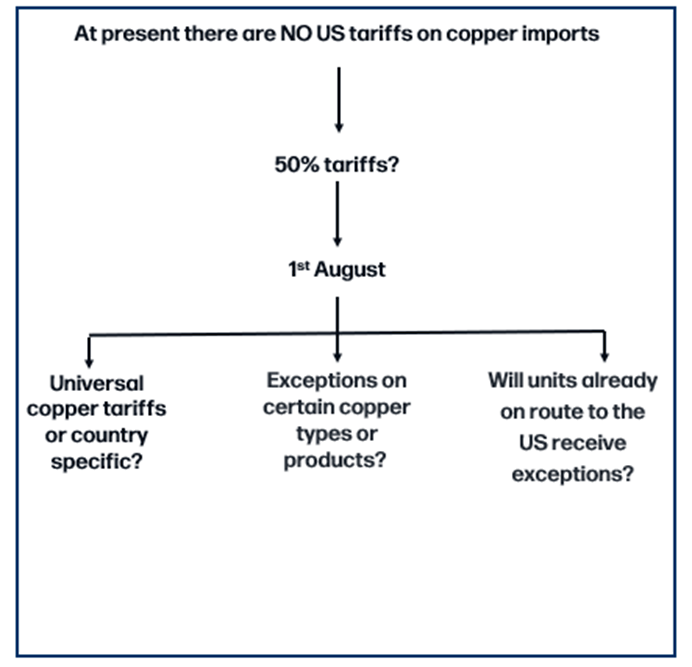

Markets Move to Price in Potential Country Exemption(s) on US Copper Import Tariffs Due on 1st August

Markets Move to Price in Potential Country Exemption(s) on US Copper Import Tariffs Due on 1st August

On 28th July, Chile’s Finance Minister Mario Marcel announced that the country will push for an exemption from planned US copper imports set to come in at 50% on 1st August. This comes hot on the heel of news on Monday that the European Union and the US will develop a metals alliance to mitigate the impact of subsidised Chinese production on global markets, with the EU reported to be granted a quota system with minimal or zero tariffs to replace 50% tariffs on steel, aluminium and potentially copper (although nothing has been put on paper yet). This article will discuss the latest impacts on the copper market and our view for prices over the course of H2.

Source: StoneX

Chile’s Finance Minister Pushes for a Tariff Exemption

On 28th July, Chile’s Finance Minister Mario Marcel announced during a radio interview with Radio Dura:

“What we hope is that these conversations that begin today (28th July) in Washington, also address the topic of copper because it wouldn’t be much use to have a trade agreement that excludes copper and timber, which make up more than half of our exports to the US”.

During Mr. Marcel’s interview, he alluded to potential exemptions being carved out for other countries on sector specific tariffs, noting the UK and steel. Meanwhile, on the same day, details were released over the US-EU trade deal that has been agreed (via a handshake), which includes a potential reduction in copper tariffs to 15% (based on Reuters).

A US-EU Metals Alliance to be Formed

On 28th July, European Trade Commissioner Maros Sefcovic outlined the creation of a metal alliance between the European Union and the US.

"The agreement is clear prospect of joint action on steel, aluminium, copper and the derivatives in what I'd like to call a metals alliance, effectively creating a joint ring-fence around our respective economies through tariff rate quotas at historic levels with preferential treatment”.

"It became very, very clear that if it comes to steel and metals we are not each other's problem”.

"I have to say that despite the strenuous efforts of my colleagues and myself and several long meetings with my Chinese counterparts, unfortunately, the list of the accumulated issues on the table will not get shorter, but just grew longer. "

What Does this Mean?

EU steel and aluminium makers will be granted a quota system with minimal or zero tariffs to replace the 50% import tariffs. Note, the system has not been finalised. European steel exports within the agreed quota would face the most-favoured nation tariff rate agreed under WTO rules, which are low and in some cases zero depending on the steel grade. Steel exports outside the quota would be at 50%. Tariffs on copper and timber will be applied after the conclusion of the 232 investigation, but duties will not exceed 15%.

US- UK Deal on Steel?

