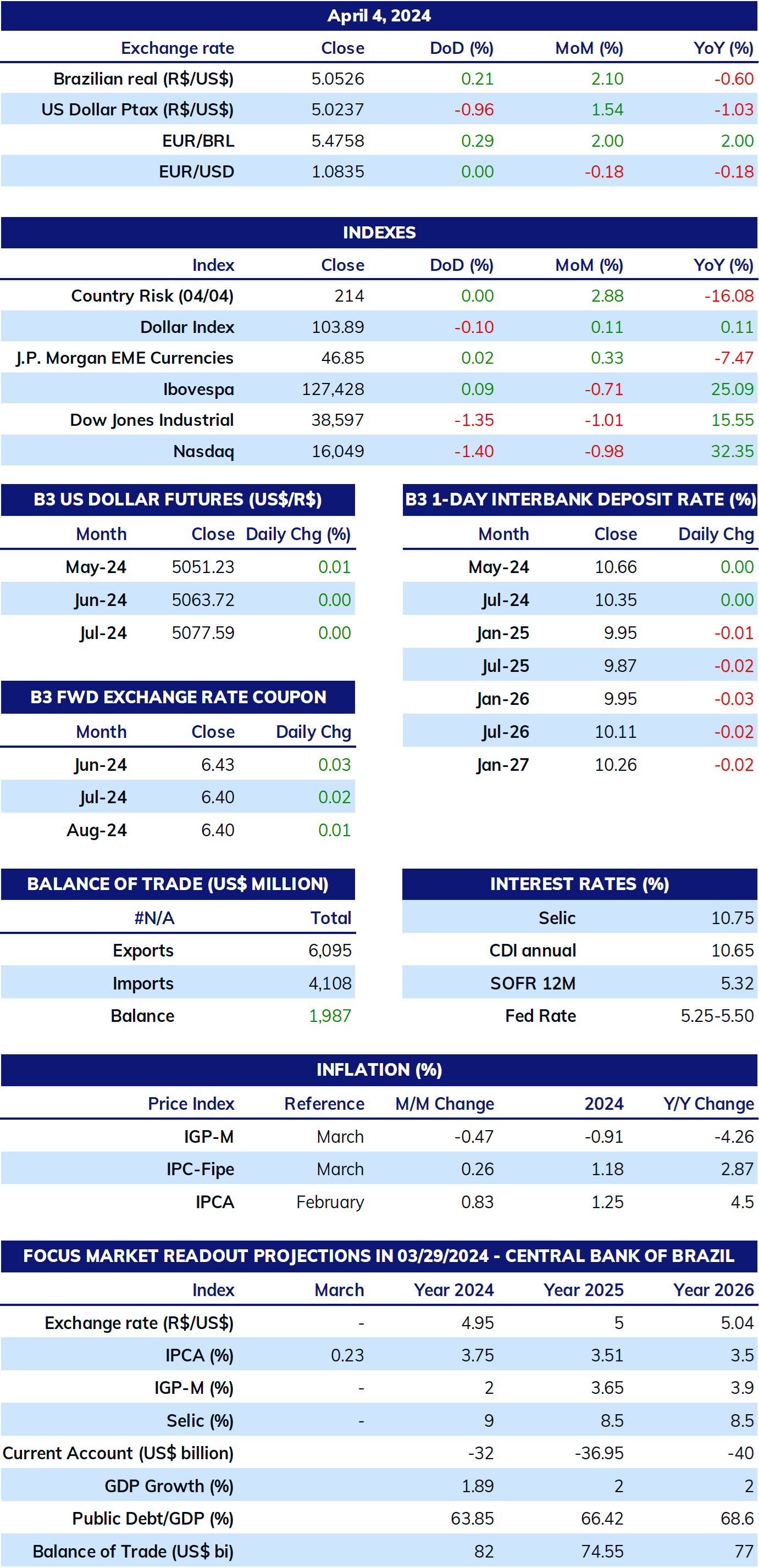

- The outlook for moderation in Brazil's March IPCA is expected to increase the perception that COPOM will maintain its pace of 0.50 p.p. interest rate cuts to the Selic rate beyond May, which would harm the Brazilian interest rate differential and weaken the BRL.

- The ECB monetary policy decision should reaffirm bets on a cycle of interest rate cuts by the authority starting in June, which would falter the euro and contribute, by length, to the strengthening of the USD.

- Forecast of a slight decline in the US CPI may lessen agents' fears about American inflation and increase bets that the Fed will make three interest rate cuts in 2024, reducing the attractiveness of American bonds and weakening the USD.

