- The historically-reliable 4-year halving cycle suggests that Bitcoin’s current bear market may stretch through Q3 before forming a durable bottom.

- The outlook for Bitcoin in Q3 remains biased to the downside, but the outlook for Q4 is starting to look more constructive amidst subdued valuation and continued resilience on the part of long-term holders.

- Long-term holders are once again advised to exercise patience until the price action confirms a shift to more bullish price action in the run-up to the 2028 halving.

Bitcoin H1 2026 in Review

In our last Bitcoin outlook, we concluded that “Bitcoin remains in a downtrend off the October 2025 high” and that “For now, there’s no evidence that the current downtrend is ending yet.” Despite some fits and starts, including a bounce above $80K by mid-May, that forecast has proven correct. The key question for crypto traders now is when (and perhaps more importantly where) the downtrend will run its course.

Below, we update our quarterly outlook for the king of cryptocurrencies and highlight relevant fundamental and technical trends that will drive Bitcoin in the coming months.

Bitcoin Q2 2026 Outlook

Starting from a top-down perspective, analysts have identified a reliable 4-year cycle centered around the Bitcoin Halving that has relatively reliably helped traders identify significant tops and bottoms over the years, though that’s no guarantee it will necessarily continue to do so moving forward.

For the uninitiated, the Bitcoin Halving is when the reward for mining new bitcoins is cut in half. This reduces the rate at which new Bitcoins are created and thus lowers the total supply of new Bitcoin coming into the market. The halving tends to increase scarcity and can make Bitcoin a more compelling investment for some traders. As any Bitcoin bull will tell you, the most recent halving in April 2024 took the “inflation rate” of Bitcoin’s supply to below 1% per year, less than half of gold’s annual inflation rate.

