Gold 2026 Outlook: What’s in store for XAU/USD in Q2?

Gold has been on a rollercoaster ride in recent quarters - how will the precious metal fare in Q2? Read our full outlook!

Fawad Razaqzada

- Global Macro

By: Julian Pineda, Market Analyst

As 2026 continues to unfold, currencies across North America are beginning to show notable shifts compared to the price action seen earlier in the year. Heading into Q2 2026, both USD/CAD and USD/MXN face a landscape shaped by changes in monetary policy, uncertainty around economic growth, and rising geopolitical tensions in the Middle East. In this context, both the Canadian dollar and the Mexican peso have started to lose ground against a strengthening U.S. dollar, and this trend could gain further traction if confidence in the greenback holds in the coming months. If this dynamic persists, both USD/CAD and USD/MXN could continue to face buying pressure over the medium term.

What path will central banks follow?

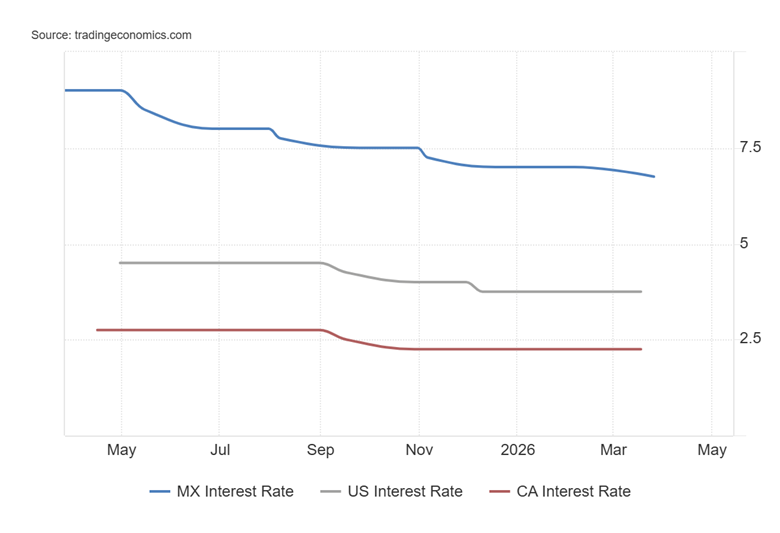

At the time of writing, North American central banks are beginning to show some divergence in their monetary policy outlook, as they have moved away from a path of lower interest rates toward a more stable, hold-driven stance. Bank of Mexico stands out, maintaining the highest rate in the region at 6.75% and largely keeping policy unchanged since December 2025, when rates were reduced from 7.25%. As a result, a central bank that was once more flexible has now aligned with its peers, adopting a more conservative stance in recent months.

Bank of Canada has now spent five months under a similar approach, stepping away from the rate cuts seen in late-2025. Since October of that year, the policy rate has remained at 2.25%, placing it in a relatively stable environment where, for now, no significant changes are expected to alter the current policy outlook.

Federal Reserve has also surprised markets by signaling a pause in rate cuts, after lowering rates to 3.75% from 4.00% in its December 2025 decision. While a new easing cycle had been expected following a period of stability throughout much of 2025, the current outlook points more toward a hold scenario, reflecting a more cautious stance from the central bank. In this context, the Fed appears to be aligning with its regional peers, reinforcing a more prudent approach to monetary policy.

North America Interest Rate Table 2025–2026

Colors: From green to red. Green indicates higher interest rates, while red represents lower rates in each country.

Source: Data - Tradingeconomics

North America Interest Rate Chart 2025–2026

Source: Tradingeconomics

The key question is what path North American central banks will follow for the remainder of 2026, as this factor could prove decisive for the performance of their currencies in the coming trading months:

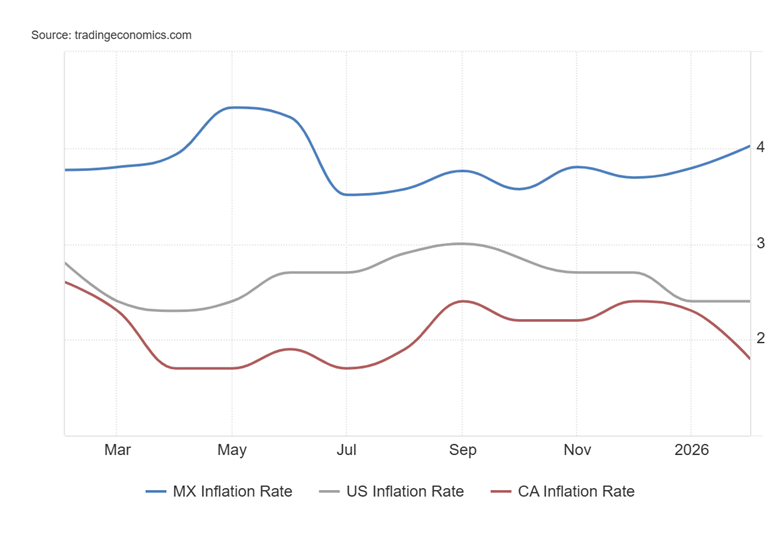

It is important to note that inflationary pressures have once again become a key focus for central banks, making it essential to assess how recent inflation data may influence or confirm the outlook for their upcoming policy decisions.

