Copper’s price performance on a YTD basis is currently flat, with prices dominated by macro headwinds over fundamentals, in which copper ore supply is being tightened. While the long-term view for copper over the decade is bullish, with well documented under-investment for mining projects forecast to create a semi-irreversible structural supply gap in the next five-years, where exactly does this leave copper for 2024? In this article we will explore the current dynamics that copper faces and our projections for the year ahead.

Copper LME 3M Price Performance

Macro Headwinds to Remain in Place over Q1

In our Metals Outlook 2024 report (link HERE), we outlined the key macro drivers for copper over the year, which all-in-all are tilted to the downside. However, if we break down the outlook on a quarterly basis, then in our view, we do not foresee the macro environment supporting higher copper prices in the near-term, with the latest comments from the Federal Reserve, global PMIs and indeed initial January data sweep from China, pointing to more pain ahead. However, over the course of H2, we see these headwinds retreating.

• Outcome of January’s FOMC Meeting

As expected, interest rates were held steady, with Chairman Jerome Powell reducing expectations for a March rate cut stating that he “does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably towards 2%". He followed on from this by saying “based on the meeting today, I would tell you that I don’t think it’s likely that the Committee will reach a level of confidence by the time of the March meeting”. In addition to this, Powell went on to say, “we believe that out policy rate is likely at its peak for this tightening cycle and that, if the economy evolves broadly as expected, it will likely be appropriate to begin dialling back policy restraint at some point this year”, “we are prepared to maintain the current range rate for the the federal funds rate for longer, if appropriate”.

To read in more detail, please see Rhona O'Connell report POWELL, EMPLOYMENT NUMBERS BOOST GOLD - here.

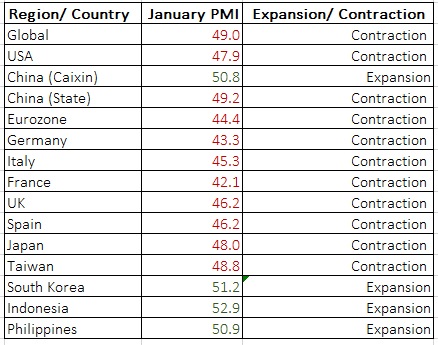

• Global PMIs Remain Deep in Recession

Global Manufacturing PMIs

• Fears over Weakening Chinese Confidence Offset Reality of Growing Copper Demand in China

The PBoC took advanced action last month to calm the waters within China when it comes to future growth prospects, with the central bank Governor Pan Gongsheng announcing (unusually) two weeks in advance that it will cut the Reserve Requirement Ratio by its largest amount since 2021. The ruling by Hong Kong Judge Linda Chan to liquidate Evergrande (the world largest indebted property developer), in addition to an incredibly weak performance by domestic stock market (among the worst performing in the world in 2023), has only moved to reduce confidence over a recovery in the country at the start of this year.

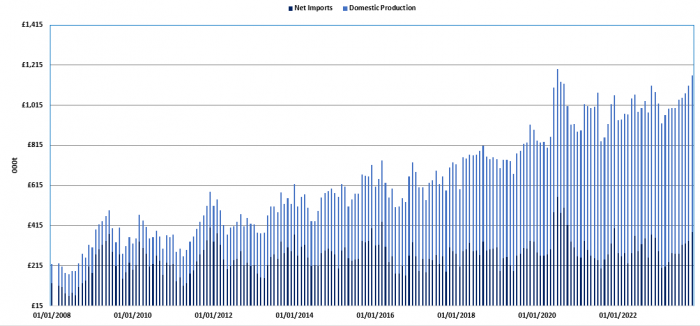

Yet despite these headlines, the reality for copper demand is positive, with apparent demand

(the summation of net imports and domestic output of refined material) having jumped to its highest level on record in 2023. It is important to note, that while copper demand for construction has been in decline, this has been offset by other sectors of demand, most notably, industrial, automotive, the green transition, consumer electronics and military applications.

