- Fed easing and BOJ normalisation priced next year

- Risk sentiment key as volatility can flip flows

- April and October seasonality positive, summer soft

- Politics and fiscal risks could drive sharp rates and FX repricing

USD/JPY 2026 Outlook Summary

USD/JPY starts 2026 with the policy divergence trade largely exhausted, shifting attention to surprises and second-order factors. Interest rate spreads remain supportive but look increasingly fragile as expectations evolve. Seasonality adds nuance: April and October often lean positive around Japan’s fiscal calendar, while summer tends often sees softness. Technicals point to rallies being faded as spreads compress and risk assets struggle for traction, reinforcing a neutral to bearish bias. Intervention risk and fat left-tail shocks, from Fed independence uncertainty to tariff rulings, loom large and threaten to upend familiar these dynamics. Modest downside is the base case, but politics and volatility could change the script fast.

Fundamental Outlook: Divergence is priced, surprises will drive the tape

The easy part of the USD/JPY story is done. Policy divergence is largely in the price, so the next leg depends on how expectations shift and where surprises land. For now, the Fed is expected to ease as inflation cools, while the BOJ moves cautiously toward normalisation, guided by wages and services inflation. Wide interest rate differentials still support the dollar, but that influence is fragile. Faster Fed cuts or a hawkish BOJ could compress spreads quickly, challenging the carry bias and pressuring USD/JPY. A slower Fed and patient BOJ would do the opposite, although volatility spikes can interrupt any trend.

Risk sentiment is the second pillar. The yen’s funding role in carry trades means asset price performance and volatility matter. Strong gains with subdued volatility tend to reinforce yen weakness, while volatility shocks can drive rapid yen repatriation. When risk appetite is buoyant, rate differentials dominate. When volatility spikes, sentiment and positioning take over.

That familiar rates-and-risk dynamic could be upended quickly in early 2026 by two fat left-tail risks from the United States, both carrying the potential to reshape policy and fiscal expectations in ways markets are not pricing.

The first is Fed independence, and it goes well beyond who becomes the next chair. Lisa Cook, a sitting governor, was fired by Trump, and her case on the legality of that dismissal begins at the Supreme Court on 21 January. A ruling against her opens the door for Trump-aligned appointments to the Board of Governors, likely shifting the FOMC sharply dovish. Jerome Powell is another swing factor. He can remain as a governor until January 2028, well past his term as chair ends in May. Staying would act as a check on politicisation, though it would be highly unusual. If he leaves, the balance tilts decisively toward policy being set for political rather than economic reasons, raising the risk of a slide in longer-dated Treasuries and the dollar.

The second risk concerns trade policy. A Supreme Court ruling on reciprocal tariffs could reignite fiscal uncertainty. A loss for the administration would force tariff revenues to be refunded and open the door to secondary lawsuits against the government. That amplifies the risk of a significant widening in the primary fiscal deficit, which may pressure long bond yields and dollar. Timing for both rulings is uncertain, but the impact would generate material downside risk for USD/JPY if either lands.

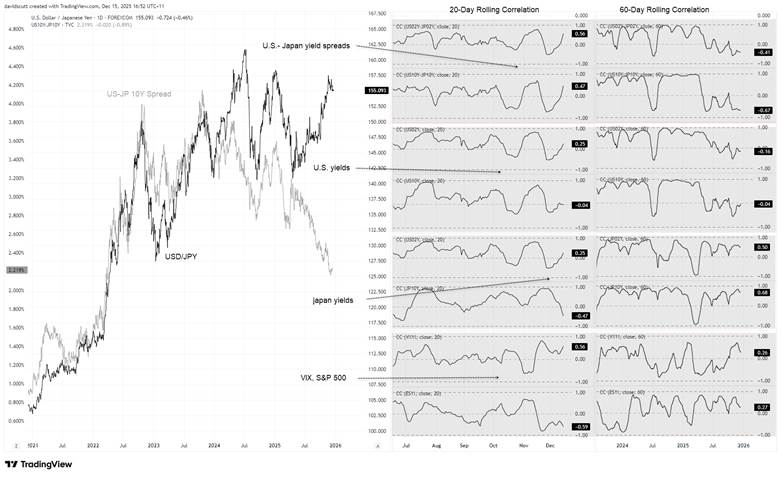

Correlation Analysis

Source: TradingView

USD/JPY tracked U.S.–Japan 10-year spreads closely until Liberation Day, when the reciprocal tariff announcement broke the link. Despite spreads staying wide, the relationship fractured, reminding traders that political shocks can override textbook rate dynamics.

Japan’s rate outlook can influence the pair at times, but similarities in correlations between outright U.S. 10-year yields and 10-year differentials suggest U.S. rates remain the dominant force. Rolling correlation data reinforces this. The 60-day correlation with both outright U.S. yields and 10-year spreads isn’t significant now, but strengthening in the 20-day window hints the rates-dollar-yen dynamic may be reasserting itself.

