Precious Metals Talking points 062926: StoneX weekly gold, silver round-up; gold suffers the Death Cross

Politics, economic, geopolitics and investor sentiment

Rhona O'Connell

- Precious Metals

By: Rhona O'Connell, Head of Market Analysis

Weekly round -up for StoneX Bullion; Rhona O'Connell, Head of Market Analysis,

Some interest developing but inflation fears hover overhead

EMEA & Asia, 29th June 2026:

Tel +44 203 580 6115 / +44 7384 833897

|

|

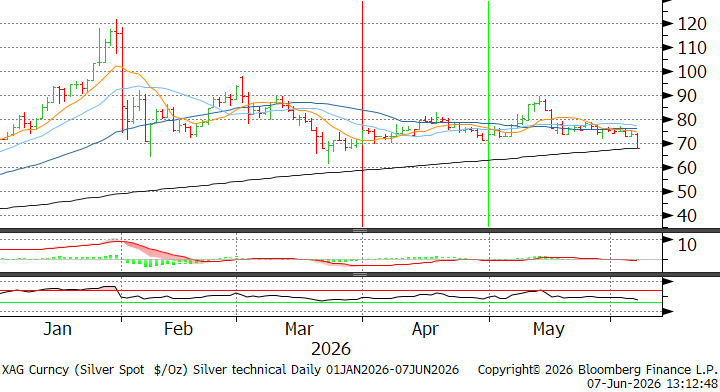

Silver; also below all four with the 20-Day MA about to cross below the 10D.

We have been saying for some weeks that it is axiomatic that extended periods of very narrow range trading do tend to lead to a build-up of pressure and generate a breakout in one direction or the other. The fall across the board in the markets at the end of last week can’t necessarily be called a break-out, but we did at least see some life in the markets as increased geopolitical tensions coupled with much stronger Nonfarm payrolls in the US, announced on Friday, burst a few bubbles, with all four precious metals sliding on rising expectations of at least one rate hike in the States this year. As widely expected, Kevin Warsh will have his diplomatic work cut out with the president seemingly reversing course from his independence comments at Mr. Warsh’s swearing-in ceremony, and calling over this past weekend for a rate cut; but the external parameters point, if anything, in the opposite direction and the bond market is reacting accordingly. That said, these markets are now oversold and the background outlook will depend to some event on whether there is follow-through selling in Asia or whether some bargain hunting starts to appear. Gold is trading below $4,330 and silver below $68. Gold’s key moving averages range from $4,428 (200D) to $4,614 (50D). Silver’s key averages are between $68.4 (200D) and $77.08 (20D). On an RSI basis, both are oversold, silver more so than gold. Gold and silver are both at their lowest since 23rd March. In the professional markets the gold and silver ETFs have remained friendless with continued attrition. The COMEX activity to the week ended Tuesday 26th saw a cautiously bullish move in sentiment (but no such move in the price) with outright longs rising 16t (4%) to 492t and shorts contracting by 30t or 36% to just 54t, the lowest outright short since end-January, when prices peaked; and compared with a 12-month average of 97t. If anything this is a potential bear signal. Over the same period silver crawled from $73 to $76 (before retreating); this was accompanied by a similar pattern to gold but in smaller scope, with a 2.3% gain in outright longs and a 0.2% contraction in shorts; the silver shorts stand at 1,027t, compared with a 12-month average of 1,749t. Gold and the 2Y, 10Y yields: correlation with 10Y, 0.78; with 2Y, 0.77 Source for charts: Bloomberg, StoneX |

Meanwhile the President is now calling for a need for a rate cut despite the evidence to the contrary. The Nonfarm Payrolls, at first glance, point in the other direction but Pantheon Macroeconomics makes the following salient points (among others): - the 172k jump in May was well above consensus forecast, which is ascribed largely to “an erratic jump in local government payrolls”, with private payrolls rising by 120k, leaving the three-month average gain at 166k, the highest since June 2023. Pantheon believes that this momentum is unsustainable because, inter alia

Silver; also below all four major moving averages with the 20D threatening to cross below the 10D

Outlook; mixed

The Core PCE released in the States last week was 4.4%, in line with expectations but still too high for the comfort of the FOMC and, in tandem with healthy Q1 GDP (2.1%, well above expectations) plus comparatively strong consumer spending serves to underpin the clarity of the message coming from new Chair Kevin Warsh and is likely to keep gold under pressure. Fellow members of the FOMC were robust last week in their views; Dean Goolsbee (Chicago) said on Thursday that he saw glimmers of light in the latest inflation figures, but that prices nonetheless are too high “and trending the wrong way”, while John Williams (New York) noted that inflation was “unquestionably elevated” and although the tariff effect has passed through, supply risks due to the Middle East remain “a source of risk to both the growth and inflation outlooks”.

