Prospects for increased production in the 2022/23 crop may reverse the scenario observed in 2021/22

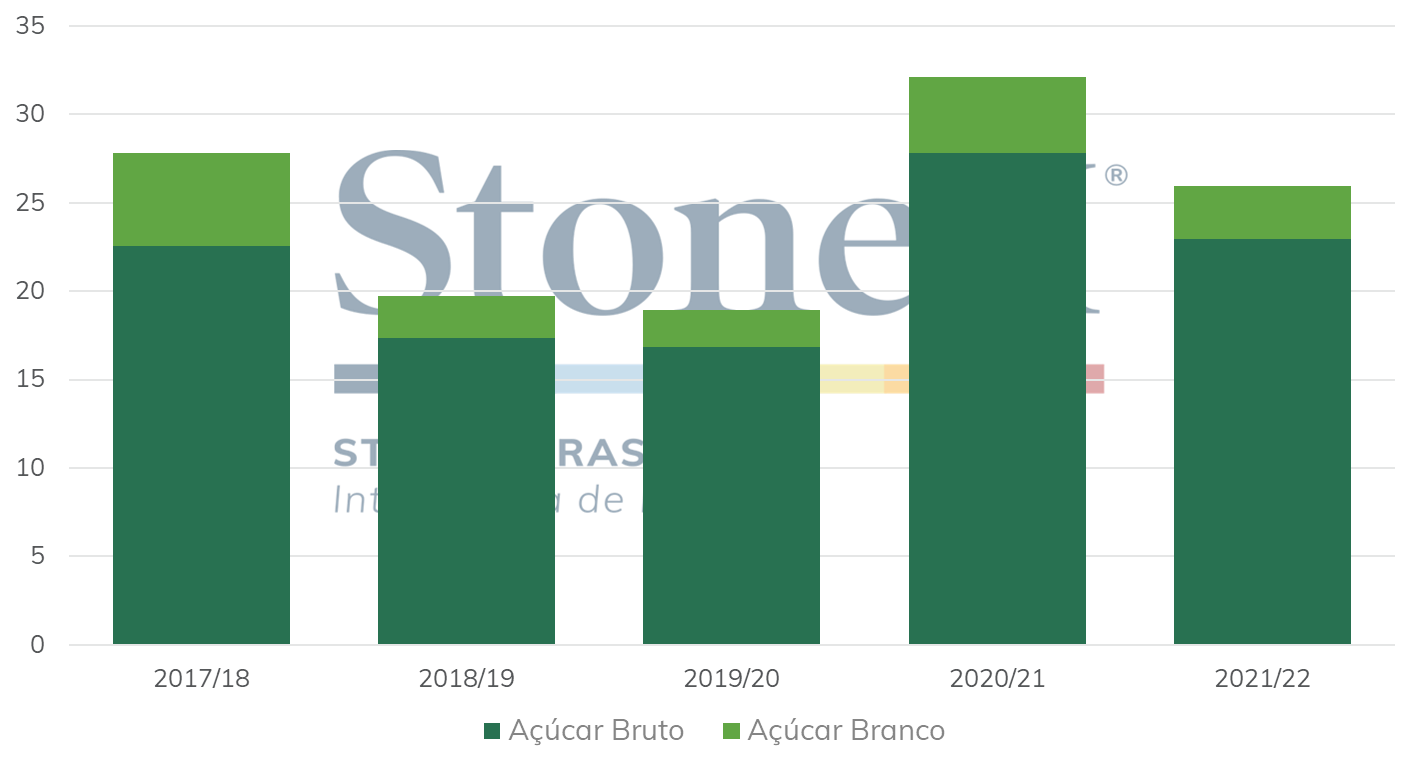

Sugar sales to the foreign market in the 2021/22 crop reached around 25.9 million tonnes, of which 22.9 million were raw sugar and 2.9 million were white sugar, corresponding to a 19% reduction from the previous cycle. White sugar shipments dropped by 30%, while raw sugar had a decrease of 17%.

Weather impacts, such as the lack of rainfall and heavy frost, damaged the progress of sugarcane harvest in the entire Center-South of Brazil (CS), which recorded the lowest crushing volume of the last 10 years at approximately 525 million tonnes, a 13% reduction in relation to the previous season.

Just like crushing, the total recoverable sugar (TRS) and tonnes of cane per hectare (TCH) indices also dropped. Average TRS compared to the 2020/21 crop dropped by approximately 1.5% and TCH lost about 14%.

