Many Faces of Gold

How to start gold trading online

Gold: The Many Faces of the Precious Metal

For traders and investors, the debate about why to buy gold – or, indeed, why to sell it – rages on.

The precious yellow metal continues to provide compelling reasons for investment and speculation, even if nobody can put forward a single unified answer as to its role within a portfolio. It remains close to its record high set during the Covid-19 pandemic, and offers a level of market depth that can be surprising to non-specialists:

- $183 billion average daily volume (including futures and ETPs), 78% of the S&P 500’s $235 billion

- LMBA averages $63 billion daily, plus $105 billion over the counter

Historically, there have been three main reasons why people trade gold; as a commodity, to hedge against inflation, and as a safe haven. But which best explains its current performance?

Part 1: Gold is a commodity

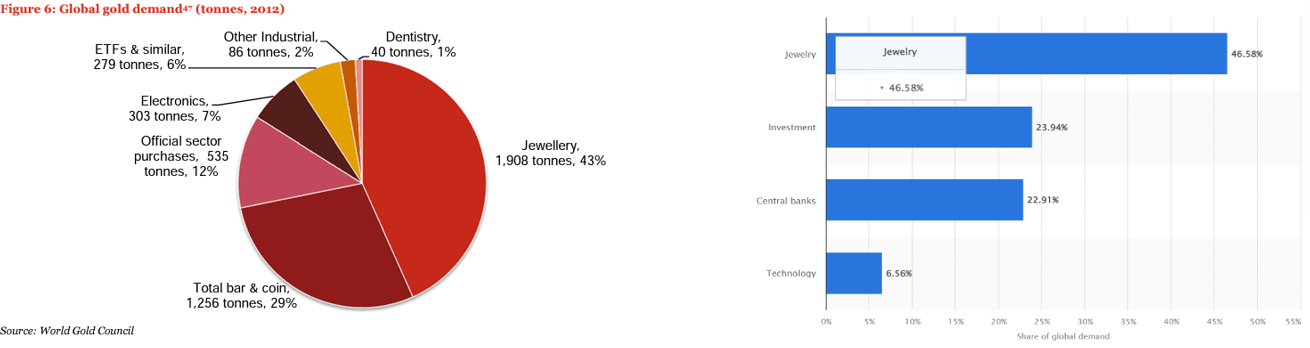

Most people own some gold, typically in the form of jewellery or components in electrical devices, demonstrating its value as a commodity.

When combined, the jewellery and technology sectors account for more than half of total gold demand – shading out financial applications. That broadly matches the demand picture from ten years ago.

