- Energy shock reinforcing US–Japan divergence

- Yen and JGBs sold together, signalling a rising risk premium

- Policy gap persists as rate differentials widen despite BoJ tightening

- 160 in focus as intervention risks build

- Downside risks tied to US labour weakness, carry unwind and BoJ intervention

USD/JPY Q2 Outlook Summary

USD/JPY enters the June quarter with strong tailwinds, with fundamentals and technicals aligning to support a push towards multi-year highs, even as the risk of Bank of Japan intervention builds near key levels. Recent price action reflects how differently the US and Japan are positioned as the Iran war extends into a second month, with the US largely insulated as a self-sufficient energy producer, in stark contrast to Japan’s vulnerabilities as a major importer.

Energy Shock Driving US–Japan Divergence

Higher energy prices remain the key transmission channel for USD/JPY, feeding into inflation while raising downside risks to growth. The US is not immune, remaining exposed to global pricing, but its vast domestic energy resources suggest the initial impact is more likely to be higher inflation rather than a material hit to activity, even if supply disruptions persist.

Japan faces a very different backdrop, with existing fiscal and structural vulnerabilities now being amplified by the energy shock. As a major energy importer, it is not only exposed to higher prices but also potential supply shortages, with a large share of crude sourced from the Gulf. That leaves it far more vulnerable to elevated inflation and downside risks to growth.

For FX, that divergence continues to favour USD/JPY upside.

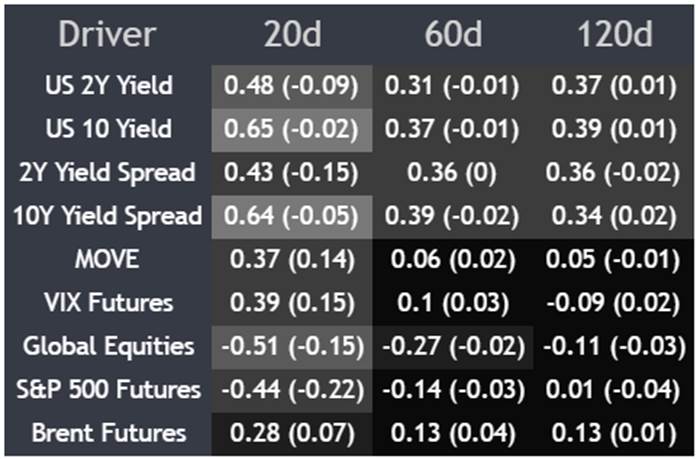

Rates Back in Control, but for How Long?

Source: TradingView

The US rate outlook has reasserted itself to some degree as a driver of USD/JPY over the past month. However, while the pair is once again responding to moves in US yields, the longer-term relationships are much weaker, raising questions about how durable that link will be.

It also suggests this is no longer just an energy story feeding through rates. The relationship between energy prices and US yields across the curve has been weak over the past month, pointing instead to a broader mix of relative inflation and growth risks driving price action.

Beyond rates, the more notable shift is how USD/JPY is behaving relative to broader risk sentiment. The pair is now showing positive relationships with US bond and equity volatility, while remaining negatively correlated with global and US equities. That often means the yen weakens when volatility rises and stocks fall, suggesting it is being treated more like a risk asset than a safe haven or funding currency.

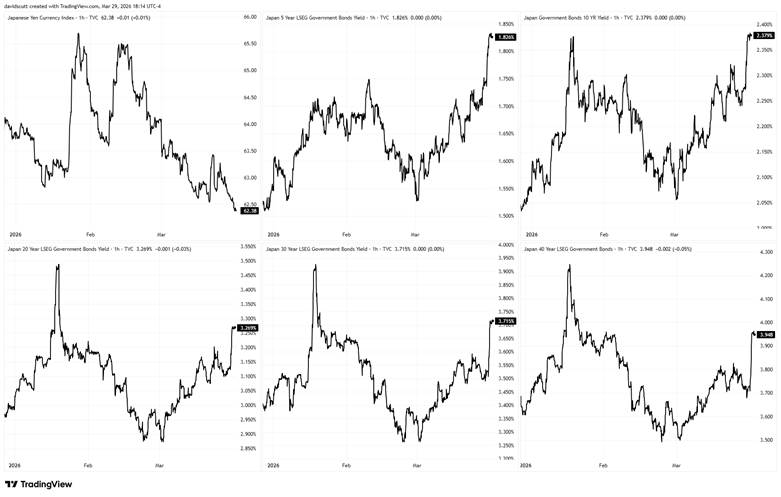

Questioning Japan’s Fiscal and Economic Outlook

The price action in Japanese markets is sending a clear message. This is not just a USD strength story, it is a yen weakness one. The decline in the yen against a broad basket of trading partner currencies, shown in the top left pane below, makes that clear.