The US Administration is expected to impose wide-ranging tariffs on a number of countries on 24th July (when the current 10% global tariff expires) on the back of concern over counterparties not sufficiently preventing the import of goods believed to be made with forced labour. This includes China, the EU, Japan and India and a certain amount of early purchase and shipping is underway (freight rates are at four-year highs). This may put some further pressure on commodity prices thereafter and silver would most likely be caught up in this. The position is exacerbated by companies also looking to ship goods ahead of any renewed surge in fuel costs.

Gold COMEX positioning, Money Managers (t)

Source: CFTC, StoneX

Source: CFTC, StoneX

COMEX Managed Money Silver Positioning (t)

Source: CFTC, StoneX

Source: CFTC, StoneX

COMEX Managed Money gold positions, as prices eased marginally in the week to 22nd June, saw outright longs expand by just 2.4% or 10t while shorts expanded just over four tonnes or 10%, taking the net long up by just five tonnes to 359t. Silver longs dropped by 6% or 190t to 2,823t while shorts lost less than 1% to 905t, leaving the net long at 1,918t.

Gold ETFs are again friendless. The latest numbers from the World Gold Council date to 19th June, at 4,086t, a 61.8t gain for the year to date; since then, Bloomberg has reported net losses of 20t. Silver ETFs saw some bargain hunting at the end of last week after combined losses of 260t over the course of June. This takes the year-to-date net redemptions to 2,421t or 9% to stand at 24,401t. World Mine production is ~26,300t.

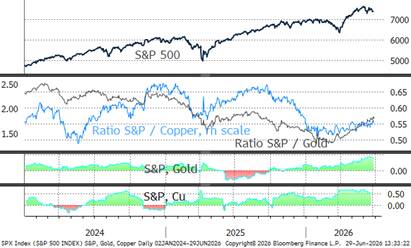

The S&P, gold and copper; S&P/gold rising at 0.57 while S&P/Cu is 0.55

Source; Bloomberg, StoneX

Gold, silver and copper; silver-gold 0.82 (tighter) silver-copper, 0.72 (a lot looser)

Gold:Brent ratio

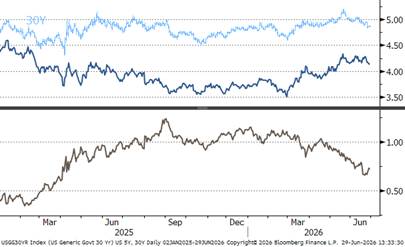

US five-year and 30-year yield

Source for above charts; Bloomberg, StoneX

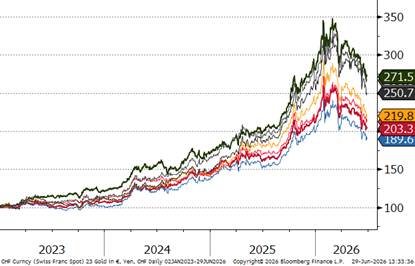

Gold in key local currencies. Year-to-date, up just 4% in Rupee terms now , the strongest of the key measures, but down almost 3% in US$

Gold:silver ratio; expanding to 12-month highs; overbought

Source for above charts: Bloomberg, StoneX

| 29 June 2026 | Previous week | % change | Jan 2025 onwards | Range as % | |||

| Min | Max | ||||||

| Gold (pm LBMA price) | 4,072.05 | 4,150.90 | -1.90% | 53.88% | 1,985.10 | 5,405.00 | 172.28% |

| Silver (LBMA price) | 58.38 | 64.67 | -9.72% | 98.50% | 22.09 | 118.45 | 436.34% |

| Platinum (pm LBMA price) | 1,613.00 | 1,662.00 | -2.95% | 75.14% | 1,589.00 | 2,811.00 | 76.90% |

| Palladium (pm LBMA price) | 1,200.00 | 1,247.00 | -3.77% | 30.29% | 852.00 | 2,106.00 | 147.18% |

| S&P 500 | 7,354.02 | 7,500.58 | -1.95% | 24.50% | 4,688.68 | 7,609.78 | 62.30% |

| $:€ | 1.1384 | 1.1471 | -0.76% | 9.38% | 1.0244 | 1.2041 | 17.54% |

Source: Bloomberg, StoneX

This material should be construed as market commentary and represents the opinions and viewpoints of the author, and does not reflect tailored advice associated with any specific account.

