The Australian dollar enters Q3 with the market's focus shifting away from geopolitics and back towards monetary policy and economic data. The Middle East conflict failed to become the sustained macro driver many feared, oil prices have retreated, and traders are once again weighing the relative outlook for the RBA and Fed.

That shift comes at an awkward time for the Aussie. After a strong multi-quarter rally, speculative positioning has turned bearish and the US dollar has regained momentum as traders increasingly favour the Fed over the RBA. While seasonality suggests higher volatility through Q3, it provides little support for a sustained recovery in the Australian dollar.

View related analysis:

AUD/USD Fundamental Outlook: RBA, Fed and Economic Data

Australian Economy Showing Early Signs of Slowing

Data have begun to turn against RBA hawks. While inflation remains too high for the RBA's comfort, signs of weakness have emerged in consumer confidence and business sentiment, while employment and household spending have hit a bump in the road.

May's data briefly fuelled bearish expectations for AUD/USD, with household spending contracting, unemployment rising to a four-year high and employment disappointing. However, June's figures largely reversed those concerns as spending rebounded, unemployment edged lower and employment recovered. While unemployment continues to trend higher overall, the latest data do not suggest the economy is on its knees.

Inflation remains the fly in the ointment, with trimmed mean CPI rising to 3.6% year-on-year, even as headline inflation eased to 4.0%. Both measures remain well above the RBA's 2–3% target range and, unless inflation retreats more quickly, the RBA is likely to retain a hawkish bias—even if it ultimately refrains from delivering another rate hike.

Takeaway: The Australian economy is showing early signs of slowing, but inflation remains sticky enough for the RBA to retain its hawkish bias.

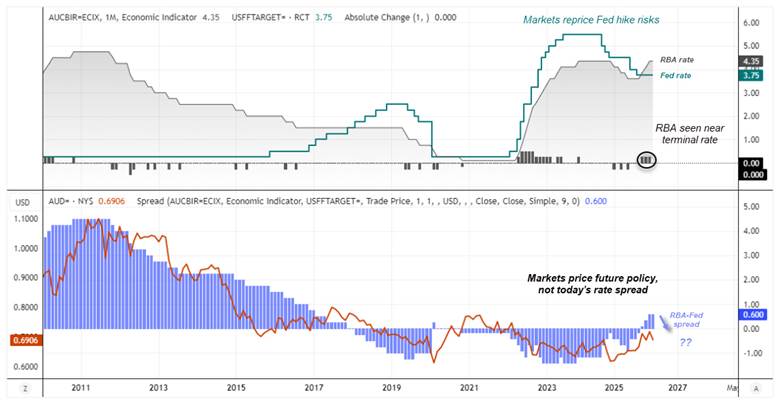

RBA Outlook: Is the Hiking Cycle Over?

The RBA left the cash rate unchanged at 4.35% in June after delivering three consecutive hikes totalling 75bp. While policymakers retained a mildly hawkish tone, it marked a step back from the stronger rhetoric accompanying the previous hikes.

RBA cash rate futures imply a peak cash rate of 4.50% by December, just 15bp above the current rate. Three of the Big Four banks also expect the RBA to remain on hold before eventually easing, leaving Westpac as the only major bank forecasting further hikes.

With crude oil prices now down 37.5% from their post-war peak and around 20% above pre-war levels, inflation pressures remain elevated but are far less acute than when the RBA was signalling an urgent need for further tightening. I therefore see another rate hike as an outlier scenario and expect the RBA to remain on hold throughout Q3, leaving AUD/USD increasingly exposed if the Fed resumes tightening.

Source: LSEG, Reserve Bank of Australia, Federal Reserve.

Takeaway: Markets increasingly expect the RBA to remain on hold, leaving AUD/USD more exposed if the Fed tightens again.

Fed Outlook: Markets Price the Risk of Another Hike

Kevin Warsh has taken over from Jerome Powell as Fed Chair, and markets increasingly believe the Fed's next move could be another rate hike. Fed funds futures imply just under a 50% chance of a hike as early as September, while the probability of a December hike has climbed to around 40%.

The final estimate of Q1 GDP was revised up to an annualised 2.1%, while core PCE inflation remains well above target at 3.4% year-on-year. Retail sales continue to outperform and business surveys remain expansionary, with elevated 'prices paid' components suggesting inflationary pressures persist.

Ultimately, persistent inflation, resilient labour market data and hawkish comments from FOMC members have prompted traders to rebuild expectations of another Fed hike this year.

The primary risk to this outlook is a meaningful deterioration in US economic data. That would likely remove expectations of further Fed tightening, weaken the US dollar and stabilise the AU–US yield differential, allowing AUD/USD to outperform its otherwise mixed seasonal tendencies.

Takeaway: Markets are increasingly pricing another Fed hike, leaving the US dollar well supported unless incoming data materially weaken.

AUD/USD Technical Outlook: Charts, Positioning and Seasonality

AUD/USD Chart Signals Turn More Cautious

AUD/USD ended Q1 having posted five consecutive quarterly gains—its longest winning streak in nine years. Whether Q2 records a sixth consecutive advance or not, the rally already appears stretched in both time and price terms. Q2 is also on track to close with a shooting star reversal candle.

- AUD/USD has already corrected 5.4% from its May high and is now testing the March low alongside its 200-day SMA and EMA around 0.6900. While the macro backdrop has become less supportive, these may not be ideal levels to initiate fresh short positions.

- AUD/USD's correlation with the Chinese yuan has weakened markedly. The six-month correlation has fallen to 0.70 and the three-month correlation to 0.28, suggesting US dollar dynamics are becoming a bigger driver than China alone.

- Options markets remain relatively sanguine. Three-month implied volatility points to a trading range of roughly 0.6614–0.7170, while risk reversals remain far less bearish than futures positioning suggests.