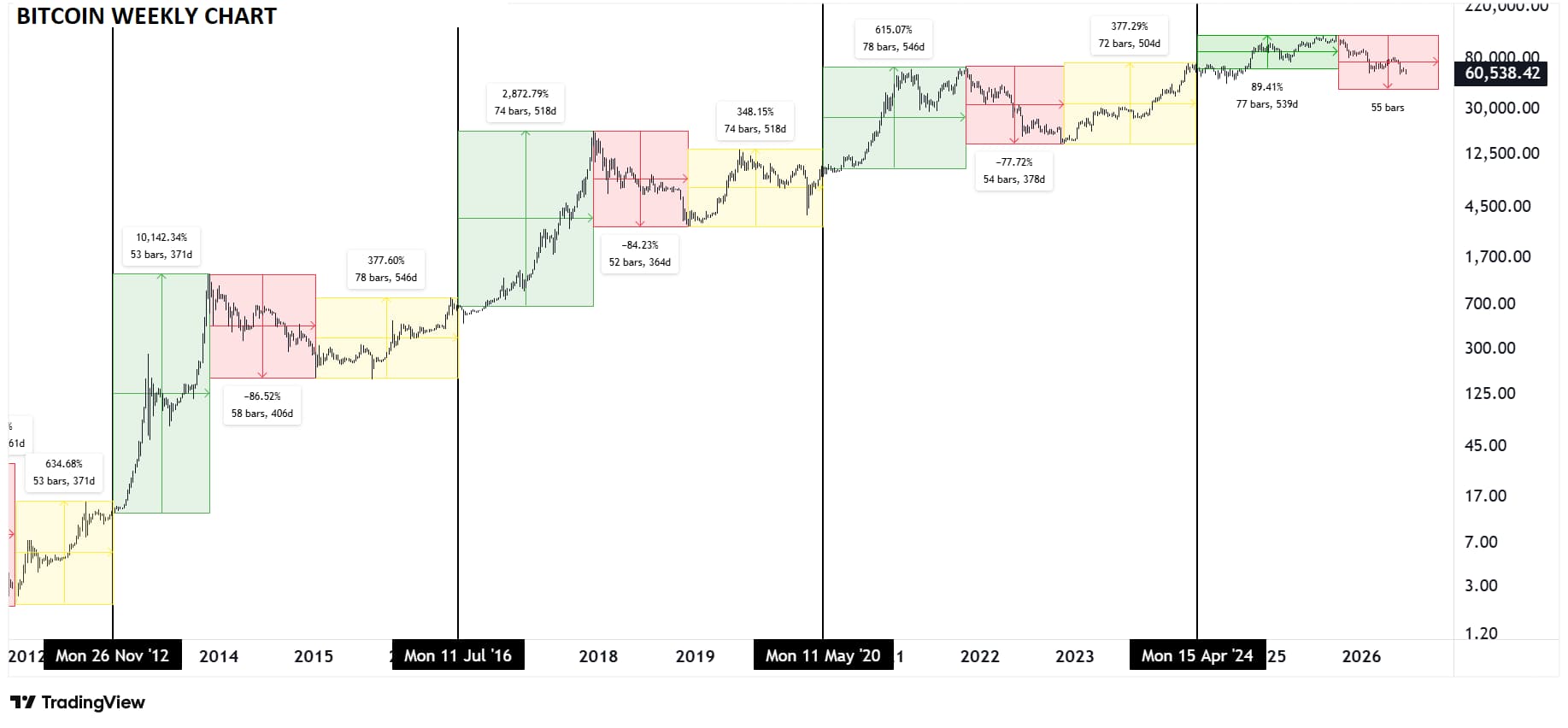

Looking at my favorite chart, which I colloquially call “The Only Bitcoin Chart You'll Ever Need™”, previous Bitcoin halvings have marked the transition from the (yellow) post-bottom recovery rally stage to the (green) full-blown bull market stage, followed by a (red) bear market stage as sentiment resets.

Projecting a similar time-based cycle forward from the last halving suggests that we reached the peak of the last cycle at the start of Q4 2025, and that a durable bottom may not be found until closer to the start of Q4 2026:

Source: TradingView, StoneX. Past performance is no guarantee of future returns.

Beyond the 4-year cycle, the fundamental and technical outlook for Bitcoin is relatively mixed, as we discuss in more detail below.

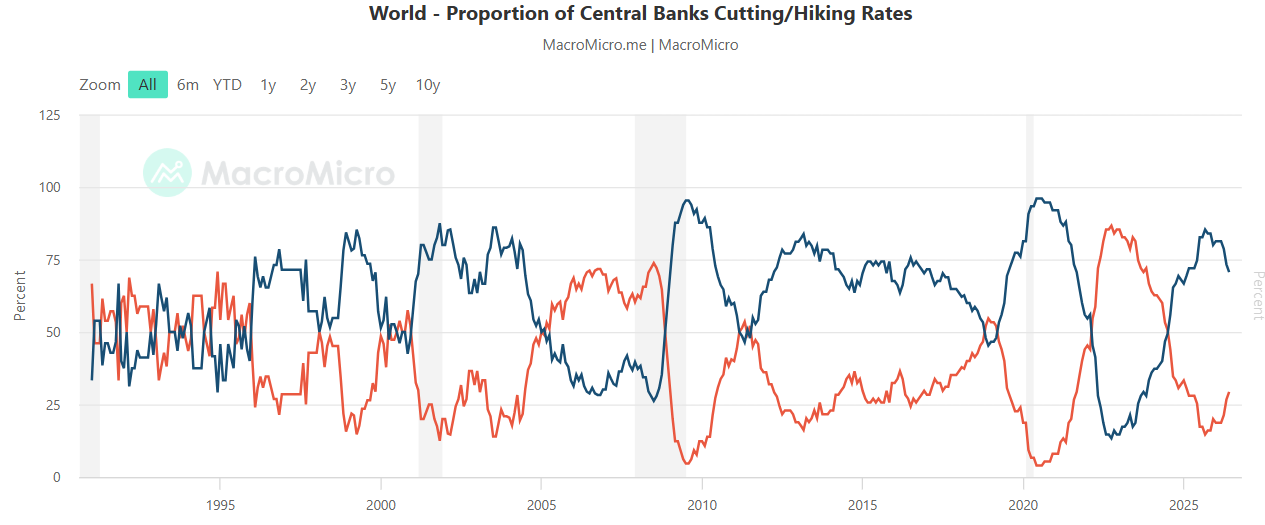

From a macroeconomic perspective, the monetary policy backdrop appears to be shifting, with more and more central banks tipping toward interest rate increases as they navigate the continued fallout from geopolitical shocks. As the chart below shows, most global central banks have still cut interest rates more recently, but with major central banks like the ECB, BOJ, and Federal Reserve all trending toward (additional) rate increases, the rest of the world may soon be forced to follow:

