The Outlook

It’s an annual rite that’s so reliable you could almost set a clock to it – or perhaps more accurately – mark your calendar by: the increase in trading volume and volatility within the financial markets in September and October after the ‘doldrums of summer’.

Why has this phenomenon proven so consistent over time? In part, volume rebounds at first simply as a practical function of more traders and managers returning from vacation to their desks with full attention focused on the markets and their positions therein.

What drives the tide change in volatility, as measured by benchmarks like the CBOE Volatility Index (VIX), is a little more complicated, says StoneX Head of Content John Kicklighter.

“There is a case of self-fulfilling prophecy when it comes to the seasonal liquidity and activity levels in the capital markets that spill into other areas of the financial system. So many have come to expect it as a natural rhythm of the market that they set ‘cruise control’”, he explains. “What’s more, that backdrop of quiet appeals to many as an environment to pursue yield while the cost of hedges can be re-evaluated. Inversely, as volume increases, the volatility typically climbs in tandem towards an October historical peak.”

Adding a further important relationship to these sea changes, broad market performance – as measured by recognizable benchmarks like the S&P 500 index – typically experience an inverse relationship to activity. “Historically, the averages suggest September and early fall trade can be some of the most difficult terrain of the year for the markets,” adds Kicklighter.

Implications for traders and the commodity complex

Despite the heightened risk from unpredictable conditions, directional and volatility traders tend to lick their chops each autumn. Volatility creates opportunities for price development and even momentum that can be cut off during more anemic summer periods.

On the opposite end of the spectrum, commodity hedgers can struggle with the costs brought on by volatility. Naturally, the same group is no stranger to seasonality in asset prices. But how many are vulnerable to a ‘double dip’ (e.g. a dovetail of peak seasonality in their commodity prices and peak VIX) in October? The answer varies by commodity, but the short answer is not many.

That is, unless the VIX surpasses 30, cautions StoneX Chief Commodities Economist Arlan Suderman.

“Based on my experience, it is difficult for just about any commodity to mount and sustain a rally when the VIX goes above 30,” he explains. “At that level, there is just too much fear in the market to hold on to so-called risky assets like commodity futures, and there is too much speculative money exiting these assets a result. You’d have to have a really compelling story behind that commodity’s rally to overcome this effect.”

Suderman points to a moment in March 2009 as anecdotal evidence for this dynamic.

“Corn plummeted at the outset of the Great Recession and kept falling through the early part of 2009,” he recalls. “Then, in March, the VIX finally crept back up above 30. And at that moment, it seemed, we found the bottom of the corn market.”

Seasonal volatility + X = 30?

So, what are the odds that a VIX that has traded below 25 for most of this calendar year gets to 30 or above this September-October? The answer may spring from the following factors as potential catalysts.

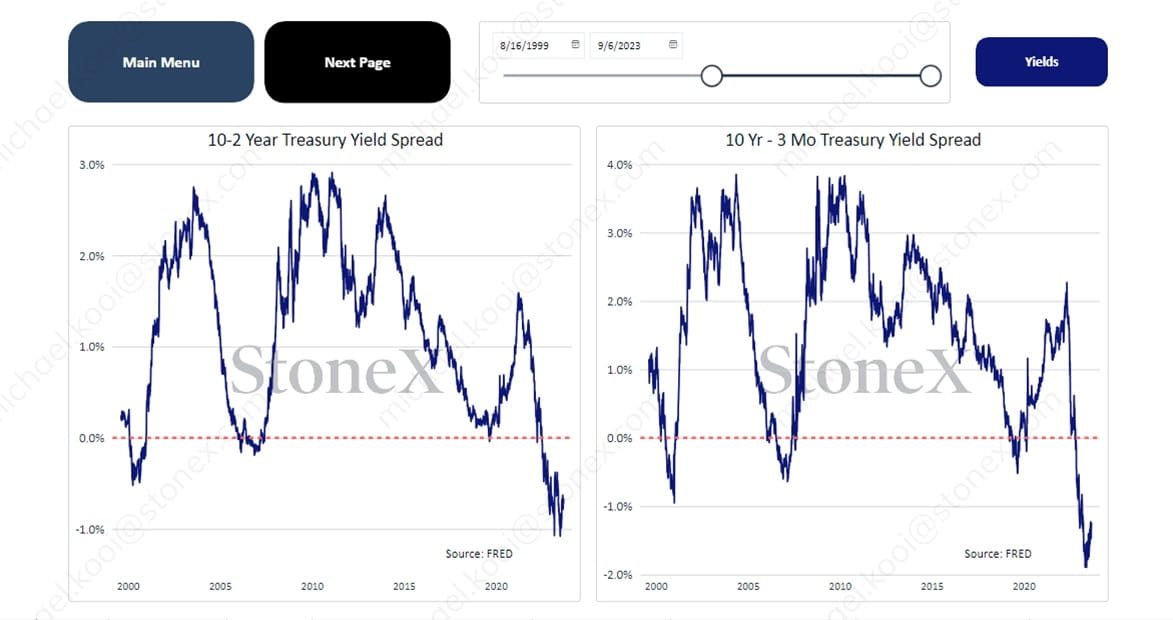

Treasury Yield Spreads

Two of the most popular recession indicators among investors and economists – the 10 - 2 Year Treasury Yield Spread and the 10 Yr – 3 Mo Treasury Yield Spread, respectively – have been blinking red for some time. Will economic conditions conform to these market signals? If so, volatility will likely rise.

Interest Rates

The U.S. Fed Open Markets Committee has maintained steadfastly that it will continue to pursue restrictive monetary policy so long as the data dictates the need to tame inflation – even at the risk of recession. Many analysts are looking to September and October meetings as a true test of the FOMC’s resolve. If markets don’t like the answer, or if a recession ensues, volatility will rise.

Black Sea Uncertainty

Ukraine seems to have turned the tables on Russia militarily, but there remains no end in sight to the war. Thus, the uncertainty shadowing supplies of grain, natural gas and oil-derived products from that region will likely persist. In fact, as winter approaches, Russian President Vladimir Putin may grow desperate and exert Russia’s leverage over these commodities to make Ukraine and its allies in Europe pay a higher price for their defiance of his will. Should that need for progress reach levels of desperation, it is even possible that he may do something rash with a form of catastrophic retribution – certainly a source of volatility.

Any of these factors could give volatility a goose this autumn – either individually or in concert. Add to these – and a myriad of other potentially systemic catalysts – the seasonal effects described above, and you could see some commodity hedges stressed to their breaking points.

That’s why “back to school” may be as smart of a time as any to re-evaluate positions and hone hedges. Liken this portfolio check to changing the batteries in your smoke detectors each year at the end of daylight savings.

For more charts related to autumn seasonality in the financial markets, visit StoneX Market Intelligence.

Originally published as part of The Outlook Newsletter

Vol. 1, Issue 4C

See why StoneX is a partner of choice