Join us next week for Kathryn Rooney Vera’s 2024 Economics & Market Strategy Outlook Conference Call on Tuesday, March 5, at 11:00am ET featuring many of StoneX's top experts, including Eric Rose - StoneX Digital’s Head of Digital Asset Execution. Register here:

StoneX 2024 Outlook Virtual Event

Summary

- Market trading color: Bitcoin and Ethereum experienced notable monthly price surges of 48% and 53%, respectively, alongside increasing open interest in futures contracts

- Theme of the week – Uniswap earnings distribution proposal and what is Eigenlayer and how does it tie in with modularity?

- Sector commentary: Bitcoin climbs, DeFi expands to Africa, NFTs update with MetaMask, Avail funding, and $90B funding for crypto projects

Market Trading Color (Nolan Aibel)

While we usually focus on weekly statistics on this note, given we’re at month end we figured it was worth pointing out that $BTC is up 48% in February, its largest monthly gain since December 2020. On the same monthly timeline, $ETH has risen over 53%. Both have major catalysts coming in the months ahead. Bitcoin should continue to see volume and inflows for their spot ETFs. Couple this with the halving coming up in April. Ethereum has its much anticipated Dencun upgrade in March which comes with the development of restaking and potential spot ETF with initial deadline in May.

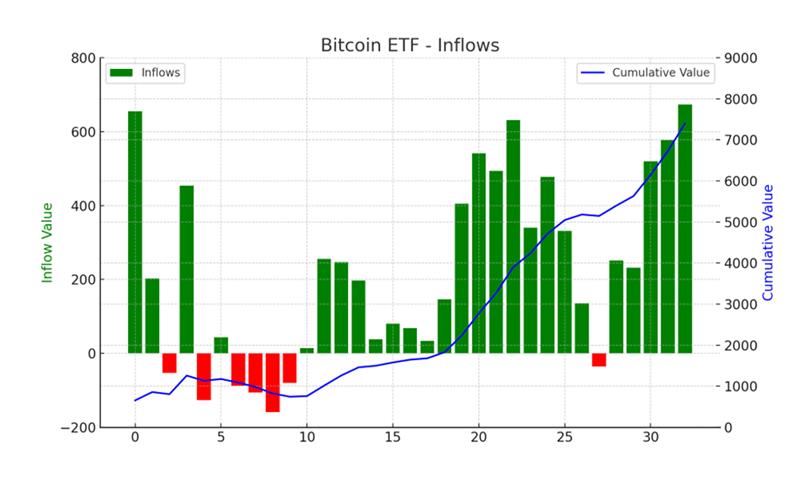

Source: BTC_Archive @ X

Despite $216M in outflows from $GBTC, $BTC ETFs saw record inflows of $673M yesterday. Blackrock’s $IBIT saw $612M of these inflows and is now well on their way to $10B in AUM, currently sitting at $9.1B. For context, it took $GLD over two years to hit the $10B mark.