Left image: Gold demand, 2012, PwC/World Gold Council

Right image: Distribution of gold demand worldwide by Sector, 2022, Statista

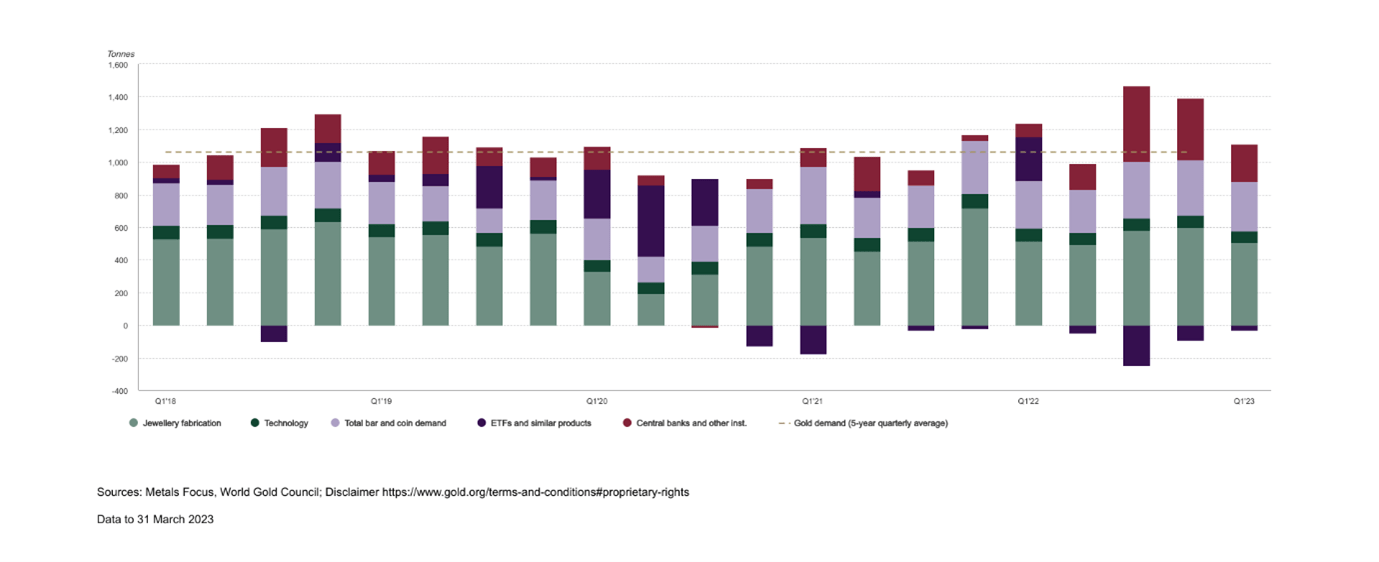

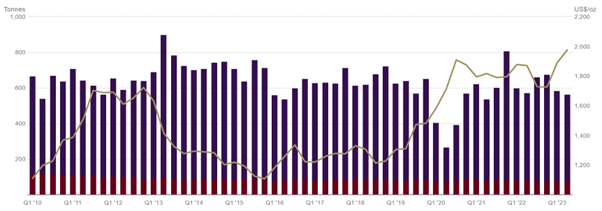

However, the pandemic was a major disruption to gold demand. Jewellery usage plummeted while investment spiked, before reverting to historical levels. The chart below highlights both these changes, and how gold demand has been driven by its use as a commodity over the past five years.

Mixed picture for gold demand in Q1 2023, World Gold Council

Gold supply

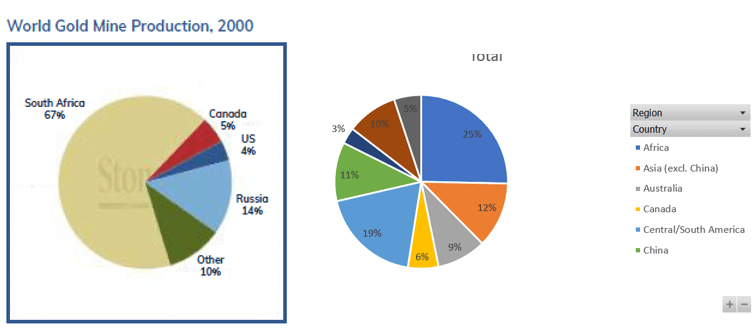

Perhaps the biggest argument for gold as a commodity comes from its supply. Like any other metal, the world’s gold production is mainly dependent on mining.

As with the demand side, mining supply for gold has remained steady in the short term – hovering around 3,500-3,700 tonnes for the last five years. Looking over a longer period, gold supply has grown on average by 2.2% a year since the 1970s, and the make-up of global supply has changed considerably.

While South Africa is responsible for a large proportion of gold in global circulation, it has been dwarfed by other countries in terms of new gold produced over the last decade. Today, China is the world’s biggest gold miner, with Russia closely behind. South Africa has fallen to 13th.

Africa remains the biggest gold-supplying region, representing 24% of global share. But South Africa is no longer the continent’s top supplier, beaten by Ghana, Mali, and Burkina Faso.

Gold production by country in 2000 and 2023, World Gold Council

The steady rises in gold production still haven’t been enough to match growing demand, with most of the shortfall made up by recycling. Recycling levels vary much more than for mining, with multiple contributing factors. In 2022, recycling comprised around 25% of total gold supply.

So, is gold a commodity?