- FOMC minutes may bring more information about the Committee's more flexible stance in May and reinforce bets that the Fed will make three interest rate cuts in 2024, reducing the attractiveness of American bonds and weakening the USD.

- Expectation of more favorable data for the Chinese economy could raise growth and demand expectations for the country, favoring the performance of risky assets, such as stocks, commodities, and currencies of emerging countries, like the BRL.

The week in review

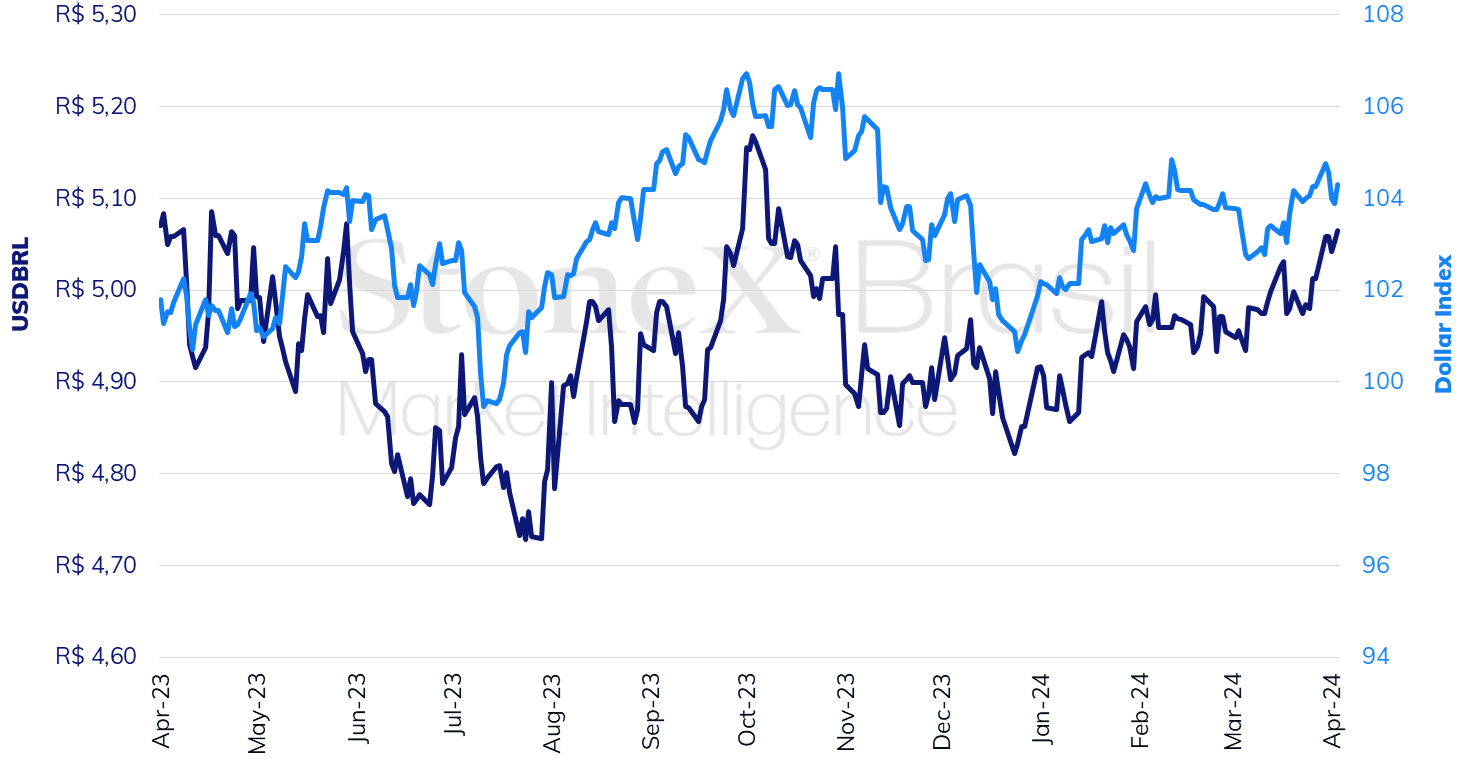

The week was marked by the wide fluctuation of the value of the American currency abroad, amidst a sharper reading than expected for the country's industrial activity and labor market in March and weaker than expected for the service activity. Not even the first exchange rate intervention by the Central Bank in 15 months could contain the depreciation of the BRL real.

The USDBRL ended the week higher, closing Friday's session (05) at BRL 5.065, a weekly gain of 1.0%, a monthly gain of 1.9%, and an annual gain of 4.4%. The dollar index closed Friday's session at 104.3 points, a change of 0.0% for the week, +0.2% for the month, and +3.2% for the year.