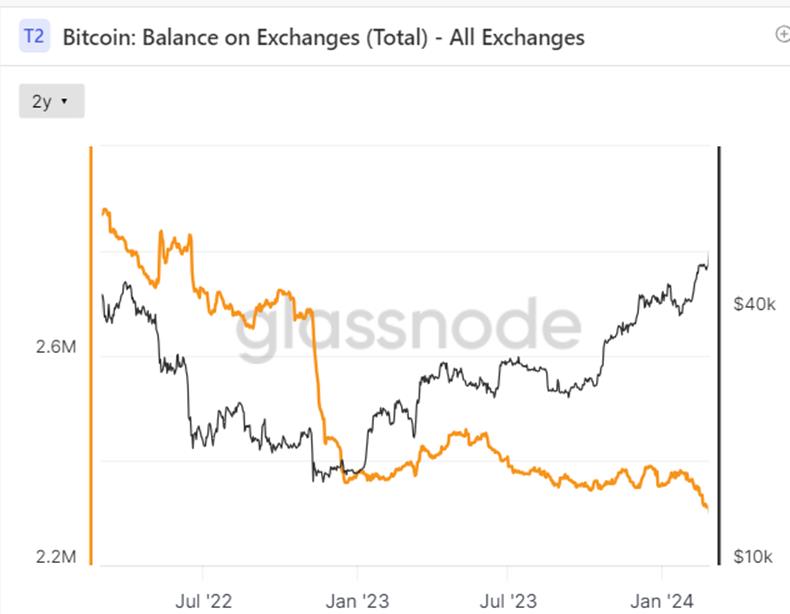

Source: Glassnode

Zooming out, the ETFs took in over 11,000 $BTC yesterday while miners mined their daily rate of 900 new $BTC. As you could see above, the total amount of $BTC on exchange has continued to shrink over the past two years with just over 2 million of $BTC currently on all exchanges. With these numbers, the $ETFs took in about 0.5% of the total supply yesterday. Now keeping in mind the trading supply of Bitcoin will half in 51 days and we have supply crunch on our hands. The main question is where does supply and demand balance out?

Source: Derebit

We’re seeing a large increase in open interest over the course of the month. On Feb 1, open interest was just over 210k contracts. Open interest now sits above 280k contracts. The majority of this increase coming from upside call buyers. For March end, we’re seeing heavy open interest around 70k and 75k. This has led to the spike in implied volatility that we’ve seen of late with Implied now well above realized.

Uniswap

The Uniswap Foundation has put forth a proposal to distribute earnings from the Uniswap fee switch to UNI stakers and delegates, causing a notable surge of +60% in the token's value on February 23rd. This development has sparked additional speculation within the DeFi community, as one of the largest protocols in the field is taking such a significant step. The positive market response has led to discussions on whether other projects will follow suit, with the FRAX team already advancing a proposal to distribute revenue to veFXS stakers. This movement suggests a growing trend among profitable projects to explore avenues for returning value to their token holders, potentially reshaping narratives around protocol fundamentals and governance mechanisms.

With the UNI fee switch potentially turning "valueless governance tokens" into mechanisms for value accrual, there are intriguing prospects for these tokens to evolve into productive assets with underlying yield. The recent surge in UNI's price to a two-year high at $12.73, accompanied by increased trading volume, reflects market interest and a positive outlook towards the proposed governance enhancements. The anticipation among the Uniswap community and stakeholders for the upcoming governance overhaul, scheduled for a snapshot vote on March 1 and an on-chain vote on March 8, 2024, further underscores our thesis that fundamentals become a louder part of narratives for protocols and sectors.

What is Eigenlayer?

EigenLayer, a protocol on Ethereum, introduces restaking, a concept in cryptoeconomic security, allowing users to reuse their ETH on the consensus layer. By opting into EigenLayer smart contracts, users can restake their ETH or liquid staking tokens (LST), extending security to various applications and earning additional rewards. This pooled security approach reduces capital costs for stakers and enhances trust guarantees for services, fostering permissionless innovation on Ethereum.

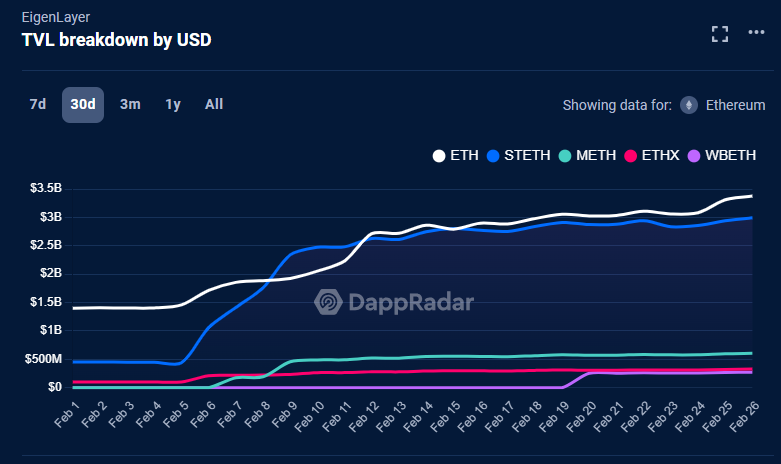

EigenLayer's liquid restaking platform has swiftly risen to become the fourth-largest protocol in decentralized finance (DeFi), attracting $4.3 billion in inflows within just 10 days. Removing its staking cap on Feb. 5 aimed to boost organic demand, leading to a $600 million increase in total value locked (TVL) despite closing the restaking window on Feb. 10. Currently holding nearly $8.8 billion in TVL, EigenLayer's surge mirrors DeFi's broader trend, with TVL across DeFi protocols doubling since October to reach $79.2 billion. Restaking platforms like ether.fi have also seen an increase, from a TVL from $350 million in December to $10 billion.

