Rhona O'Connell, Head of Market Analysis, EMEA & Asia

Tel: +44 203 580 6115 / mobile +44 7384 833897

4 November 2025

StoneX Bullion round-up; COMEX silver inventories almost back to pre-tariff levels; Gold slides by 11% before steadying

- Gold is now taking some of the froth off the top of its recent exponential price rise . The recent intraday peak was $4,382, a gain of 32% since this strong rally started in late August and of 67% since the start of this year.

- The recent correction saw a move to $3,386 in seven days in what some members of the Press called a rout; this 11% fall was triggered largely on technical considerations as the market was very heavily overbought and once the move faltered, some profits were taken and then technical stops were hit, bringing in CTAs and momentum traders.

- From a fundamental standpoint, the fall coincided with Diwali, the day in the Hindu calendar that is regarded as the most auspicious for the gifting of gold.

- The Monsoon season had been a good one, with a good harvest, and after months in which gold (and silver) demand had been under a cloud, the Indian market rocketed in October. The onset of Diwali took this element out of the market as most of the buying had been done beforehand.

- At the LBMA annual Conference last week, where there were more than 900 delegates, the overwhelming feeling was that we did indeed need this break in the bull run, but that with the width and depth of geopolitical uncertainty still swirling around the markets this looked looks more like a correction than a breakdown.

- The general body of opinion is that there is very good solid support between 3,700 and 3,800, a view to which we also adhere in the investment session. It was suggested that one of the areas that has been supporting gold has been the loss in industrial productivity globally over the past few years and that the advent of AI may be able to reverse this, at least in part. If so, then this theory points towards an easing in gold prices after maybe a year or so when the situation is clearer.

- We are looking for a period of consolidation in the near term. In our view a major key to the 2026 outlook revolves around the Supreme court’s ruling over the Lisa Cook Case. If found in favour of the President this could be good for a fresh $500 on the gold price on the back of reduced Fed independence vs political influence. This would be a bullish factor in itself, but there could be further ramifications from a weaker dollar. If the Court finds in favour of Cook then the reverse would be the case.

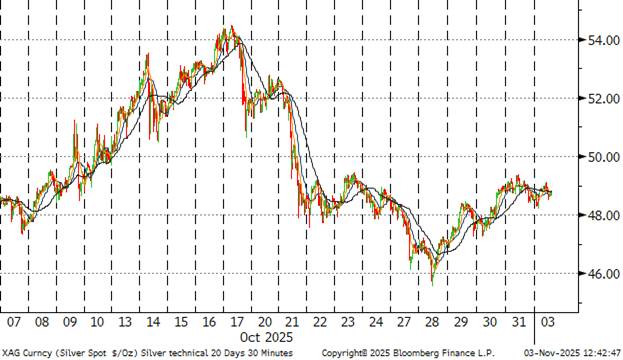

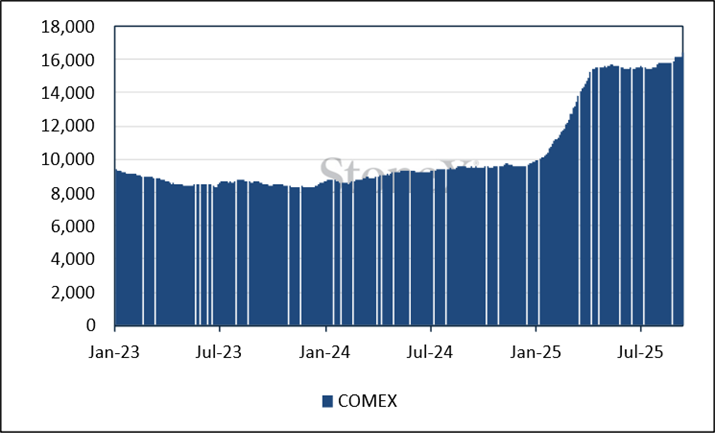

- Silver is also taking a much-needed breather and the dislocations in the market have been easing as metal has been coming across the Atlantic with houses reacting to the London- COMEX arbitrage. Inventories have dropped from 16,491t at end-September to 15,005t at end-October, a fall of 1,486t or 9% and taking them down to levels last seen two days after the tariff day. We won't have trade figures for a good while yet, but I got the impression from logistics companies last week that business has been active and material continues to be flown rather than shipped

- The onset of Diwali would also have helped ease conditions as buying was rampant in silver in October also. But we now have the wedding seasons ahead of us and this will also be supportive for both metals, with brides’ Shreedans (gold) and with wedding presents often in silver.

