative to seek legal alternatives that would allow for the imposition of tariffs in the event that the courts blocked the use of emergency powers to impose trade barriers.

- Once imposed, Section 301 tariffs can be changed quickly, as the USTR and the Treasury have the authority to adjust, raise, lower, or suspend them without the need for new investigations.

Possible impacts on the electoral landscape: The USTR’s announcement of the proposed tariffs came one week after Senator and presidential candidate Flávio Bolsonaro’s visit to the White House.

- Since, in July of last year, the White House had already linked the imposition of 50% tariffs on Brazilian products to an alleged legal persecution of former President Jair Bolsonaro, political opponents began to claim that the senator had contributed to the new trade threat.

- Aware of the accusation, Flávio filed a petition and participated in a hearing at the USTR, requesting the postponement or suspension of these tariffs on Brazil.

- As a result, there is a risk that the implementation of new tariffs by the United States could harm Flávio’s campaign for the presidency.

Brazilian political and electoral landscape

Expected impact on the BRL exchange rate: bullish

As the national elections approach, domestic financial markets tend to become more sensitive to updates on the election race.

- Two presidential voting intention polls are scheduled to be released next week, one on Monday (13) and another on Wednesday (15).

- The polls are expected to reflect voters’ current views following news reports about the rift among members of the Bolsonaro family and the suspected involvement of Senator Jacques Wagner (PT) in the Banco Master case.

Why this matters: If polls reinforce the prospect of President Luiz Inácio Lula da Silva’s reelection, they are likely to heighten investors’ perception of political risks associated with Brazilian assets, thereby weakening the Brazilian real.

Fiscal concerns: In recent months, investors had already reacted negatively to news related to the election cycle, such as after Luiz Inácio Lula da Silva and Flávio Bolsonaro announced their presidential candidacies.

- In practice, recent reactions from financial market participants reveal a preference for the election of a new president, who might adopt a more conservative fiscal policy.

Recent polls: In the most recent voting intention poll, President Lula led Flávio Bolsonaro by 4 percentage points, 47% to 43%, in a potential runoff election.

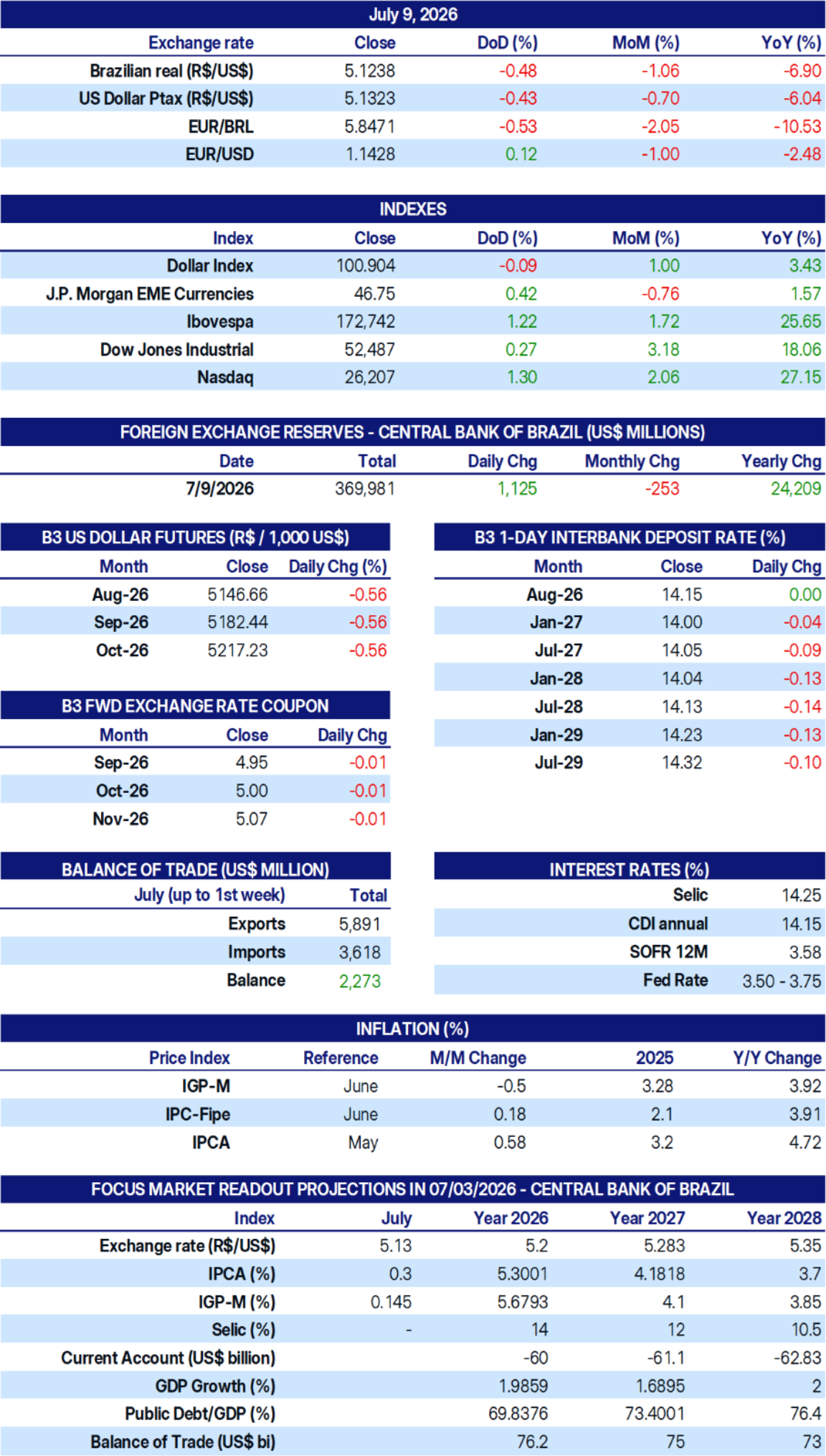

INDICATORS

Sources: Central Bank of Brazil; B3; IBGE; Fipe; FGV; MDIC; IPEA; and StoneX cmdtyView.