EigenDA

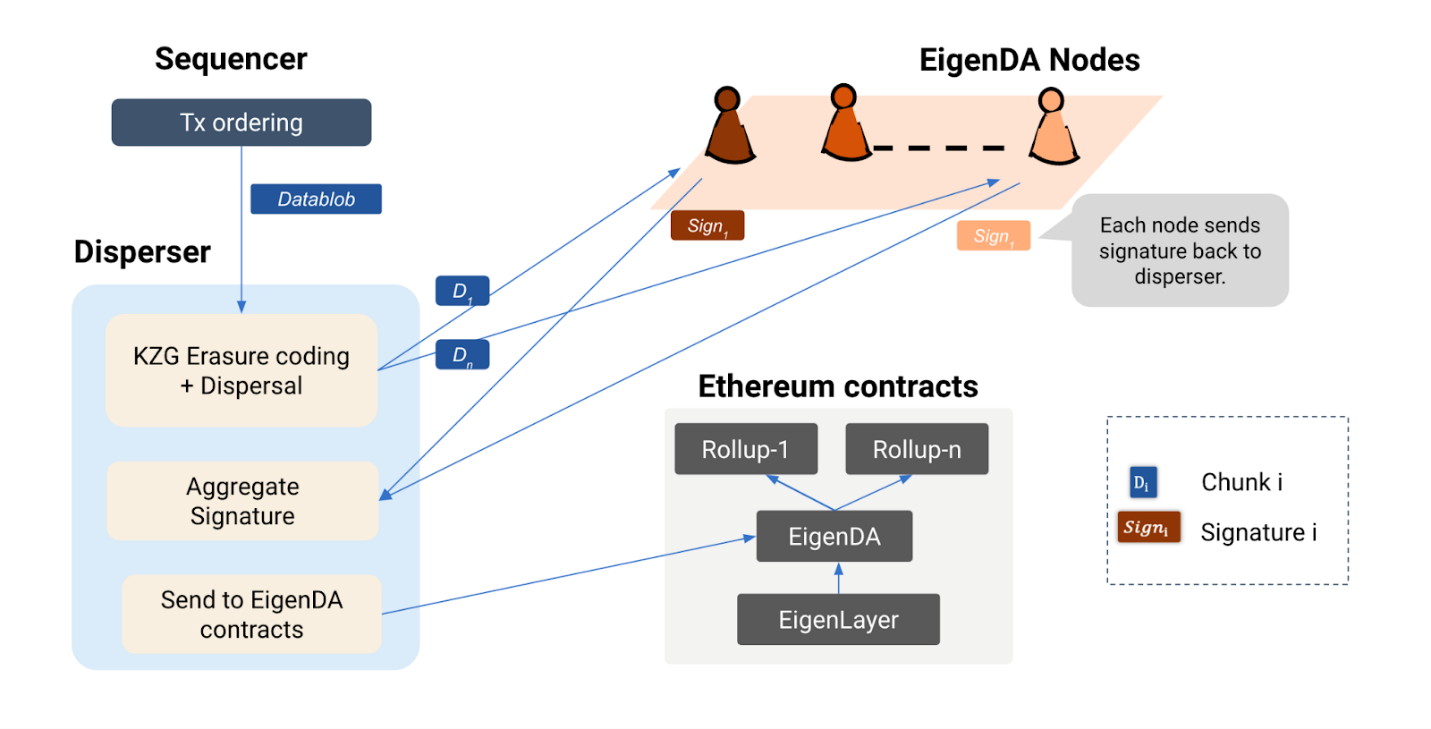

EigenLayer's Data Availability (DA) layer stands as an important modular component within its ecosystem. At the heart of EigenLayer's architecture, the DA layer addresses critical challenges surrounding data storage, accessibility, and security, laying the foundation for hyperscale performance and seamless user experiences. With innovative features such as Erasure codes and zero-knowledge polynomial cryptography, EigenLayer's DA layer ensures efficient data storage while upholding stringent security standards. EigenLayer's modular architecture allows for versatility and flexibility in staking options. This system supports multiple Ethereum-based tokens, including ETH, stETH, mETH, eTHX, and wBETH, catering to a wide array of investor preferences.