In Canada, inflation declined to 1.8% in February from 2.3% in January, slightly below the 2.00% target. In Mexico, a recent uptick stands out, with inflation rising to 4.02% in February, above 3.79% in January and the 3.00% target. In United States, inflation has remained stable at 2.4% year-over-year for January and February 2026, slightly above the 2.00% target.

North America Inflation Trend 2025–2026

Source: Tradingeconomics

Inflation data is showing a mixed pattern, with Mexico and the United States drifting away from their targets, while Canada maintains a more controlled rate within the region. In the case of Federal Reserve and Bank of Mexico, this could limit further rate cuts, as both have emphasized the need to keep inflation under control. Although there may be more room for Bank of Canada to adjust policy, it is still maintaining a cautious stance due to ongoing external risks that could generate additional inflationary pressures in the coming months.

This environment suggests that monetary policy across the three central banks is likely to remain largely in a hold or stable stance over the coming months. Federal Reserve stands out, as only weeks ago markets expected rate cuts to begin in June 2026, but expectations have now shifted toward 2027, reflecting a more restrictive stance relative to its peers and reducing the likelihood of lower rates in the near term.

Overall, shifts in central bank policy could reshape the strength of North American currencies. Mexico continues to hold the highest interest rate in the region, which helps support the peso’s appeal in a relatively lower-rate global environment; if rates remain near 7.00%, demand for the peso could hold up against its peers, given the relative attractiveness of peso-denominated investments. However, it is important to note that risk perception in Mexico remains elevated, which could limit a sustained recovery.

In Canada, inflation concerns are supporting a more stable policy stance, but its rate remains the lowest in the region, reducing the relative appeal of Canadian dollar–denominated assets compared to alternatives such as the Mexican peso or the U.S. dollar. In contrast, the more cautious stance of the Federal Reserve continues to support the strength of U.S. dollar–denominated assets, as both the bond market and the dollar itself remain global safe-haven benchmarks. Additionally, stable rates and a more aggressive stance relative to its peers help reinforce the dollar’s attractiveness over time.

This scenario suggests that, unlike Mexico and Canada, the U.S. dollar could continue to show a meaningful recovery, as seen at the start of 2026. Over time, this could translate into sustained buying pressure or a stable environment in both USD/MXN and USD/CAD over the medium term.

The big surprise: Middle East conflict

The conflict escalated further, impacting activity in the Strait of Hormuz between March 9 and 12, reaching peak tension with a nearly 90% drop in traffic. Market reaction was immediate: a surge in risk perception, increased demand for safe-haven assets, and a rise in energy prices, with WTI crude approaching the $120 level.

At the time of writing, the situation remains an active conflict with no clear short-term resolution, keeping risk sentiment elevated across major financial markets.

In this context, the U.S. dollar has gained relevance, as since the start of the Middle East conflict it has increasingly been perceived as a temporary safe-haven currency, offering stability and liquidity. In fact, the DXY index, which measures the dollar’s strength against other currencies, moved above the 97 level at the onset of the conflict, later surpassed 99 as disruptions in the Strait of Hormuz intensified, and eventually broke above the 100 psychological level amid continued escalation. This highlights that the dollar has been one of the currencies attracting the strongest demand as the conflict has persisted.

Source: Data TVC - Tradingview

The conflict has begun to generate additional inflationary pressures through rising energy prices, increasing production costs at a global level. This environment has led central banks to adopt a more cautious stance, while the U.S. dollar has regained prominence as a safe-haven currency, gaining ground against currencies such as the Canadian dollar and the Mexican peso.

In this context, if no clear short-term resolution emerges, demand for the U.S. dollar is likely to remain firm, potentially translating into sustained buying pressure in USD/MXN and USD/CAD over the coming months.