The views are current only through the date stated and are subject to change at any time based upon market or other conditions, and StoneX Group Inc. (“SGI”) disclaims any responsibility to update such views. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. Past performance does not guarantee future results.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided.

References to certain OTC products or swaps are made on behalf of StoneX Markets, LLC (SXM), a member of the National Futures Association (NFA) and provisionally registered with the U.S. Commodity Futures Trading Commission (CFTC) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ and who have been accepted as customers of SXM.

StoneX Financial Inc. (SFI) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (SEC) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Advisor. StoneX Financial (Canada) Inc. (SFCI) is registered in Canada and is a member of CIRO and CIPF. References to certain securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to certain exchange-traded futures and options are made on behalf of the FCM Division of SFI. Wealth Management is offered through SA Stone Wealth Management Inc., member FINRA/SIPC, and SA Stone Investment Advisors Inc., an SEC-registered investment advisor, both wholly owned subsidiaries of SGI.

R.J. O’Brien & Associates, LLC (RJO) is registered with the CFTC as a Futures Commission Merchant and is a member of NFA.

StoneX Financial Ltd (SFL) is registered in England and Wales, company no. 5616586. SFL is authorized and regulated by the Financial Conduct Authority (FCA) (registration number FRN:446717) to provide services to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorized to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorized and regulated by the FCA under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorized by the FCA.

This communication is issued in the European Economic Area by StoneX Financial Europe GmbH (SFEG). StoneX is the trade name used by STONEX GROUP INC. and all its associated entities and subsidiaries. StoneX Financial Europe GmbH (“SFEG”) is a securities trading firm registered in Germany under Company No. HRB 80844.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism. SAP is an “Approved International Trading Company” authorized to act as a “Spot Commodity Broker” under the Commodity Trading Act.

StoneX Financial Pte Ltd (Co. Reg. No 201130598R) (“SFP”) is regulated by the Monetary Authority of Singapore and is a Capital Markets Service Licence holder (for dealing in capital market products), an Exempt Financial Adviser (for advising on investment products and issuing or promulgating analyses/ reports on investment products) and a Major Payment Institution (for domestic and cross-border money transfer services).

SFP may distribute analysis/report produced by its respective foreign affiliates within the StoneX Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations Recipients should contact SFP at (65) 6309 1000 for any matters arising from, or in connection with, this webinar.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism.

StoneX Financial (HK) Limited (CE No.: BCQ152) (“SHK”) is regulated by the Hong Kong Securities and Futures Commission for Dealing in Securities and Dealing in Futures Contracts.

StoneX Financial Pty Ltd (ACN 141 774 727) holds an Australian Financial Service License (AFSL: 345646) for Dealing in Securities, Exchange-Traded Derivatives Contracts, OTC Derivatives Contracts and Foreign Exchange Contracts, and is regulated by the Australian Securities and Investments Commission.

StoneX Securities Co., Ltd. (“SSJ”) (Co. Reg. No 010401047199) is regulated by the Japanese Financial Services Agency as a Type-I Financial Instruments Business Operator (Kanto Local Finance Bureau (FIBO)No.291’), is a member of the Financial Futures Association of Japan for dealing and broking FX and FX Option transactions, and is a member of the Japan Securities Dealers Association for dealing and broking stock indices and option transactions.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

The report/analysis herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

© 2026 StoneX Group Inc. All Rights Reserved.

Our subscribers have access to comprehensive market analysis from StoneX spanning commodities, equities, currencies and more.

Politics, economic, geopolitics and investor sentiment

Politics, economic, geopolitics and investor sentiment

Gold has fallen to a seven-month low as a surging U.S. dollar and Federal Reserve rate hike expectations dominate trader sentiment. Falling oil prices and lower Treasury yields are providing no relief, leaving precious metals exposed to further losses below key technical levels.

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bi-lateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve; our financials and record of accomplishment are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform, to “boots on the ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.