Before Liberation Day, USD/JPY often held positive relationships with yield differentials and outright U.S. yields for extended periods, only briefly interrupted by volatility spikes such as the Q3 2024 U.S. growth scare. Outside those episodes, risk appetite has been secondary. Correlations with VIX and S&P futures have rarely been meaningful, suggesting risk appetite and volatility only dominate when fears escalate quickly.

What matters now is whether the short-term rebound in rate correlations sticks. If it does, the familiar playbook returns: spreads and U.S. yields drive the tape, with risk sentiment playing a supporting role. If it fades again, traders should brace for a market that trades more on headlines and volatility than policy.

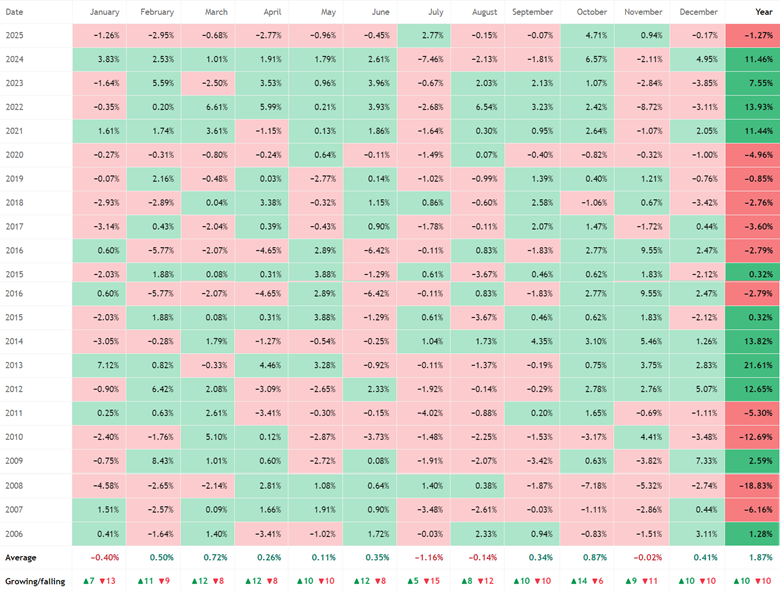

USD/JPY Seasonality

Source: TradingView

Seasonality can help frame expectations but it does not guarantee outcomes. The data say January is often weak for USD/JPY while months around the start of Japan’s fiscal year on 1 April tend to lean positive. October, after Japan’s fiscal half-year, also has one of the highest win rates which points to capital flows, carry positioning and rebalancing playing a role.

Seasonality tends to shift during the summer months. July has recorded five positive and 15 negative outcomes across the sample, while August shows eight positive and 12 negative. The averages are modest, yet the skew is difficult to ignore. One explanation is the reduction in liquidity during the northern hemisphere holiday period, which can amplify volatility and allow reversals to extend further. In such conditions, there is often a tendency to reduce risk exposure.

Bottom line, seasonality is context not a signal. Use it to tweak bias and sizing when it lines up with rates and risk and fade it quickly when the macro regime says otherwise.

Fed, BOJ Policy Expectations

Source: Bloomberg

This analysis is being prepared ahead of the Bank of Japan’s 19 December meeting, where it is widely expected to deliver a 25bp hike to 0.75%. Swaps price a 94% chance of that outcome, and the remaining assumptions here are based on it occurring without a shock hold.

Another full hike is priced by October 2026, with the risk of it arriving earlier flipping above 50% by June. Markets appear comfortable with this path given no adverse carry trade unwind so far. The outlook will hinge on inflation and wages, household spending and export demand. The spring wage negotiations will be critical as sustained real wage growth is likely needed to cement the cycle between firm demand and domestic inflation. A rapid yen appreciation without this would risk forcing the BOJ to abandon hikes and potentially ease again.

That puts greater emphasis on the US, given Fed policy tends to drive USD/JPY. Two full cuts are priced by October 2026, with the first favoured by April at over 80%. Risks lean towards deeper easing if the FOMC turns more dovish should Powell and Cook depart. Political pressure for lower rates ahead of November midterms could add to that bias, potentially pressuring USD/JPY in response.