That weakness is building on existing vulnerabilities. Concerns around Japan’s longer-term fiscal outlook were already elevated prior to the Iran conflict, following the election of reflationist Prime Minister Sanae Takaichi with a strong lower house majority earlier this year. The energy shock has only amplified those risks.

While Japan is not running an aggressively expansionary fiscal position relative to other developed economies, it is operating with a public debt burden of around 250% of GDP, alongside rapidly ageing demographics and an economy highly exposed to global trade. This combination increases its sensitivity to a sustained energy shock, with rising inflation and weaker activity adding to the strain.

Source: TradingView

Defending the Yen or Containing Yields?

The simultaneous sell-off in the yen and Japanese government bonds reflects growing concern around Japan’s fiscal and economic outlook. This is not a Bank of Japan policy normalisation story, but one where investors are demanding greater compensation for risk.

Japanese policymakers are in a difficult position. Markets are pushing yields higher while weakening the yen at the same time, forcing a trade-off in how the Ministry of Finance and the Bank of Japan respond. In effect, the market is signalling that to absorb these risks, either yields need to rise further, or the yen needs to weaken to provide the adjustment.

Intervening to support the yen risks shifting pressure into bonds, with investors demanding higher yields to hold JGBs. Alternatively, ramping up bond purchases by the Bank of Japan to contain yields risks adding further downward pressure on the yen by increasing liquidity and widening rate differentials.

FX intervention does not remove the underlying fundamental concern, it merely shifts where it shows up. As a result, it is unlikely to do more than slow the pace of yen weakness unless it is backed by a more meaningful shift in underlying fundamentals.

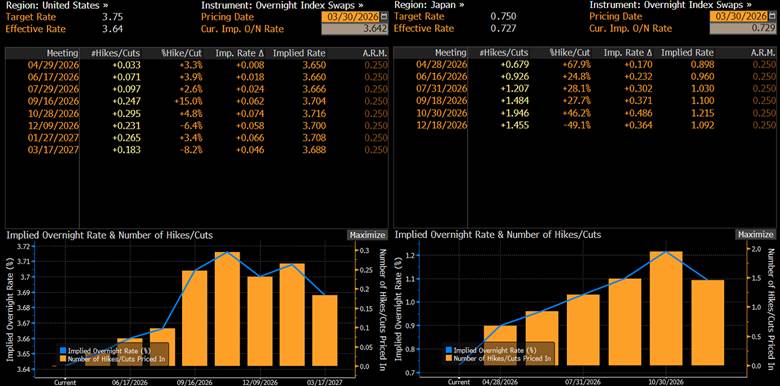

Fed–BoJ Policy Paths Still Far Apart

Source: Bloomberg

The escalation in the Gulf has triggered a sharp hawkish repricing in the US rate outlook, with markets now pricing the risk of a hike, a clear reversal from early March when more than two cuts were expected. However, with the Fed balancing price stability and full employment, markets remain reluctant to price an aggressive tightening cycle, particularly as employment growth slows.

That stands in contrast to pricing for the Bank of Japan, which is focused solely on its inflation objective. While labour market conditions matter for Japan’s inflation outlook, they do not carry the same weight in policy deliberations, leaving further tightening more firmly embedded, with a hike close to fully priced by June and nearly two by October.

Even with that more hawkish profile, it has not been enough to offset the widening in yield differentials between the US and Japan across the curve over the past month.

Data Risks Centre on Jobs and Prices

What ultimately determines whether that gap narrows will be the incoming data.

In the US, the key releases are non-farm payrolls and consumer price inflation, with indicators such as producer prices, GDP, retail sales and even the core PCE deflator, the Fed’s preferred inflation measure, playing a secondary role. Until recently, the Fed has shown a clear sensitivity to labour market conditions, easing policy despite inflation remaining above target.