- We are not out of the woods yet, however. Although silver moved into a contango briefly in late October, it is now again in a small backwardation between spot and the COMEX active contract, and the India factor could be back in play here.

- LBMA vaulting numbers should be through next Monday and that will throw more light on the situation.

- The US Government remains in partial lockdown with the Republicans and Democrats at polar opposites on some issues, revolving in some part around medical health insurance. We therefore still haven't had any CFTC numbers since the 23rd September

- Outlook: Gold is also losing some froth, while still pricing in concerns over Fed independence and the possibility of stagflation as well as underlying geopolitical risk and international tensions. Some of the froth has been blown off in a much-needed correction. The Fed Beige Book is pointing to further slowdowns in the US and question marks persist over the state of the labour market.

- For the much longer term, silver has a robust fundamental outlook but for now, it is taking a much-needed break with metal coming eastwards across the Atlantic. The solar market remains oversupplied, but still has a constructive future, while AI and vehicle electrification will also help to keep the market in a pre-investment deficit.

Gold, year-to-date; giving back gains but still underpinned

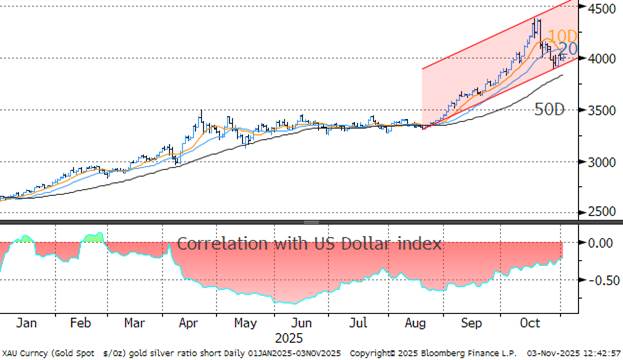

Silver; new records – but not in real terms. Taking a much-needed breather

Source: Bloomberg, StoneX

Silver easier in London- eased into contango briefly in late October; tighter again now

Source: Bloomberg

To recap: - Silver inventories on COMEX are divided into registered and eligible. “Eligible” inventories are inventories in a CME-approved warehouse, not necessarily delivered onto the Exchange itself; the owners of that metal may just be using the warehouse as a secured storage space. Eligible metals may belong to a range of different market participants. The CME does not have any direct control over these inventories.

When the holder of the metal delivers it onto the Exchange, then a warehouse receipt is issued and the inventories become “registered” and can then be used for delivery against futures contracts.

Since the 10th October combined registered and eligible silver inventories have declined by 1,525t.

The gold inventories have an additional sub-division, namely “pledged” warrants. These warrants are pledged to the Exchange as collateral, which gives CME a first priority security interest in the relevant warrants. When a clearing member initiates a pledge, the warrant status changes from “Registered” to “Pledged_PB_Pending”. When the transfer to CME is complete the status becomes “Pledged_PB”. The warrants remain registered with the Exchange. Currently 54% of COMEX inventories are registered.