Copper Apparent Demand

Copper is Well Placed to See Gains in H2

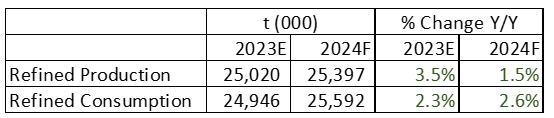

We forecast that from H2 onwards the prospects for base metals will start to improve, with an easing in monetary policy in the west paving the way for a resumption not only in consumer appetites, but downstream restocking. In addition to this, Chinese demand for copper is likely to post another record year, with demand accelerating by 2.6% Y/Y from 2.3% in 2023. Alongside this, with copper ore supply being challenged, we suspect that the copper market will move into a modest deficit in H2 upon the rebound in western demand.

Be Cautious for Bouts of Volatility

Given the historically low levels of global visible stocks available for copper, the expectation for potential price volatility is increased, and this year, we see a host of main events as possible market movers. Firstly, in March, the outcome of China’s Two Sessions is set to be pivotal in strengthening views on China’s pace of recovery this year; secondly, the timing of the first rate cut from the U.S. Federal Reserve and thirdly the outcome of the U.S. general election (and general elections in overall).

China’s Two Sessions

This is an event in which the National People’s Congress and China’s People's Political Consultative Conference hold their annual meetings to decide on legislation, economic targets, policy, Government budgets and personal changes. The outcome of these meetings lays out the tone of what to expect for growth over the next twelve months. Given the ongoing situation in the property market (which contributes ~25% of China’s GDP), market attention will focus heavily on language used in this area, in addition to comments over China’s view on its current relationships with major trading partners (i.e., Taiwan and the United States).

To read more about Two Sessions and our expectations please see Metals Outlook 2024 - here.

U.S. Federal Reserve

We are leaning towards H2 as the timing for the first rate cut, with the Federal Reserve (as a typical central bank), likely to run shy of cutting rates too soon for fear of reigniting inflation. In addition to this, external issues impacting oil and freight prices of late, only underscores this view. While we have no expectations that the first (and subsequently) rate cuts will result in an immediate rebound in downstream copper restocking and return in consumer appetites (given a lagged impact of ~6 months), the move to begin easing monetary policy will play a more subtle role, with investors revaluing copper’s longer-term prospects once again – arguably signalling, a potential bottom of the rout.

To read more about the outlook in the United States please see Metals Outlook 2024 - here.