While higher energy prices have seen some policymakers lean towards the risk of hikes, the real test will be how the labour market evolves. A sharper deterioration, which is not difficult to envisage, would likely see markets flip towards pricing cuts, taking some heat out of the US dollar.

In Japan, Tokyo CPI remains the key release, arriving ahead of the national series and offering a reliable lead on underlying inflation trends. With the BoJ focused on establishing a virtuous cycle of wage growth feeding through to consumption and broader economic expansion, wages and consumption data will also be closely watched.

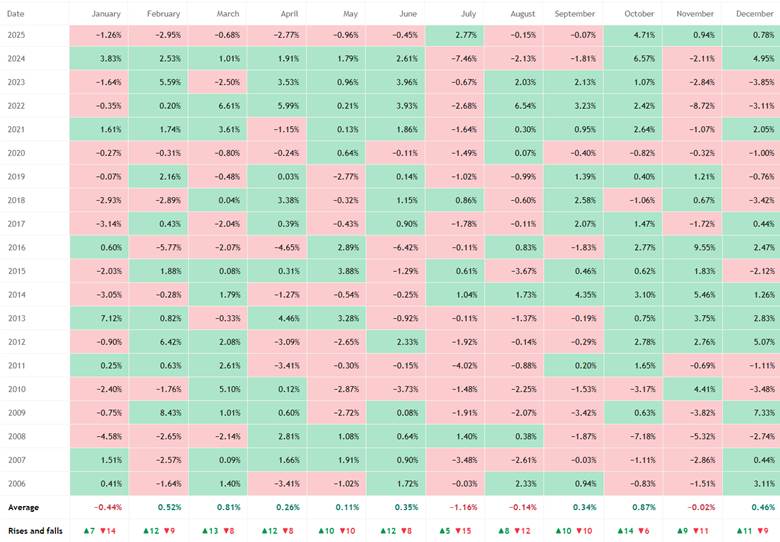

Seasonality Offers Limited Insight

Source: TradingView

Seasonality offers little guidance for USD/JPY. While average returns in the June quarter point to modest upside, the dispersion in outcomes is wide, both in direction and magnitude.

Looking at the breakdown, April and June have only a slight skew towards gains, with a 12–8 split between positive and negative months, while May is evenly balanced at 10–10. That lack of consistency highlights how unreliable seasonal signals can be.

The broader takeaway is that seasonality should be treated as a secondary consideration at best, and even that may be generous in the current macro environment.

160 the Key Battleground for USD/JPY

Source: TradingView

USD/JPY remains a buy-on-dips play, with the price continuing to print higher highs and higher lows, and oscillators remaining broadly supportive even as signs of waning upside strength emerge. While RSI remains elevated, it is starting to flatten near recent highs, pointing to a loss of momentum rather than a clear divergence signal.

160 remains a focal point entering the June quarter given the history of yen intervention above it.

On the topside, 161.95 is the key level to watch, coinciding with the 2024 high where the BoJ also acted. A break above would leave little in the way of nearby resistance, shifting the focus towards longer-term historical levels, with the September 1978 low of 177.05 the first reference point.

On the downside, 157.50 has acted as both support and resistance this year, making it an important level to watch below current levels. The January 2026 swing low of 152.10 is another key reference point, especially with the influential 200-day moving average sitting just above and rising.

Key Upside and Downside Risks

From a fundamental perspective, upside risks remain tied to a continuation of the current geopolitical backdrop. Persistently elevated energy prices, a Fed that remains reluctant to ease or even leans towards hikes, or a cautious pace of tightening from the Bank of Japan would likely see USD/JPY test and potentially push through 161.95.

On the downside, a de-escalation in the Middle East, a sharper deterioration in US labour market conditions, or a more forceful policy response from the Bank of Japan could see the pair come under pressure.

Intervention risk presents another obvious downside risk. However, history suggests it tends to have a more lasting impact when aligned with underlying fundamentals rather than working against them. That said, depending on the scale of any response, past episodes highlight the risk of an abrupt pullback, with levels such as 152.10 or even 150.90 potentially coming back into view.

Another downside risk is a disorderly unwind in carry trades. A combination of higher borrowing costs in Japan, a strengthening yen and a meaningful decline in global asset prices would amplify the risk.