The US dollar also warrants consideration. While it remains in a solid uptrend, I continue to believe the major cycle topped in 2022, followed by a lower high in January 2025. If correct, the current rally is likely the final leg of a corrective advance rather than the start of a new structural bull market. Attention should therefore shift towards identifying a Q3 or Q4 peak in the US dollar, which would likely coincide with a durable low in AUD/USD.

Source: ICE, TradingView

Takeaway: The technical backdrop has become less supportive for AUD/USD, but much of the bearish macro narrative may already be reflected in price. A durable low is more likely to emerge alongside a peak in the US dollar later in Q3 or Q4.

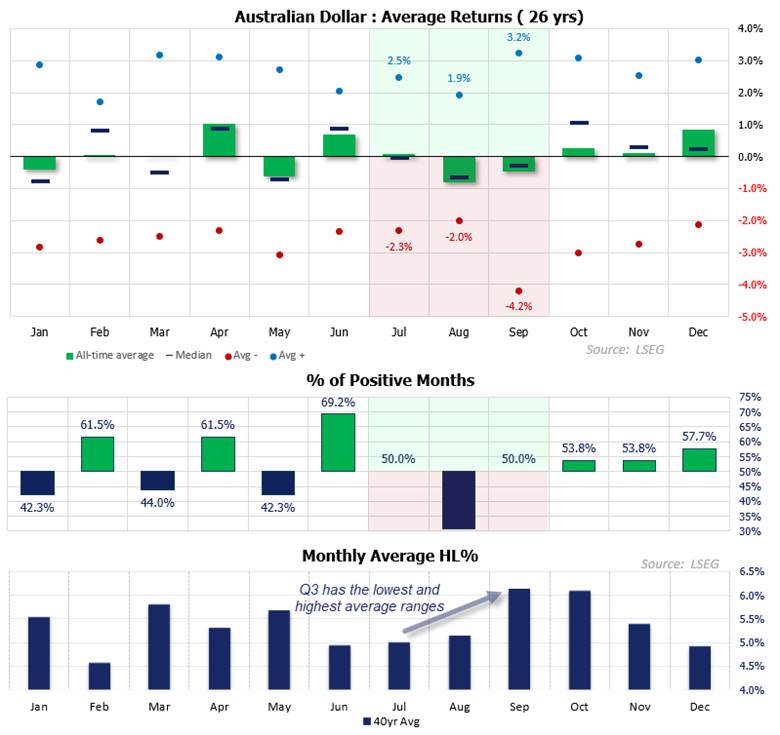

Seasonality Points to a Volatile and Directionless Q3

The third quarter presents a mixed seasonal backdrop for AUD/USD. Historical data show volatility rising through the quarter, while returns become less supportive after June. July has typically been directionless, while August and September have produced modest average declines alongside larger price swings.

- Using data since 2000, July's average return is broadly flat, while August and September have recorded average declines of around 0.7% and 0.3%, respectively.

- Median returns are broadly flat in July and August before improving slightly in September, suggesting the weaker average returns were driven by a handful of larger declines.

- June has the highest win rate of the year (69.2%), but that falls to 50% in both July and August before improving modestly to 53.8% in September and October.

- September and October record the highest average trading ranges of the year, highlighting the tendency for volatility to increase into the latter part of Q3.

Source: LSEG

Takeaway: Seasonality no longer provides the tailwind seen in June. Instead, Q3 tends to bring higher volatility alongside broadly neutral-to-soft returns, increasing the likelihood of larger swings without a sustained directional trend.

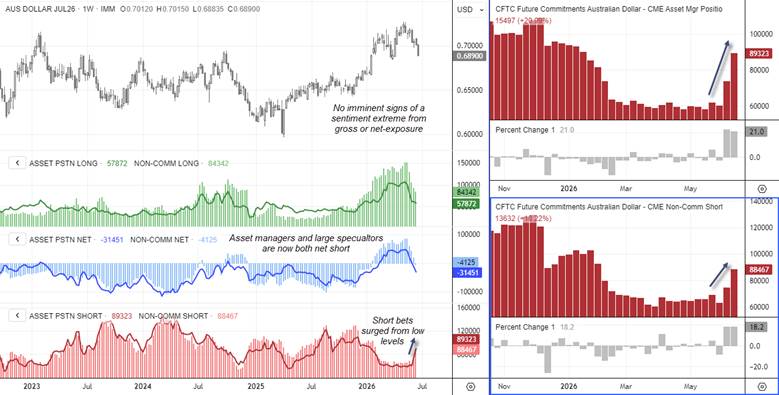

AUD/USD Futures Positioning Turns Bearish

While seasonality tends to favour the Aussie early in Q3, futures positioning does not. Large speculators and asset managers have recently flipped to net-short exposure after holding record net-long positions just weeks ago, with short positions now rising sharply.

With neither gross nor net exposure signalling a sentiment extreme, there is little to suggest bearish positioning has become overcrowded. That leaves scope for further downside if incoming data continue to favour the US dollar.

Source: CME, CFTC (COT), LSEG

For traders wanting a deeper understanding of futures positioning, I’ve also published a guide on how to read and interpret weekly COT data in forex markets.

AUD/USD Forecast: Q3 Outlook

Overall, the balance of risks points to a more challenging quarter for AUD/USD. Expectations for further Fed tightening contrast with a more patient RBA, leaving the Australian dollar vulnerable if US data continue to outperform. However, much of that deterioration has already been reflected in price following the recent 5% correction, suggesting downside may become increasingly difficult as Q3 progresses. With seasonality also pointing to higher volatility rather than a clear directional edge, I continue to favour a volatile trading range through the quarter before a more durable low emerges later in the year alongside a peak in the US dollar.