Source: MacroMicro

Looking ahead, the ongoing shift to a focus on the risks of re-accelerating inflation may develop into a potential headwind for Bitcoin as we move through H2, especially amidst generally accommodative fiscal policy across the globe.

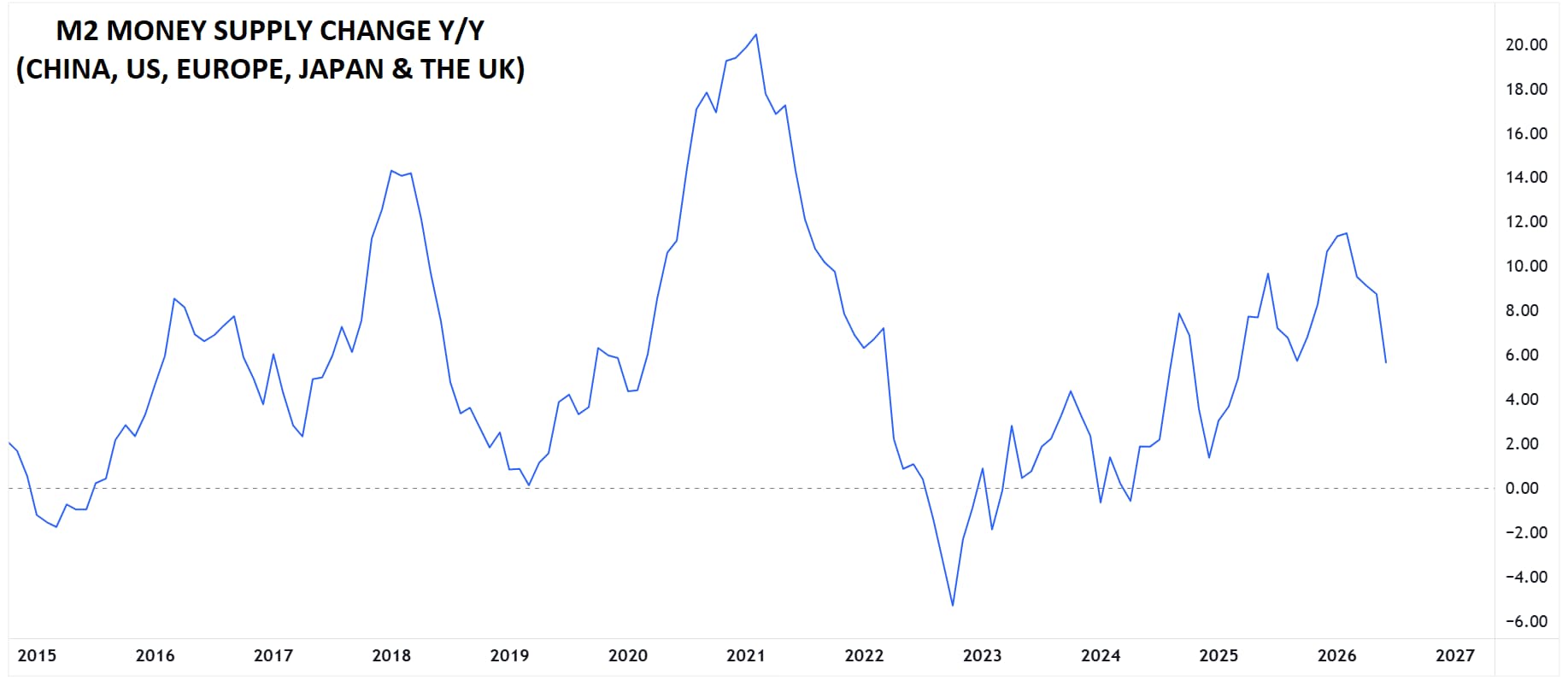

Meanwhile, the growth rate of fiat money in the financial system has slowed in recent months. So-called “M2” is central banks’ estimate of the total money supply, including all the cash people have on hand, plus all the money deposited in checking accounts, savings accounts, and other short-term saving vehicles such as certificates of deposit (CDs). While it is still growing, the year-over-year growth in M2 has dropped toward 6% from prior highs near 12% earlier this year:

Source: TradingView, StoneX.