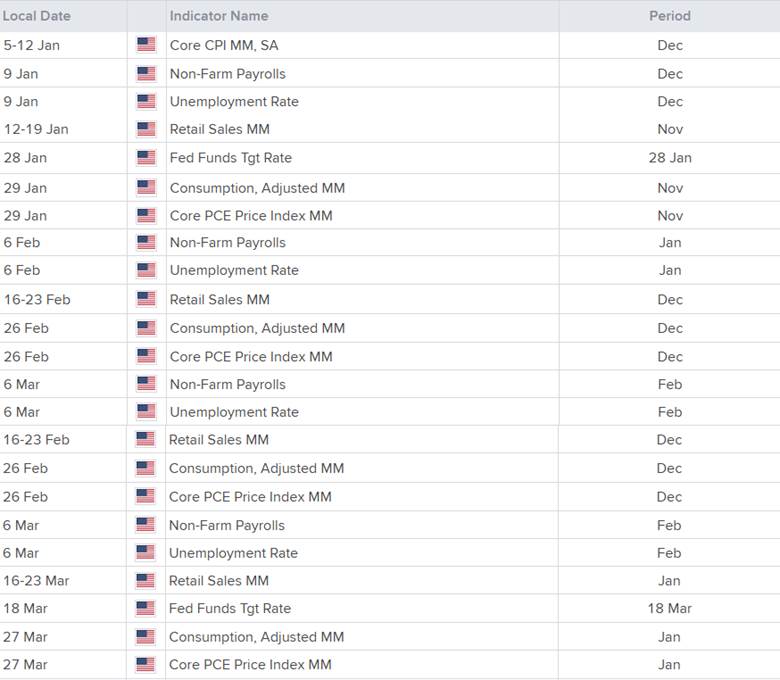

Q1 Event Map

United States

Source: LSEG (U.S. Eastern time)

Key events to watch include non-farm payrolls, unemployment, retail sales and broader consumption prints, alongside FOMC decisions. While the core PCE deflator remains the Fed’s preferred inflation gauge, core CPI tends to generate the most market volatility. Note the ongoing government shutdown makes release dates fluid early in the year.

As things stand, most FOMC members appear to be prioritising the full employment mandate over price stability, easing pre-emptively on labour market concerns while looking through inflation that remains above target. That puts greater emphasis on labour data as the key driver for policy expectations and USD/JPY directional risk.

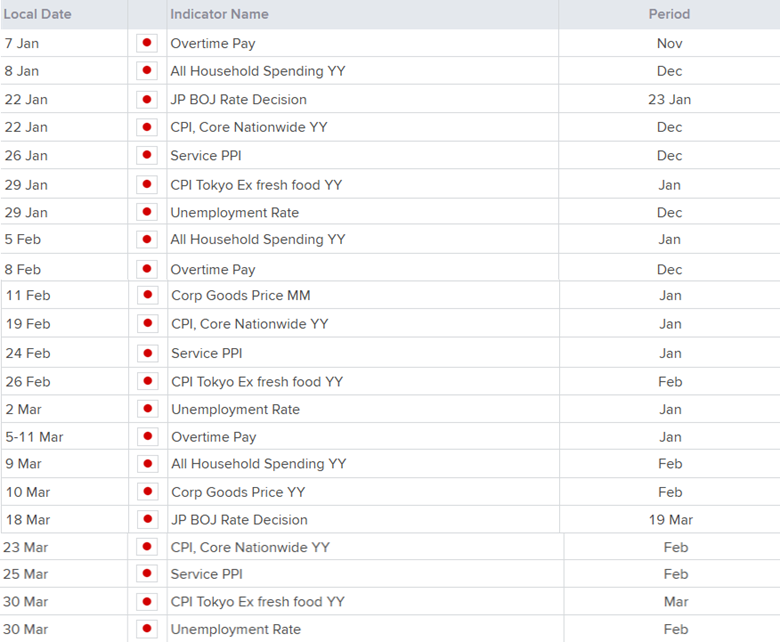

Japan

Source: LSEG (U.S. Eastern time)

Tokyo CPI stands head and shoulders above the rest when it comes to key Japanese data, setting the tone for the nationwide report three weeks later. Other releases are secondary in importance, with services inflation, household spending, wages and unemployment useful for assessing the sustainability of wage-driven inflation.

USD/JPY Directional Risks

Source: TradingView

Given elevated asset valuations and the prevailing rates backdrop, directional risks for USD/JPY in 2026 skew sideways to lower rather than higher. Fat left-tail risks around Fed independence and the Supreme Court ruling on reciprocal tariffs reinforce that bias. Price action adds weight, with each of the last two rallies failing to break the 2024 peak, creating a pattern of lower highs. Intervention risk compounds the challenge, making a sustained push above 161.95 unlikely. The probability of USD/JPY finishing the year above that level is seen around 10%.

Immediate resistance sits at 158.76, marginally above current levels. From there down to key support at 140.25, the probability of USD/JPY remaining within that range is high, around 75%. The remaining 15% is attached to an abrupt downside break beyond 140.25, likely triggered by a major risk-off event. Fed independence and tariff revenue risks aside, a sharp correction in AI-related equities could act as a catalyst. Another could be the Fed adopting policies to cap long-term bond yields via large-scale QE or yield curve control, with the release valve likely a substantially weaker USD.

Technical View

Nearer term, USD/JPY looks toppy as we approach 2026. Rallies are being sold into while weekly RSI (14) and MACD are rolling over from overbought territory, signalling waning bullish momentum despite the pair remaining in an uptrend from April’s lows. The price looks heavy and vulnerable to downside, putting levels such as 154.45, 153.00, 150.90 and the 50-week moving average on the radar before the April trendline comes into view. Below that, 145.90 and 142.50 are next in line ahead of key support at 140.25.