- Bearish Factors

- Global 24/25 production significantly above consumption, according to USDA;

- Still comfortable US supply-demand balance;

- Concerns over global demand pace;

- StoneX increases record production estimate for Brazilian 24/25 crop;

- Harvest season in the US;

- Accelerated planting in Brazil.

- Bullish Factors

- New incentive measures adopted by the Chinese government;

- Speculative funds with net short positions;

- Strong renewable diesel production and consumption in the US;

- Reduction in US production estimate, which is no longer a record;

- Fed's start of rate cut cycle.

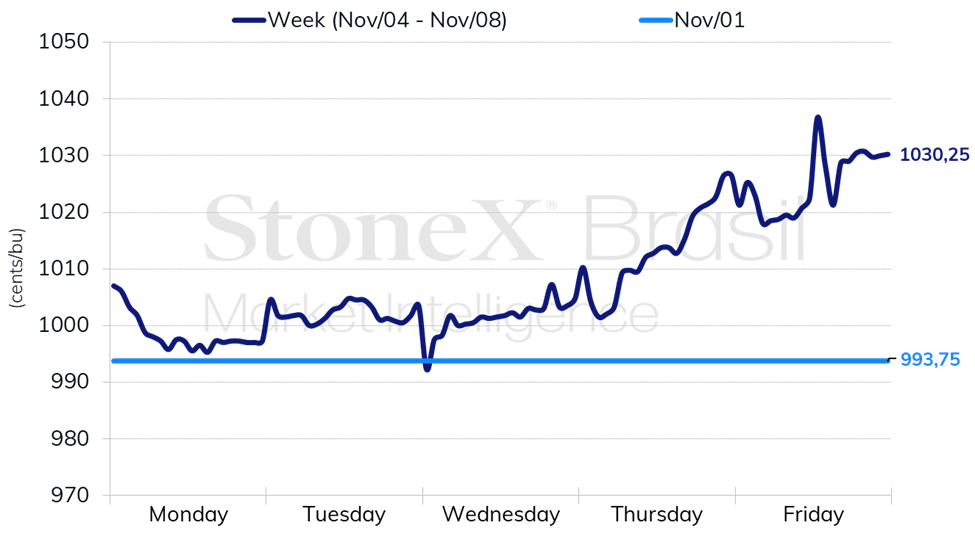

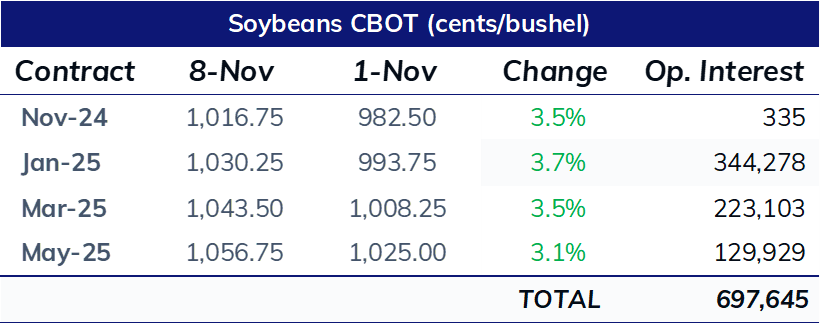

Last week, soybean prices in Chicago increased, with the January contract ending Friday (8) at 1030.25 cents per bushel, up 3.7% over the period, returning to above USD 10.00 per bushel. Highlight goes to the revision of the 24/25 US crop data, while in Brazil, perspectives remain favorable as soybean planting progresses.

StoneX USA revised its crop survey, considering USDA's official planted area and adjusting yield. The soybean production figure fell to 123.5 million tonnes, 2 million less than October's estimate, with national average yield down from 3.6 to 3.54 million tonnes. These adjustments were mainly due to lower yields in the eastern belt, which was more impacted than previously expected by drier conditions. Even so, the resulting output still represents a record.

On Friday (8), the USDA's monthly report surprised with a larger cut to the 24/25 US soybean production, dropping it to 121.4 million tonnes, a level that, if confirmed, is no longer a record, slightly below the 21/22 cycle, when it reached 121.5 million tonnes. National yield fell from 3.57 to 3.48 tonnes per hectare, with notable declines in major producing states like Iowa and Illinois.

With this reduction of over 3 million tonnes in 24/25 US production, ending stocks are also down, now at 12.79 million tonnes. However, this reduction was partially offset by cuts to expected crush and exports. Even with the drop in US production, the country's supply-demand balance remains comfortable.