One of the key narratives driving Bitcoin’s value is the idea of “hard money” or a hedge against fiat currency debasement, and as long as the global supply of money continues to increase, that theme could help support the cryptocurrency’s price.

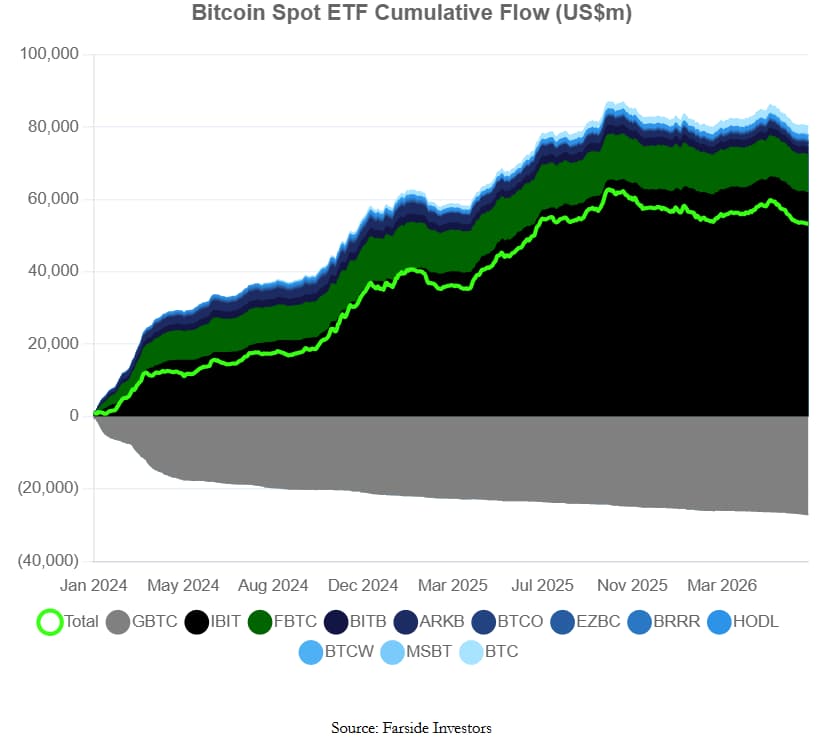

Beyond broad macroeconomic dynamics, a key theme supporting Bitcoin in recent years has been accumulation by large financial institutions and mom-and-pop investors. In addition to the growing popularity of firms accumulating the cryptocurrency as a treasury asset, we’ve also seen impressive inflows from “TradFi” institutional investors buying spot Bitcoin ETFs, with total inflows into Bitcoin ETFs near $53B, though those inflows have essentially stalled since mid-2025:

Source: Farside Investors

Broadly speaking, a revival in Bitcoin ETF purchases should support the cryptocurrency, whereas a shift toward concerted selling could weigh on it.