The UK is currently facing a lower 25% tariff on imports of steel and aluminium into the US (down from 50% that all other countries have been facing since 4th June). However, Prime Minister Keir Starmer will lobby for reduced tariffs on steel.

Initial Market Reactions Move to Price in Exemption

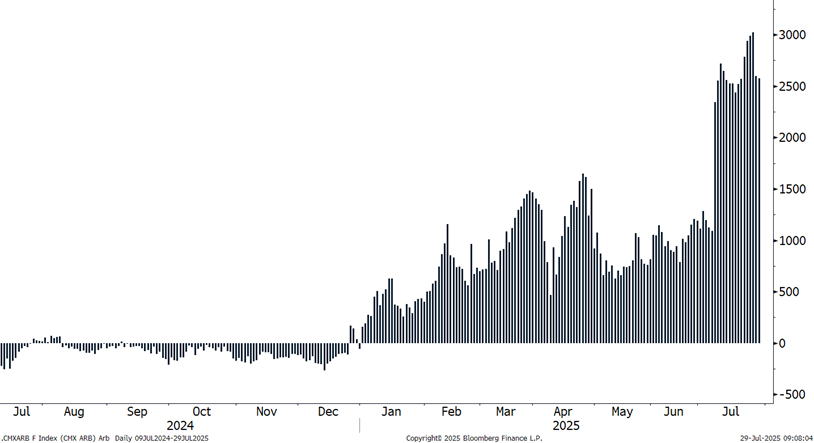

COMEX-LME Spread

Source: Bloomberg, StoneX

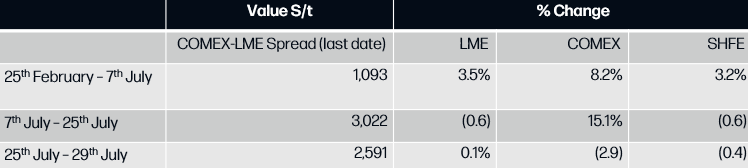

The COMEX-LME spread has fallen to $2,577/t in morning trading (29th July), from above $3,000/t at the start of the week. As it stands the market is moving to price the potential for country exemptions, with the spread reflecting a tariff of 26%, down from 31% last week.

The Markets Have Never Fully Priced in 50% Tariffs – Why?

• Not only is there an excess of US inventory already in the country, set against modest demand expectations for this year.

• There is a risk that we will see a rapid increase in copper inflows into the US ahead of the tariff deadline. Indeed, we understand some material has been waiting on ships outside the US for the opportune time to be delivered.

• In addition, we also expect that major trading partners will do what they can to limit the transit period. For example, South American producers may opt to deliver metal into a port in Puerto Rico, which is a US customs territory, over delivery to the mainland. Asian market players may choose to re-route flows into Hawaii over New Orleans, reducing the transit time from one month down to ten days.

• Furthermore, there remains uncertainty over country-based exemptions and a general sense of tariff fatigue.

Note: US imports of refined copper under HS code 7403 have increased over Jan-May by 680,727t or 127% Y/Y (with imports over April and May accounting for 62% of the total). Based on the assumption that we see a similar level of imports over June, total imports into the US may rise to over 800,000t.

Ships Re-Route to Hawaii to Beat Tariff Deadlines

Source: Bloomberg

Ships En-Route to US Ports from Latin America

Source: Bloomberg, StoneX

Stock Moves Across Exchanges on Major Tariff Announcements in 2025

Source: Bloomberg, LME, StoneX

Note:

• 25th February = Signing of the executive order investigation into US copper import tariffs

• 7th July = President Trump announces tariffs to come in at 50% on 1st August

• 28th July = Chile’s Finance Minister outlines hope for Chile country exemption on tariffs

Price Performance Across Exchanges on Major Announcements in 2025

Source: Bloomberg, LME, StoneX

Note:

• 25th February = Signing of the executive order investigation into US copper import tariffs

• 7th July = President Trump announces tariffs to come in at 50% on 1st August

• 28th July = Chile’s Finance Minister outlines hope for Chile country exemption on tariffs