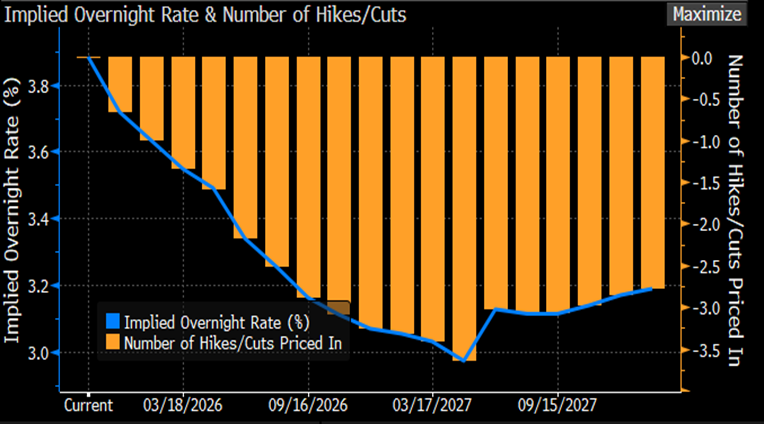

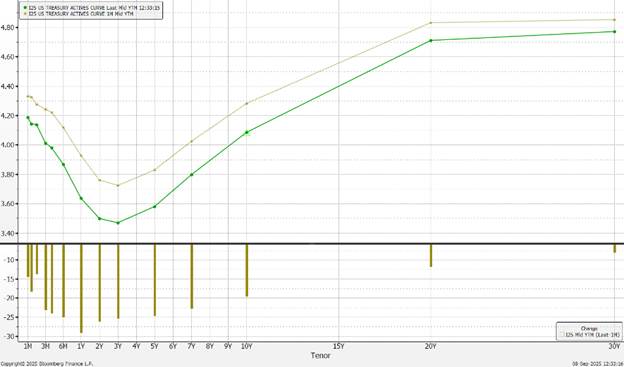

Meanwhile the US bond markets are pricing in a 66% chance of one more 25-point cut this year. The next FOMC meeting is scheduled for 9-10 December.

Source: Bloomberg

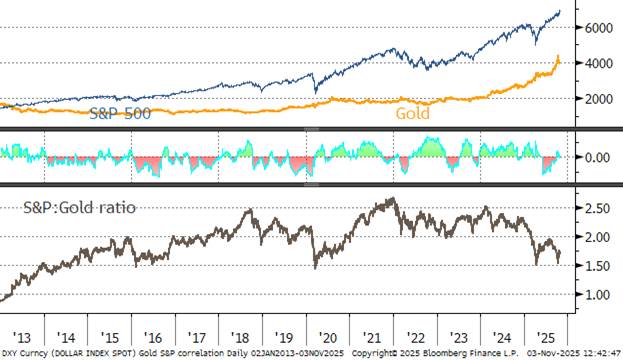

The S&P, gold and the dollar

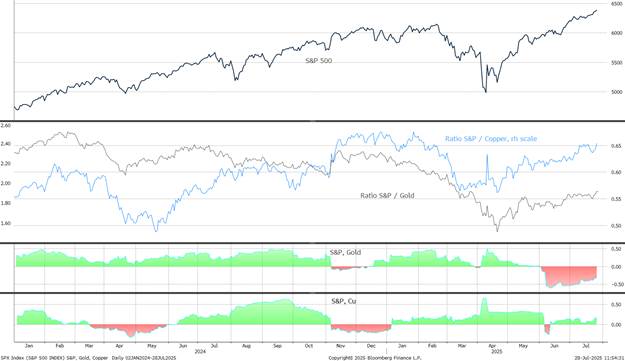

The S&P, gold and copper

Gold:dollar correlation; easing again; now down to -0.21

Source: Bloomberg, StoneX

US yield curve: still steepening as the short end prices in rate cuts while the longer tenors are rising on fears of a longer-term inflationary impact; overall levels continue to drift lower, however

Source: Bloomberg, StoneX

COMEX silver inventories, tonnes

Source CME via Bloomberg, StoneX

Silver ETFs have oscillated over the same period, with reasonably chunky movements in both direction for a net gain (basis the Bloomberg figures) of 75t to 25,606t.

Gold COMEX inventories are also easing after touching a recent peak of 1,249t on 6th October, to stand last at 1,216t. Holdings in ETFs stood at 3,924.8t (World Gold Council figures) for a year-to-date gain of 705.9t. North American holdings are up 24.4% or 402.9t; Europe holdings are up 11.9% or 153.3t; Asia has expanded by 56.9% to 142.6t and “other” up 11.1% to 7.1t.