When the results of the 2020/21 crop are compared against 2019/20, there were significant increases in sugar and ethanol exports, with gains of 70% and 53%, respectively. However, this scenario was reversed in the 2021/22 season, mainly influenced by reduced crop productivity, lower domestic supply, and an earlier inter-crop period in some of the CS areas, which contributed to higher sugar prices on the domestic market.

Exports of raw and white sugar (million tonnes)

Source: ComexStat. Design: StoneX.

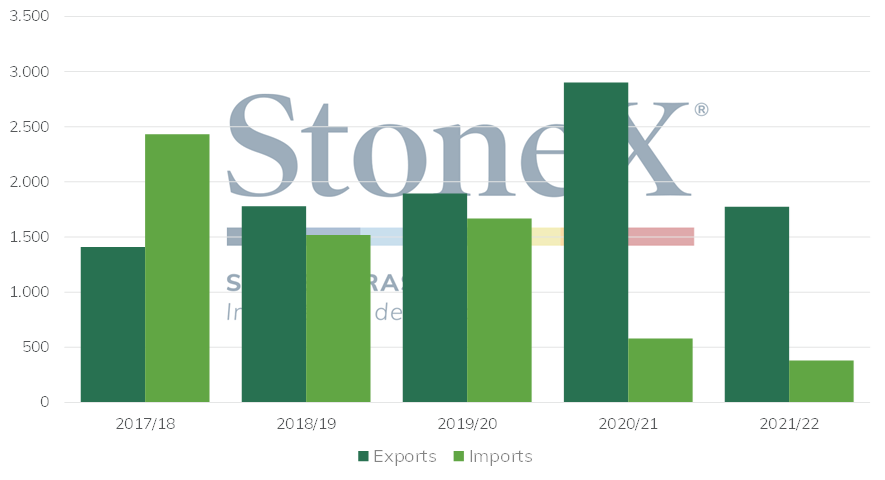

In relation to the ethanol market, Brazil exported about 1.77 billion liters in the 2021/22 crop, which corresponds to a 39% reduction in relation to the previous season. Like in sugar, the drop was influenced by limited production and restricted domestic supply in the season.

In addition to the low output that influenced the reduction in exports, lower international purchases also had an impact on domestic supply, since a high exchange rate caused imports from the US to drop by 46% in relation to the previous cycle, accumulating a volume of 229 million liters. Imports from Paraguay, the second largest, had a more subtle drop of only 2%, keeping a level of 150 million liters of ethanol.

Ethanol imports (million m³)

Source: ComexStat. Design: StoneX.

As shown in a recent analysis, the sugar-directed mix in the CS still carries a number of uncertainties for this 2022/23 crop and, consequently, can directly affect the prospects for sugar production and exports. Fuel prices are rising sharply and may encourage mills to produce ethanol from now on, a scenario supported mainly by the appreciation of crude oil on the international market since last year.

In terms of cane production, above-average rainfall over the last quarter in CS Brazil points to good average soil moisture conditions, a positive factor for this start of the cycle. This regularity of rains, also observed at the end of 2021, contributed to the development of sugarcane that will be harvested from mid-April. In StoneX’s last sugar and ethanol crop estimate, published in March 2022, average TRS was projected at 140.7 kg/t and the sugar-directed mix at 45.5%, which is 0.5 percentage points above the number estimated for the 2021/22 crop.