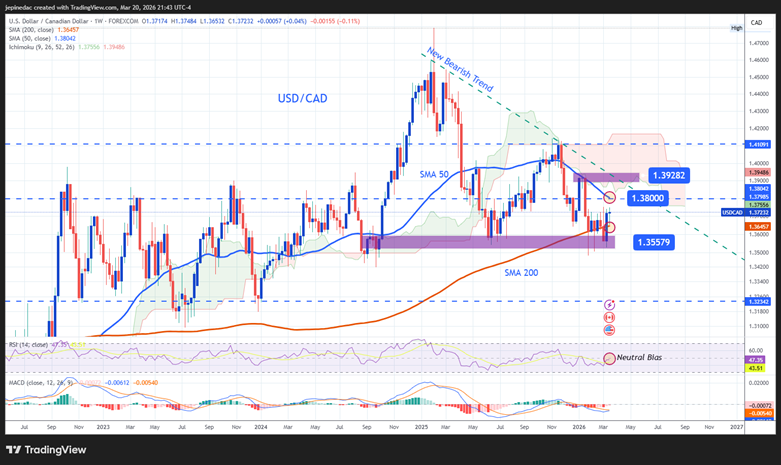

USD/CAD attempts to hold its downtrend

Source: StoneX, Tradingview

Indicators:

Key Levels:

USD/MXN begins to show a relevant bullish bias

Source: StoneX, Tradingview

Written by Julian Pineda, CFA, CMT – Market Analyst

Follow him on: @julianpineda25

This material should be construed as market commentary and represents the opinions and viewpoints of the author, and does not reflect tailored advice associated with any specific account.

The views are current only through the date stated and are subject to change at any time based upon market or other conditions, and StoneX Group Inc. (“SGI”) disclaims any responsibility to update such views. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. Past performance does not guarantee future results.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided.

References to certain OTC products or swaps are made on behalf of StoneX Markets, LLC (SXM), a member of the National Futures Association (NFA) and provisionally registered with the U.S. Commodity Futures Trading Commission (CFTC) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ and who have been accepted as customers of SXM.

StoneX Financial Inc. (SFI) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (SEC) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Advisor. StoneX Financial (Canada) Inc. (SFCI) is registered in Canada and is a member of CIRO and CIPF. References to certain securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to certain exchange-traded futures and options are made on behalf of the FCM Division of SFI. Wealth Management is offered through SA Stone Wealth Management Inc., member FINRA/SIPC, and SA Stone Investment Advisors Inc., an SEC-registered investment advisor, both wholly owned subsidiaries of SGI.

R.J. O’Brien & Associates, LLC (RJO) is registered with the CFTC as a Futures Commission Merchant and is a member of NFA.

StoneX Financial Ltd (SFL) is registered in England and Wales, company no. 5616586. SFL is authorized and regulated by the Financial Conduct Authority (FCA) (registration number FRN:446717) to provide services to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorized to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorized and regulated by the FCA under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorized by the FCA.

This communication is issued in the European Economic Area by StoneX Financial Europe GmbH (SFEG). StoneX is the trade name used by STONEX GROUP INC. and all its associated entities and subsidiaries. StoneX Financial Europe GmbH (“SFEG”) is a securities trading firm registered in Germany under Company No. HRB 80844.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism. SAP is an “Approved International Trading Company” authorized to act as a “Spot Commodity Broker” under the Commodity Trading Act.

StoneX Financial Pte Ltd (Co. Reg. No 201130598R) (“SFP”) is regulated by the Monetary Authority of Singapore and is a Capital Markets Service Licence holder (for dealing in capital market products), an Exempt Financial Adviser (for advising on investment products and issuing or promulgating analyses/ reports on investment products) and a Major Payment Institution (for domestic and cross-border money transfer services).

SFP may distribute analysis/report produced by its respective foreign affiliates within the StoneX Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations Recipients should contact SFP at (65) 6309 1000 for any matters arising from, or in connection with, this webinar.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism.

StoneX Financial (HK) Limited (CE No.: BCQ152) (“SHK”) is regulated by the Hong Kong Securities and Futures Commission for Dealing in Securities and Dealing in Futures Contracts.

StoneX Financial Pty Ltd (ACN 141 774 727) holds an Australian Financial Service License (AFSL: 345646) for Dealing in Securities, Exchange-Traded Derivatives Contracts, OTC Derivatives Contracts and Foreign Exchange Contracts, and is regulated by the Australian Securities and Investments Commission.

StoneX Securities Co., Ltd. (“SSJ”) (Co. Reg. No 010401047199) is regulated by the Japanese Financial Services Agency as a Type-I Financial Instruments Business Operator (Kanto Local Finance Bureau (FIBO)No.291’), is a member of the Financial Futures Association of Japan for dealing and broking FX and FX Option transactions, and is a member of the Japan Securities Dealers Association for dealing and broking stock indices and option transactions.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

The report/analysis herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

© 2026 StoneX Group Inc. All Rights Reserved.

Our subscribers have access to comprehensive market analysis from StoneX spanning commodities, equities, currencies and more.

Gold has been on a rollercoaster ride in recent quarters - how will the precious metal fare in Q2? Read our full outlook!

How will major US indices fare in Q2 after the big swoon in March? Read our full outlook!

EUR/USD slides toward a make-or-break level as Fed bets shift. Can support hold or is a larger breakdown underway?

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bi-lateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve; our financials and record of accomplishment are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform, to “boots on the ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.