THE MOST IMPORTANT EVENT: March US CPI

Expected impact on USDBRL: bearish

After the higher readings in January and February for the core Consumer Price Index (CPI) in the US, which excludes volatile food and energy components, a slight decrease is expected in the indicator for March on Wednesday (10), around 0.3% for both the full index and its core. If confirmed, the amount should not be enough to dispel fears that inflation is becoming more persistent in the US but would keep the possibility of a first interest rate cut by the Fed in June viable. Last week, Fed President Jerome Powell raised investors' optimism about the possibility of interest rate cuts throughout 2024 by stating that the risk scenario remains largely unchanged, with "solid growth, a strong but rebalancing labor market, and inflation moving down toward 2% on a sometimes bumpy path". So, it seems that the institution authorities are hopeful that January and February were outliers, but this may change if the CPI is higher than expected for the third consecutive month.

FOMC Minutes

Expected impact on USDBRL: bearish

Also, next Wednesday (10), the Federal Reserve will release the minutes of its last monetary policy decision on March 20. The document is always released three weeks after the decisions of the Federal Open Market Committee (FOMC) and, therefore, is a bit outdated. Still, the statement, the Summary Economic Projections, and Powell's press conference surprised investors by downplaying the recent stronger economic data, stating that the broader economic outlook remains unchanged and maintaining the possibility of three interest rate cuts this year. Accordingly, the minutes can bring more details about the discussions on the economy's risk balance, that is, whether there was any concern among FOMC members about the possibility of the current monetary tightening being insufficient to bring consumer inflation back to the institution's annual target of 2% as well as about the possibility of the current monetary tightening causing an excessive slowdown in economic activity and the labor market. Most analysts generally observe that the conjuncture is more favorable for inflationary risks than recessive ones. Additionally, comments on the Fed's asset balance reduction policy (quantitative tightening) and its impacts on the liquidity of the American financial system will be closely monitored by analysts.

March IPCA

Expected impact on USDBRL: bullish

After the last Monetary Policy Committee decision's more cautious statement, investors should follow the publication of the Broad National Consumer Price Index (IPCA) for March. The median estimate for the month is a monthly increase of 0.27%, compared to 0.83% growth in February. If confirmed, the index slowdown should reduce the Central Bank's recent concerns and magnify the possibility of another 0.50 p.p. interest rate cut for the basic rate (SELIC) in the June decision.

Chinese economy data

Expected impact on USDBRL: bearish

After positive surprises with Chinese economic indicators last month, expectations for the Consumer Price Index (CPI) and the trade balance in March are more optimistic. The CPI is estimated to increase by 1.2%, and exports and imports are expected to grow by 6.0% and 2.0%, respectively. If the projections are confirmed, they can magnify foreign investors' risk appetite and strengthen the real.

ECB interest rate decision

Expected impact on USDBRL: bullish

The European Central Bank (ECB) is expected to keep the basic interest rate unchanged at 4.00% p.a., also maintaining its signaling for the interest rate trajectory in the unified currency bloc. Amidst a moderation of inflation and broad economic weakness in the economies of the bloc, the European economic authority says it is comfortable with the projections in the futures market for interest rates, which indicate that the first interest rate cut may occur in the June decision. Additionally, the economic scenario is more favorable for cuts in Europe than the US, which may lead the ECB to make more cuts than the Fed throughout 2024. Thus, the statement and the press conference can contribute to a weakening of the euro due to the prospect of a worsening interest rate differential compared to the US.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided. References to over-the-counter (“OTC”) products or swaps are made on behalf of StoneX Markets LLC (“SXM”), a member of the National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM. StoneX Financial Inc. (“SFI”) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (“SEC”) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Adviser. References to securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to exchange-traded futures and options are made on behalf of the FCM Division of SFI . StoneX is a trading name of StoneX Financial Ltd (“SFL”). SFL is registered in England and Wales, Company No. 5616586. SFL is authorized and regulated by the Financial Conduct Authority [FRN 446717] to provide to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorised to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorised & regulated by the Financial Conduct Authority under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorised by the Financial Conduct Authority. StoneX Group Inc. acts as agent for SFL in New York with respect to its payments services business. StoneX APAC Pte. Ltd. acts as agent for SFL in Singapore with respect to its payments services business. ‘StoneX’ is the trade name used by StoneX Group Inc. and all its associated entities and subsidiaries.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

© 2024 StoneX Group Inc. All Rights Reserved.

Discover more insights