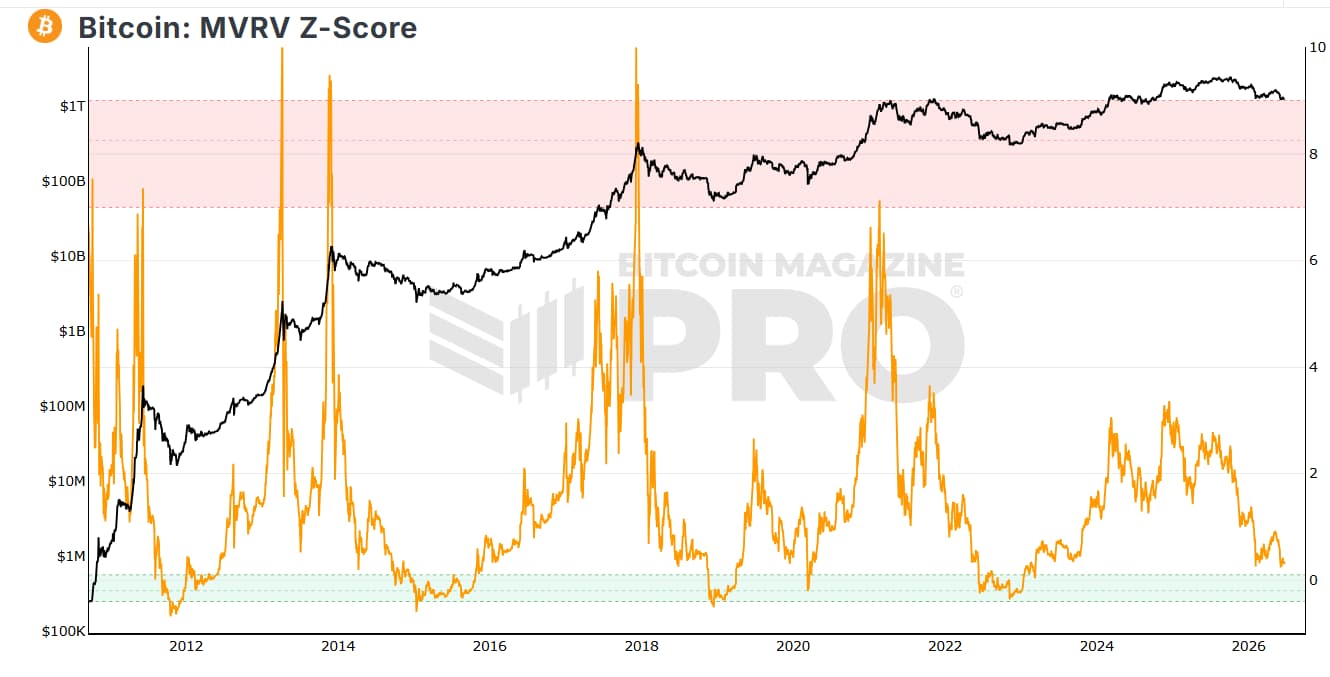

From a valuation perspective, the MVRV (Market Value to Realized Value) Z-score, which compares the current price to the price where each Bitcoin was last traded, has fallen to just 0.3, closer to the typical bear market bottom zone at 0.0 than the recent peak above 3.0:

Source: Bitcoin Magazine. Past performance is not indicative of future returns.

In a sign that Bitcoin is maturing as an investment and arguably, a new asset class, this valuation metric has become less volatile over time; for instance, the most recent peak never crossed 4, far from previous cycle peaks in the 7-10 range. Accordingly, it may not fall as far below 0 as the past bottoms in the -0.3 to -0.6 region would suggest. Time will tell whether this indicator remains a reliable measure moving forward.