Source: DappRadar

The flow of data through EigenDA can be broken down into several key steps:

- Rollup Sequencer Request: Initially, the rollup Sequencer generates a block containing transactions and sends a request for data dispersion.

- Data Dispersal: The Disperser, responsible for data dispersion, divides the data blobs into smaller, manageable chunks. It applies erasure encoding to these chunks, generating a KZG commitment and multi-reveal proofs. These components, along with the chunks themselves, are then sent to the operator nodes of the EigenDA network.

- Rollup Option: Rollups can either operate their own Disperser or utilize a third-party service, such as EigenLabs, for convenience and to reduce signature verification costs.

- Optimistic Usage: Rollups can also employ a third-party service optimistically. In this scenario, if the service becomes unresponsive or engages in censorship, the rollup can seamlessly switch to its own Disperser. This approach ensures both amortization benefits and censorship resistance.

- Node Verification and Storage: EigenDA nodes verify them against the KZG commitment using multi-reveal proofs upon receiving the chunks. Once verified, the nodes store the data locally. Subsequently, they generate a signature and return it to the Disperser for aggregation.

Source: Eigenlayer

In his technical presentation in January 2023, Eigenlayer founder, Sriram Kannan introduces EigenDA, EigenLayer's data availability service, designed to meet the demands of hyperscale gaming applications. He outlines its features, including Erasure codes and zero-knowledge polynomial cryptography, enabling efficient data storage and high security. Kannan emphasizes EigenDA's low latency and verifiability, which are essential for supporting complex gaming infrastructures. Lastly, he discusses integrating staking mechanisms within EigenLayer's ecosystem, showcasing how this enhances security and decentralization for gaming systems built on top of EigenLayer. The modular setup allows investors to choose staking options that offer higher returns than traditional methods, compounded by the potential of additional rewards through airdrops.

Airdrop

EigenLayer has been incentivizing Ethereum holders by leveraging a dashboard point system. The points system associated with EigenLayer's airdrop aims to incentivize user engagement within the protocol's ecosystem. Users can earn points through various activities on the mainnet, such as connecting a Metamask wallet, acquiring ETH, restaking through supported platforms, and interacting with projects built on EigenLayer. Additionally, participation in EigenLayer's testnet phase offers another avenue for accumulating points, where users can engage with the environment using Goerli ETH to test features and functionalities, potentially qualifying them for an airdrop.

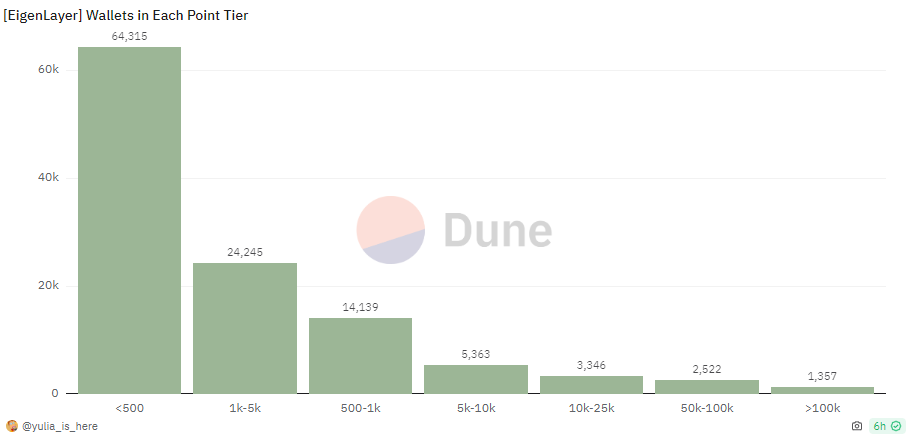

The data from the graphs shows the distribution of points by the number of wallets within EigenLayer. A significant number of wallets, 64,315, engaged at the lower end of the point spectrum, shows that the platform is attracting a wide number of users.