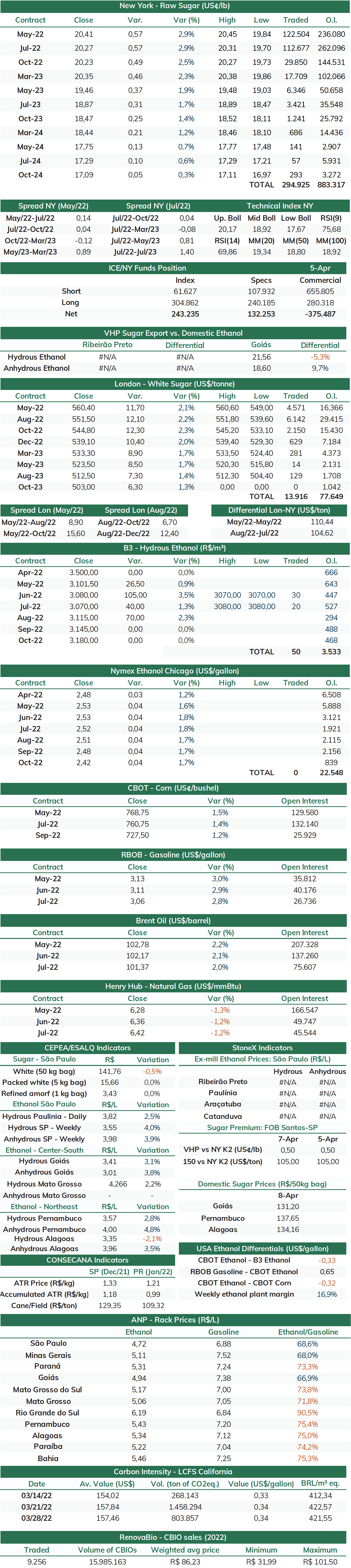

With these variables and average TCH of 73.4 tonnes/hectare, the report estimated that 34.5 million tonnes of sugar would be produced in the CS during the 2022/23 season, an annual increase of 7.5%. In this respect, the commodity’s prices on the international market and the expected rise of 7.6% in cane crushing favor sugar. In March, ICE/NY sugar fixations for 2022/23 export were well advanced at 76% of production, compared to 70% in the same period of the previous year.

In this sense, sugar exports until the end of the new crop can certainly benefit from greater productive perspective, mentioned earlier, and from sellers’ commitment to future supply of the product. However, it is important to point out that the Brazilian currency gained over 15% against the dollar in the first quarter of 2022, a fact that tends to make the nation’s goods more expensive in global trade, thus discouraging exports. Other points will be on the market’s radar, especially with regard to the lingering uncertainty of how much cane will actually be allocated to sugar and ethanol production.

In recent months, the dynamics of the fuel market may be important for potential revisions to the sugar mix. Crude oil remains at the highest levels since 2014, with Brent operating close to USD 100/barrel. The conflicts between Russia and Ukraine and productive deficits in other regions of the world have brought on major bullish factors to the industry, and these points should continue to be monitored from now on. However, Covid-19 is spreading again in China, which may slow down the recovery of fuel consumption in the country, and supply-side rearrangements are occurring in other markets, such as the release of oil from strategic reserves in the United States. These two factors have a bearish influence on the crude oil market.

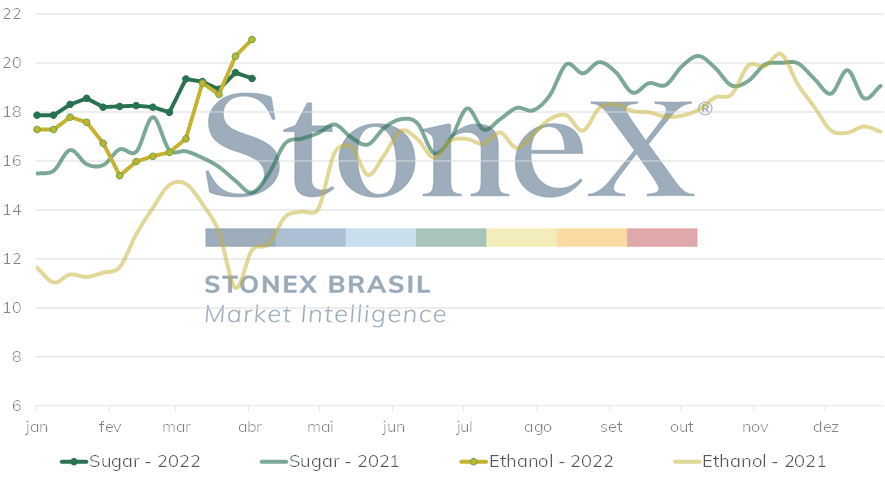

Since February, the sugar-energy sector has faced a significant increase in hydrous ethanol prices. When we observe the parity between sugar #11 in NY and hydrous based in Ribeirão Preto, from the last third of March, ethanol is favored against sugar. When we look at the trajectory, the accelerated upward trend in ethanol is clear, and this can cause the market to revise the productive mix at mills in the coming months, possibly with greater allocation of sugarcane to ethanol production. This, in turn, would lead to a decrease, even if marginally, of sugar production and, consequently, less availability for shipments in the 2022/23 cycle.