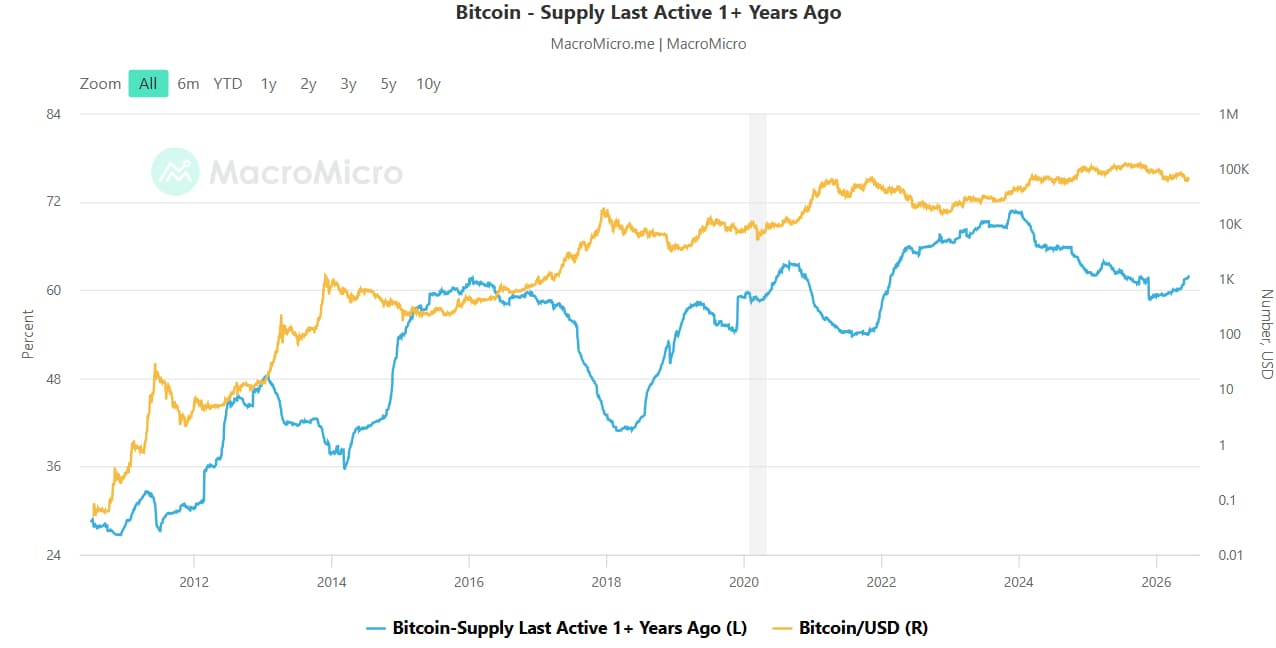

A final consideration is the behavior of long-term holders. As we’ve noted in previous outlooks, those who have held their Bitcoin for more than a year, almost tautologically, are not trying to make a “quick buck” off the cryptocurrency; rather they are more likely to be “true believers” or “HODLers” who are unlikely to sell unless they’re sitting on a truly massive gain.

As the chart below shows, the proportion of Bitcoin that has been held for at least a year has fallen from record highs above 70% to below 59%, but now appears to be trending back higher as long-term holders weather the worst of the bear market. This measure, by definition, moves relatively slowly, but any renewed selling from longer-term “HODLers” may offset inflows into ETFs as we move through H2:

Source: MacroMicro.me

Taking these diverse forms of analysis in totality, the outlook for Bitcoin in the third quarter remains biased to the downside: Money supply growth and ETF purchases have moderated, monetary policy is shifting in favor of the hawks, and the 4-year cycle suggests more near-term to pain to come. That said, the outlook for the fourth quarter is starting to look more constructive amidst subdued valuation and continued resilience on the part of long-term holders, just as the 4-year cycle nears a potential trough.

Of course, the catalysts we highlight in this report may not play out as expected – and to some extent, they may already be priced in, so readers should always exercise caution when trading Bitcoin and other cryptoassets. As ever, it will be critical to monitor a broad swath of macroeconomic and crypto-specific metrics as the year develops.

Bitcoin Technical Analysis – BTC/USD Weekly Chart

Source: TradingView, StoneX

Looking at the longer-term chart, Bitcoin remains in a downtrend off the October 2025 high. Since then, the cryptocurrency has formed a pattern of consistent lower lows and lower highs, with occasional periods of sideways price action and short-term bounces along the way.

As we noted three months ago, there’s still no evidence that the current downtrend is ending yet, with the next support zone starting in the mid-$50K range if the year-to-date lows near $60K are broken. This would represent a roughly -60% drawdown from the peak, aligning with the progressively smaller bear markets as the asset class has matured across cycles (-93%, -86%, -84%, -78% in 2011, 2014, 2018, and 2022 respectively).

Meanwhile, for bulls to grow more constructive that the longer-term trend may be shifting, Bitcoin would have to break above previous-support-turned-resistance in the $66K zone, followed by the May high near $83K. Long-term holders are once again advised to exercise patience until the price action confirms a shift to more bullish price action in the run-up to the 2028 halving.

-- Written by Matt Weller, Global Head of Research

Follow Matt on Twitter: @MWellerFX