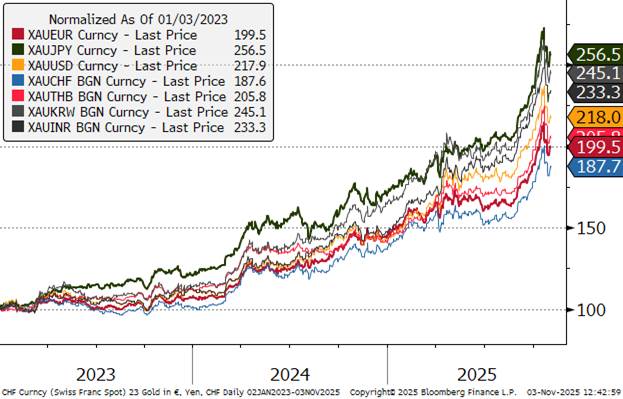

Gold in key local currencies.

Source: Bloomberg, StoneX

Gold:silver ratio, year to-date

Source: Bloomberg, StoneX

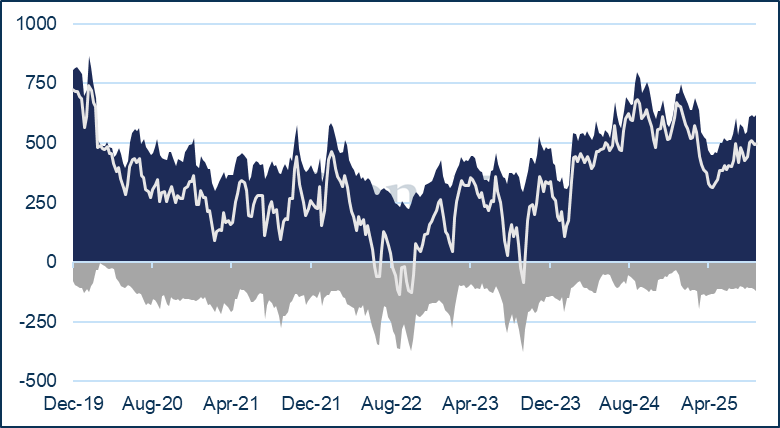

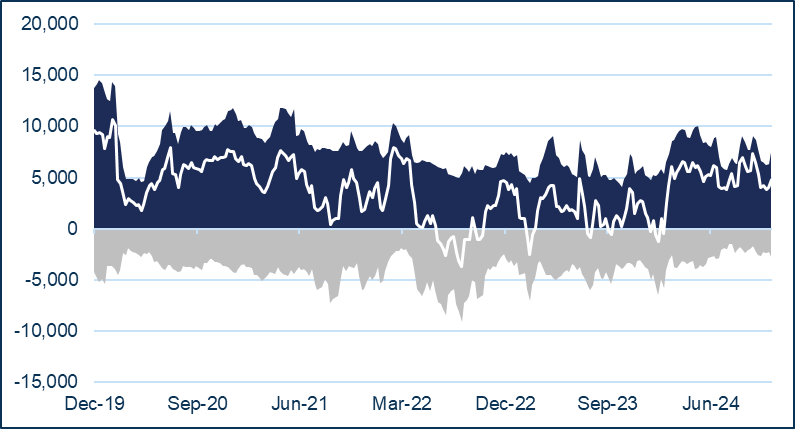

The CFTC numbers run only as far as 23rd September due to the shutdown

Gold COMEX positioning, Money Managers (t) –

COMEX Managed Money Silver Positioning (t)

Source for both charts: CFTC, StoneX

CFTC: - As of 23rd September, the net gold long position among COMEX Money Managers was broadly unchanged over the previous four weeks – in a range of 509t to 499t, which is the most recent figure. At 618t, the outright longs were only 17t higher than the 12-month average and so there is no real overhang there. At 119t, the outright shorts were 13% higher than their 12-month average of 105t.