Source: Dune Analytics @yulia_is_here

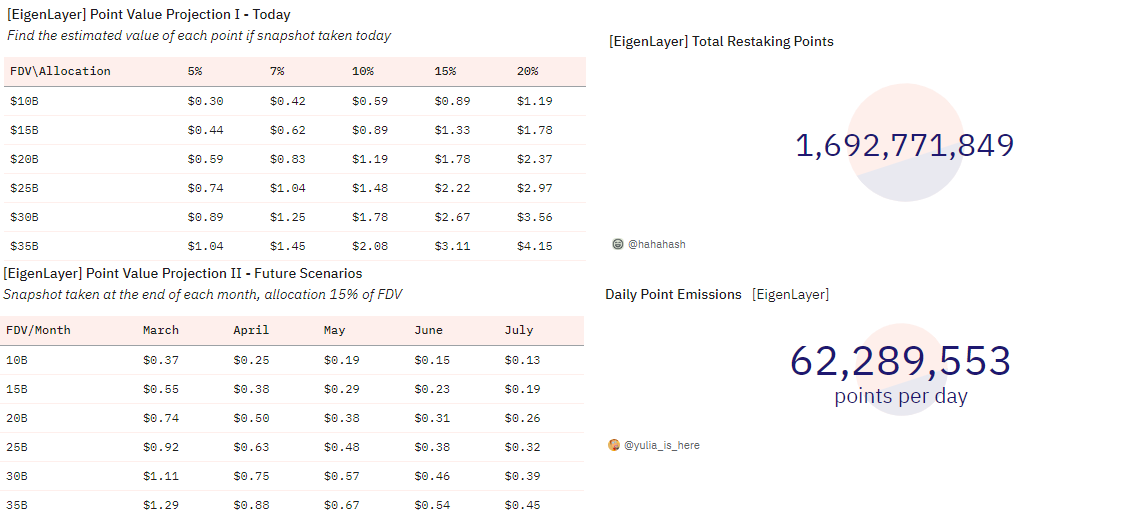

The graphics on the right show prolific issuance of points, highlighted by the daily point emissions totaling 62,289,553 points. This emission rate indicates the platform’s active reward system, which could translate into substantial value for users through potential airdrops. Point-value projections on the left, provides users with a sensitivity table to help gauge potential rewards based on current accumulated points. FDV stands for fully diluted value.

Source: Dune Analytics @yulia_is_here

Users need to note that while staked ETH deposits into EigenLayer are currently permitted and can be freely withdrawn, the actual rewards, contingent upon EigenLayer’s Mainnet’s successful launch, will only become redeemable after the Automated Validator Services (AVSs) become operational.

Slashing

EigenLayer employs slashing mechanisms to ensure cryptoeconomic security by imposing a high cost of corruption. The terms and conditions for slashing are laid out in the slashing contract of each service. By choosing to restake with a particular service, stakers acknowledge the risk of being subjected to slashing as per the rules outlined in the contract. Restakers who opt-in to EigenLayer earn additional rewards on their staked ETH, while validators who participate gain additional revenue from the services that benefit from their validation operations. Whenever there is a dispute, EigenLayer uses the service's slashing contract to verify if the staker acted maliciously and then applies the appropriate penalty.

Stakers choose to delegate to operators based on multiple criteria:

- Trust of operator. A staker must do due diligence on operators before delegating its stake to an operator, because if their delegated operator doesn't fulfill its obligations in the services it participates in, then staker assets will be subject to slashing.

- Rewards. Stakers might delegate to operators that offer maximum rewards on delegated stake.

- Preference for services. Stakers may prefer services based on their personal interests, due diligence on slashing risks, or rewards, and hence they may delegate their stake to only operators who are opted in to those particular services.

Risk on EigenLayer

EigenLayer's approach to risk management in the Ethereum ecosystem aims to promote responsible decentralization while minimizing slashing risks for Ethereum and external protocols. The implementation of a slashing veto committee helps internalize social consensus, providing a safeguard against unwarranted slashing risks. This committee functions similarly to relays in MEV-Boost, operating on a double-trusted basis where trust is placed by both proposers and builders. The EigenLayer DAO reviews contested slashing incidents, leveraging people handpicked in their respective fields like MEV and memory storage to determine the nature of the slashing incidents and who is in the right or wrong. This is a very centralized process right now, of which Eigenlayer is actively looking to change.