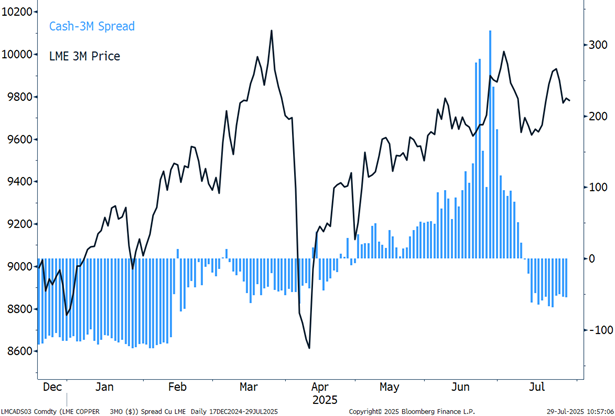

LME Copper Cash-3M Spread Versus LME 3M Copper Price

enter the source here

Our View:

Given the latest developments in the market, including the theoretical lowering of tariffs on sector specific areas (e.g. aluminium and steel for the UK and EU), it is possible that country-based exemptions may take shape when US copper imports tariffs are announced on 1st August.

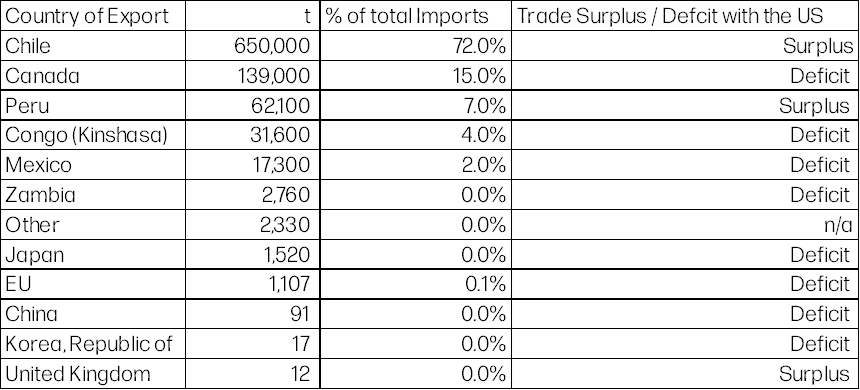

Here, Chile is singled out, not only due to the Finance Minister’s latest comments and ongoing negotiations with the US this week, but due to the US’ significant reliance on Chile imports (standing at 71.5% for refined copper in 2024). In addition to this, the US holds a trade surplus with Chile (alongside Peru and the UK).

In a scenario in which a country exemption such as Chile is outlined, we would expect on 1st August (or earlier), a collapse in the COMEX-LME arbitrage from current levels. Meanwhile, the outlook for LME copper remains in the bearish camp, with trade flows in large part reversing to the east. However, in this scenario it would take longer for depleted stocks in markets of last resort to recover, underpinning LME prices in the near-term. Please note, Chile’s largest import market is China for both refined coper and copper ore.

Meanwhile, if no country exemptions are announced and tariffs come in at 50%, we would expect the COMEX-LME arbitrage to jump to price in the full extent of tariffs in the immediate aftermath, which could see it rise towards $5,000t, before pulling back towards $4,000/t. We expect US copper prices to remain elevated in the medium-term as future supply risks arise once more, given that the US has a 44% reliance on copper imports for demand.

Looking at LME copper prices, in this scenario we forecast a more bearish outlook for prices in the near term, with a high US tariff set to limit the attraction for units into the country immediately. We expect the copper forward curve to widen, as material floods back to the LME warehouses.

Bottom line, the implementation of 50% tariffs is likely to allow LME copper to regain its Dr. Copper status, with prices reflecting the health of the global industrial market, rather than just the risk of US import tariffs, which has been the case for the last few months.

Table of 2024 Country Imports of Refined Copper into the US Versus the US Goods Trade Surplus/Deficit by Country

enter the source here

The US has a 45% reliance on imported copper for domestic consumption, with Chilean imports accounting for 71.5% (based on USGS statistics over 2024).