The silver position is different, with outright longs of 8,235t just 3% higher than the 12-month average, while the outright shorts (2,197t) are 8% below the 12-month average.

| | 4 November 2025 | Previous week | % change | Year-to-date | Range Jan 2024 onwards | | Range as % |

| | | | | | Min | Max | |

| Gold (pm LBMA price) | 4,025.25 | 3,970.80 | 1.37% | 52.11% | 1,985.10 | 4,294.35 | 116.33% |

| Silver (LBMA price) | 48.78 | 47.37 | 2.98% | 65.84% | 22.09 | 54.10 | 144.96% |

| Platinum (pm LBMA price) | 1,580.00 | 1,602.00 | -1.37% | 71.55% | 963.00 | 1,686.00 | 75.08% |

| Palladium (pm LBMA price) | 1,463.00 | 1,402.00 | 4.35% | 58.85% | 852.00 | 1,575.00 | 84.86% |

| S&P 500 | 6,851.97 | 6,875.16 | -0.34% | 16.00% | 4,688.68 | 6,890.89 | 46.97% |

| $:€ | 1.1520 | 1.1645 | -1.07% | 10.68% | 1.0244 | 1.1867 | 15.84% |

This material should be construed as market commentary and represents the opinions and viewpoints of the author, and does not reflect tailored advice associated with any specific account.

The views are current only through the date stated and are subject to change at any time based upon market or other conditions, and StoneX Group Inc. (“SGI”) disclaims any responsibility to update such views. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. Past performance does not guarantee future results.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided.

References to certain OTC products or swaps are made on behalf of StoneX Markets, LLC (SXM), a member of the National Futures Association (NFA) and provisionally registered with the U.S. Commodity Futures Trading Commission (CFTC) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ and who have been accepted as customers of SXM.

StoneX Financial Inc. (SFI) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (SEC) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Advisor. StoneX Financial (Canada) Inc. (SFCI) is registered in Canada and is a member of CIRO and CIPF. References to certain securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to certain exchange-traded futures and options are made on behalf of the FCM Division of SFI. Wealth Management is offered through SA Stone Wealth Management Inc., member FINRA/SIPC, and SA Stone Investment Advisors Inc., an SEC-registered investment advisor, both wholly owned subsidiaries of SGI.

R.J. O’Brien & Associates, LLC (RJO) is registered with the CFTC as a Futures Commission Merchant and is a member of NFA.

StoneX Financial Ltd (SFL) is registered in England and Wales, company no. 5616586. SFL is authorized and regulated by the Financial Conduct Authority (FCA) (registration number FRN:446717) to provide services to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorized to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorized and regulated by the FCA under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorized by the FCA.

This communication is issued in the European Economic Area by StoneX Financial Europe GmbH (SFEG). StoneX is the trade name used by STONEX GROUP INC. and all its associated entities and subsidiaries. StoneX Financial Europe GmbH (“SFEG”) is a securities trading firm registered in Germany under Company No. HRB 80844.

StoneX Financial Pte Ltd (Co. Reg. No 201130598R) (“SFP”) is regulated by the Monetary Authority of Singapore and is a Capital Markets Service Licence holder (for dealing in capital market products), an Exempt Financial Adviser (for advising on investment products and issuing or promulgating analyses/ reports on investment products) and a Major Payment Institution (for domestic and cross-border money transfer services).

SFP may distribute analysis/report produced by its respective foreign affiliates within the StoneX Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations Recipients should contact SFP at (65) 6309 1000 for any matters arising from, or in connection with, this webinar.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism.

StoneX Financial (HK) Limited (CE No.: BCQ152) (“SHK”) is regulated by the Hong Kong Securities and Futures Commission for Dealing in Securities and Dealing in Futures Contracts.

StoneX Financial Pty Ltd (ACN 141 774 727) holds an Australian Financial Service License (AFSL: 345646) for Dealing in Securities, Exchange-Traded Derivatives Contracts, OTC Derivatives Contracts and Foreign Exchange Contracts, and is regulated by the Australian Securities and Investments Commission.

StoneX Securities Co., Ltd. (“SSJ”) (Co. Reg. No 010401047199) is regulated by the Japanese Financial Services Agency as a Type-I Financial Instruments Business Operator (Kanto Local Finance Bureau (FIBO)No.291’), is a member of the Financial Futures Association of Japan for dealing and broking FX and FX Option transactions, and is a member of the Japan Securities Dealers Association for dealing and broking stock indices and option transactions.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

The report/analysis herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

© 2026 StoneX Group Inc. All Rights Reserved.