Outside of centralization concerns, potential risks arise from restakers prioritizing higher yields, perceiving restaking as speculative, leveraged financial product, impacting Layer 1 on Ethereum. Additionally, reliance on centralized actors issuing LSTs may introduce centralization, concerning Ethereum's consensus mechanisms. Vitalik Buterin and Ethereum developers caution against overloading consensus, redirecting staked ETH to new threats.

Source: X

To mitigate these risks, strategies such as optimizing restaking parameters and diversifying funds among for AVSs are being considered. Despite EigenLayer being live on the Ethereum mainnet, not all functionalities outlined in its whitepaper, such as AVS and slash functions, are fully realized. The current slash function lacks complete logic and is triggered by the owner of the StrategyManager contract, which is the large degree of centralized control mentioned earlier. Strategies are currently being discussed to further lower the risks mentioned above.

Source: Eigenlayer, Uniswap, X, DappRadar

Sector Commentary

- Layer One / Altcoins

- Bitcoin ($BTC): Crypto recaptures $2 trillion market cap as Bitcoin climbs above $57,000 (link)

- Bitcoin ($BTC): Bitcoin Shorts Lose $150M as BTC Poised for ‘Tremendous Upside’ (link)

- Bitcoin ($BTC): Op-Ed: 5 Things Satoshi Nakamoto Correctly Predicted About Bitcoin (link)

- Ethereum ($ETH): Ether Demand Is Driven by U.S. Investors, Data Shows (link)

- Ethereum ($ETH): Ether's Bitcoin Beating Rally Not Just Because of Potential ETF Approval: Bernstein (link)

- Ethereum ($ETH); Solana ($SOL): PEPE and WIF Jump 50%, Putting Ethereum and Solana Meme Coins in Focus (link)

- Uniswap ($UNI): Uniswap's 38% Advance Leads CoinDesk 20 Gainers Over the Past Week: CoinDesk Indices Chart Pack (link)

- DeFi

- Bitcoin-Focused Payments App Strike Rolls Out Services to Africa (link)

- Days After Ditching Aave, Risk Manager Gauntlet Moves to Rival Lender Morpho (link)

- Uniswap token pumps following governance fee switch proposal (link)

- Stablecoin USDC Is Making a Comeback: Coinbase (link)

- Op-Ed: Risk Management in DeFi: Paternalism vs. the Invisible Hand (link)

- NFTs / Web3

- Nifty News: Yuga cuts non-royalty markets, South Korea to discuss NFTs with Gary Gensler (link)

- MetaMask Introduces Real-Time Scam Alerts to Combat Fraud (link)

- Peter Thiel's Founders Fund co-leads $27 million seed round for modular blockchain project Avail (link)

- Crypto projects have received over $90 billion in all-time funding (link)

- Metaverse / Gaming

- Digital Infrastructure: Capital Markets / Exchanges / DAOs / Mining

- BlackRock Bitcoin ETF Heads for Second Consecutive Day of Over $1B Volume (link)

- As spot ETFs grow, bitcoin liquidity transforms from 24/7 to traditional Monday-Friday trading (link)

- MicroStrategy buys additional 3,000 bitcoin, taking total holdings to 193,000 BTC (link)

- Tether CEO Paolo Ardoino predicts more bitcoin buy-in from funds post spot bitcoin ETF approval (link)

- Polygon’s Colin Butler Op-Ed: “New Technology Will Have Institutions Lining Up for Crypto” (link)

- AI tokens rally amid Nvidia’s breakout earnings (link)

- “Crypto Exchanges, Retail Brokers and the Fight for Day Traders” (link)

- Eyeing Coinbase's bitcoin custody dominance, Kraken launches institutional service (link)

- HTX Withdraws Hong Kong Crypto Exchange Application (link)

- Crypto Exchange OKX Enters Turkey as Part of Global Expansion Plan (link)

- Judge Signs Off on Binance's $4.3B Plea Deal With U.S. Prosecutors (link)

- Republican Lawmakers Introduce Legislation to Ban a CBDC in the U.S. ... Again (link)

- Do Kwon likely won’t be extradited ‘before the end of March,’ say lawyers (link)