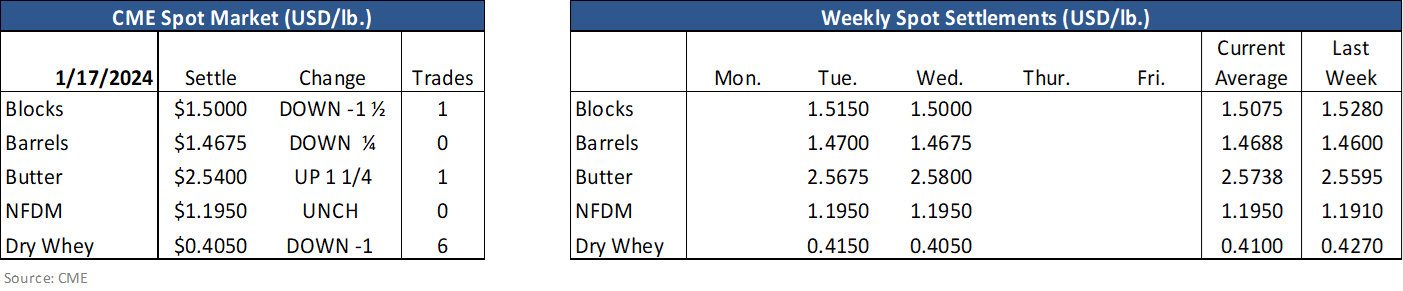

The cheese market went rather quiet Wednesday with just one block changing hands and no trades on the barrel market. Both prices fell slightly so you could chalk the lack of activity to a reduced desire by buyers. Class III and Cheese futures turned lower as futures prices revisited – or in some cases – etched out a new low for this move (Q2 specifically). Futures trade volume was more moderate for both contracts and more eye-catching futures price weakness you’d expect in a still-bearish market cycle seems a tall order.

There could be several reasons for the lack of real aggressive selling. For starters, the speculative money in the market is already quite short and there is a limit to how many new sellers will enter the market or add to their short positions around current levels. While speculative traders like to add to winning positions (in this case short positions), its not abundantly clear that the cheese price ought to collapse more – or even stay down here another month.

Global market price action is firm with EU cheese trading between $1.80 and $2.00. GDT cheddar finished this weeks’ auction at$1.91/lb. While there seems to be plenty of milk at the moment, there are growing concerns over both US and EU milk production this year. And the cheese balance table looks rather balanced. Cheese makers have been doing a good job of matching weak cheese demand with weak cheese production. U.S. domestic cheese disappearance increased by 1.7% in October and 1.2% in November. YTD cheese disappearance is up 0.7% with American style cheeses up 2.2% while mozzarella is up just 0.1%.

So if you look beyond the spot cheese market, there doesn’t seem to be a lot of reason for lower cheese prices from here. But the spot cheese market has the final say. If sellers have product they can’t move elsewhere, spot prices can stay depressed. But be advised: that’s really been the story of the last two months or so.

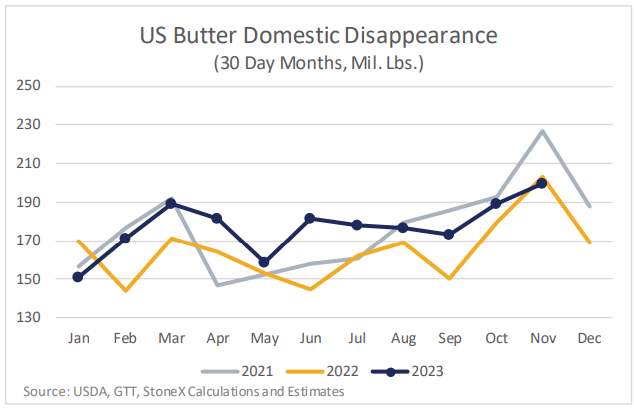

Domestic butter disappearance cooled a bit in October and November. Disappearance had been running +10% or higher for most of Feb-Sep, but it slowed to +5.8% in October and -1.6% in November. YTD domestic butter disappearance is up 7.8% (on top of a 6.2% decline last year).

Butter futures traded mostly mixed on light volume again Wednesday. Spot butter gained 1.25 cents to $2.58 on 1 trade. The lackluster spot trade this week signals a rather content butter market around current levels, which has really been more or less the case for the past 9 weeks. That’s right, spot butter has traded in a 22.5 cent range for the past 9 weeks. We’re in week 10 now. Futures need some new sense of worry to continue higher and we don’t have that today. End-user buy side interest remains a key feature but about a dime lower than current futures today. With IDFA next week, we’ll report back on any changes in sentiment for butter. For today, that sentiment seems to be mild worry of higher prices.

There is less worry on the NFDM side on the equation today. NFDM+SMP domestic disappearance was strong Feb-Jul, but when prices started rallying, disappearance has slowed significantly. YTD domestic NFDM+SMP disappearance is down 7.7%. This reduces some of the potential stressors around dwindling inventory levels, but should this continue likely means more sideways action for NFDM. Yesterday’s spot and futures action was steady and steady slightly lower. Futures trade volume got a boost, however, with 331 contracts changing hands and open interest up 170 contracts. Stable market for now.

Corn and beans still look to be determining a place for lows. Fundamental help looks to be hard to come by until we turn attention to U.S. planting in a couple months. The Jan USDA report data dump gave no help to the bulls; South America continues to dominate the conversation. Look for a mixed start to today.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided. References to over-the-counter (“OTC”) products or swaps are made on behalf of StoneX Markets LLC (“SXM”), a member of the National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM. StoneX Financial Inc. (“SFI”) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (“SEC”) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Adviser. References to securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to exchange-traded futures and options are made on behalf of the FCM Division of SFI . StoneX is a trading name of StoneX Financial Ltd (“SFL”). SFL is registered in England and Wales, Company No. 5616586. SFL is authorized and regulated by the Financial Conduct Authority [FRN 446717] to provide to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorised to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorised & regulated by the Financial Conduct Authority under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorised by the Financial Conduct Authority. StoneX Group Inc. acts as agent for SFL in New York with respect to its payments services business. StoneX APAC Pte. Ltd. acts as agent for SFL in Singapore with respect to its payments services business. ‘StoneX’ is the trade name used by StoneX Group Inc. and all its associated entities and subsidiaries.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

© 2024 StoneX Group Inc. All Rights Reserved.

Discover more insights