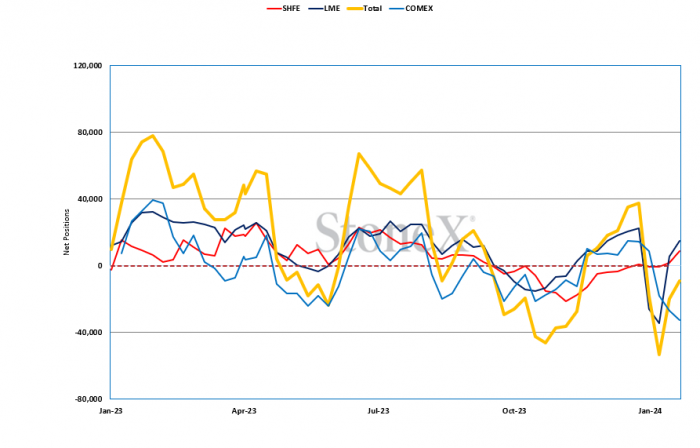

LME, COMEX & SHFE Net Speculative Investor Positioning

The Fundamental Picture of 2024

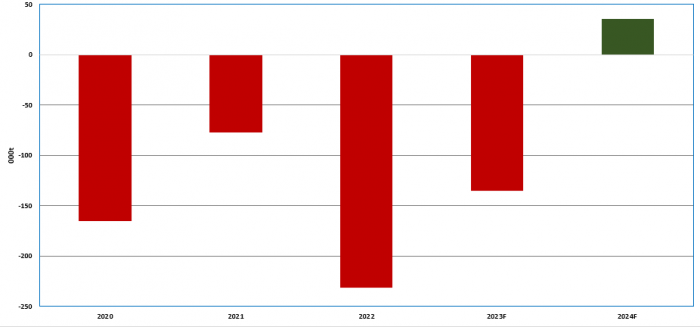

Despite ongoing copper supply disruptions removing over 600,000t of ore supply in our outlook for 2024 (roughly 2.7% of global ore supply), we are still forecasting that the copper market will move into a surplus this year on the refined side, driven by expanding domestic production within China, in addition to increasing capacities within countries such as Indonesia, Chile and the Democratic Republic of Congo (DRC). Please note, the DRC is on track to becomes the world second largest producing country of copper, overtaking Peru. Furthermore, with rising global visible inventories and the LME Cash-3M spread hovering around its widest contango since 2013, we have evidence in the near-term that the refined copper market is well supplied.

Meanwhile on the demand side, with Chinese consumption set to remain steady (with manufacturing partially offsetting weakness from the property market), a return in demand ex-China, particularly in H2 on falling western interest rates, will support higher copper prices, which in turn may encourage greater speculative investor interest. Please note, copper remains a favourite with investors given its long-term application in the green transition and long-term uncertainty over supply availably.

Forecast Supply & Demand

Copper Market Balance

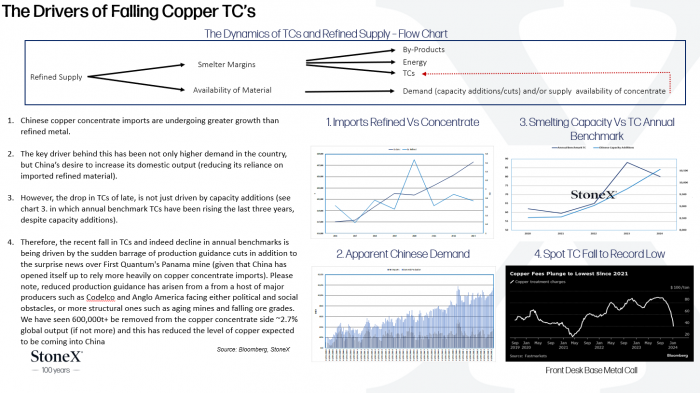

Additional Notes – The Reality of Falling Copper Chinese TC’s

To read in detail about copper concentrate supply cuts, please see our article 'Copper Separating Away from the Rest of the Suite' - here.

Please note, a risk to our forecast could arise from the potential re-start of First Quantum's Cobre Panama mine that contributes ~360,000t of copper a year (or 1.6% of global output). As it stands, Panama's Supreme Court ruled for the mine to close operations at the end of last year; however, with the upcoming general election in May, there is a chance this ruling may be revisited, although we have low-to-modest expectations the mine will come back online.

To read more about copper TCs and industrial stories, please view our

Weekly Base Metals Macro Report - here.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided. References to over-the-counter (“OTC”) products or swaps are made on behalf of StoneX Markets LLC (“SXM”), a member of the National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM. StoneX Financial Inc. (“SFI”) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (“SEC”) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Adviser. References to securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to exchange-traded futures and options are made on behalf of the FCM Division of SFI . StoneX is a trading name of StoneX Financial Ltd (“SFL”). SFL is registered in England and Wales, Company No. 5616586. SFL is authorized and regulated by the Financial Conduct Authority [FRN 446717] to provide to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorised to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorised & regulated by the Financial Conduct Authority under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorised by the Financial Conduct Authority. StoneX Group Inc. acts as agent for SFL in New York with respect to its payments services business. StoneX APAC Pte. Ltd. acts as agent for SFL in Singapore with respect to its payments services business. ‘StoneX’ is the trade name used by StoneX Group Inc. and all its associated entities and subsidiaries.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

© 2024 StoneX Group Inc. All Rights Reserved.

Discover more insights