For other major soybean market players, the USDA report made no changes, with adjustments in the US balance reflecting in global data, with global production at 425.4 million tonnes, more than 20 million tonnes above projected consumption.

The USDA continues to estimate domestic consumption and Chinese imports above the expectations of the Chinese government, even exceeding the USDA attaché in China, who predicts 104 million tonnes to be imported in the 24/25 cycle, versus the 109 presented in the monthly supply-demand report. Nonetheless, Chinese imports have remained strong in recent months, with official customs data showing 8.09 million tonnes in October, the second-highest volume ever recorded for the month.

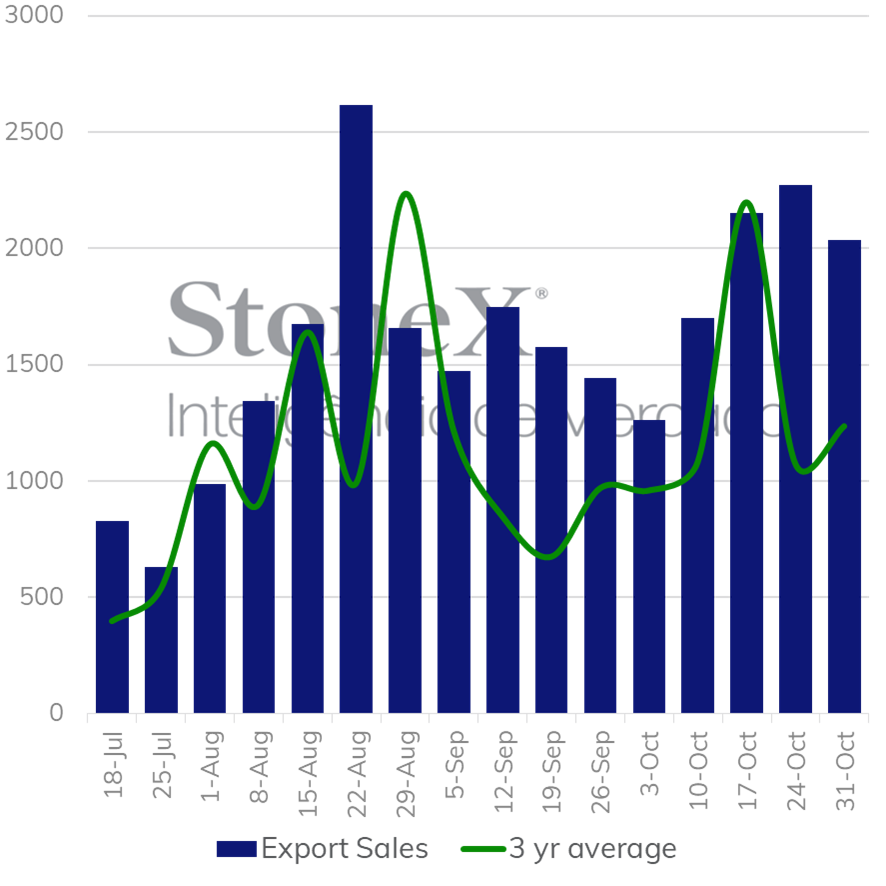

Notably, China was the largest buyer of US soybeans in the week ending 10/31, accounting for 1.22 of the 2.04 million tonnes traded in the period. In total for all destinations, 28.3 million tonnes were traded, up from 24.2 million tonnes a year ago.

In Brazil, after initial planting delays, prospects for the 24/25 crop remain positive. According to StoneX monitoring, as of Friday (8), 68.4% of the 24/25 soybean area was planted. All states tracked have surpassed last year's percentage, with the national average 9.3 percentage points higher than the same week in 2023. However, the soybean cycle is still in its early stages, and weather over the coming weeks and months will be key in confirming the record production estimates. It's important to remember that excessive rainfall can also cause damage.

Over the next seven days, heavier rainfall is expected in parts of the Southeast and Center-West, with lighter precipitation in the South.

StoneX also updated its bi-weekly commercialization monitoring, with 23/24 cycle sales reaching 91.6%, slightly above last year’s 89%. Soybean sales for the 24/25 crop are at 29.8%, compared to 25.6% last year.

This week, the South American crop will remain in focus, particularly with the release of the next Conab report on Thursday (14). Additionally, any demand data, particularly for US soybeans, which are in peak export season, could move the market. It's worth noting that Mississippi River levels have improved in the US, with higher-than-expected rainfall in parts of the Midwest, resulting in lower barge freight rates.