Clearly, discounting gold’s status as a commodity would be foolish. However, analysing gold based solely on commodity-based factors is not going to provide a sufficiently comprehensive picture.

Most gold demand may come from gold jewellery and technology, but investment and central banks also make up almost half. This isn’t true for any other major commodity.

Central banks can be a key part of the gold supply chain, particularly when they choose to sell off large parts of their reserves as the Bank of England did between 1999 and 2002. Traders of no other commodity need to take such complexities into account.

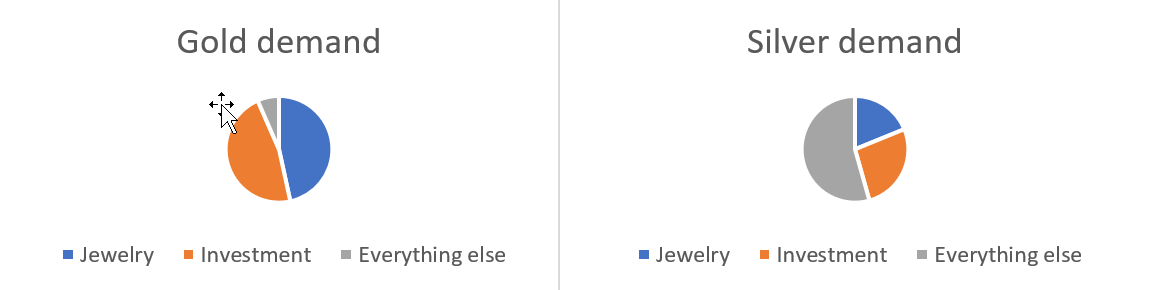

Global silver demand offers an interesting comparison. Often seen as a proxy for gold, investment accounts for a significant portion of demand, but nowhere near the same level as its more illustrious cousin.

Gold and silver demand by sector in 2022, Statista

Gold’s chief use as a commodity – the jewellery industry – further illustrates the point. Much of today’s gold jewellery is ‘price elastic’: high-caratage and bought based on the weight of the contained gold. Jewellers will buy pieces back on a similar basis, reweighing and recalculating the price in front of buyers and sellers.

Thus, price-elastic jewellery – which is common in the Middle East and Asia, hotbeds of gold demand – is a direct form of gold investment.

And as gold jewellery demand plummeted in 2020, gold’s price didn’t follow. Instead, it pushed to all-time highs. If gold is purely a commodity, then a demand gap in its largest industry shouldn’t coincide with a record-breaking rally.

Gold demand vs price, World Gold Council

Another consideration is gold’s historical utility as a currency. Many analysts believe that the relationship died with the abandonment of the gold standard in 1971, but in the present day, geopolitical tensions have led to BRIC nations announcing plans to create a gold-backed alternative reserve currency to the US dollar. Whether or not this comes to fruition remains to be seen, but it acts as a timely reminder that in the centuries-long history of humans and gold, 50 years of fiat currencies is a relative blink of the eye.

Part 2: Gold is an inflation hedge

Gold specialists know that the precious metal is rarely traded purely as a commodity. Instead, a recent StoneX survey of asset managers found that inflation hedging was the chief reason to hold gold, with 67% of respondents stating that they bought gold at least partly to protect against currency erosion. Buying gold as a safe haven was well behind at 44% (respondents were able to choose more than one reason).

Gold’s status as a reliable inflation hedge goes back decades. It has long been viewed as a store of value – much of the jewellery industry is based on the belief that gold items will still be worth the same amount in years to come, even as currency values are gradually eroded by inflation.

Inflation has been used to explain some of gold’s peak periods, too. The precious metal’s remarkable climb from 2008 to 2011, for instance, came as low interest rates and radical new easing initiatives distorted currency values. This forced investors to look outside of traditional fiat investments and towards markets like gold.

See why StoneX is a partner of choice

Gold vs bitcoin

The low-interest-rate environment didn’t end in 2011, though. And in the years since the Global Financial Crisis, 2008-2009, another market has arisen among investors as an alternative to fiat currencies: bitcoin.

Comparisons between bitcoin and gold are numerous – after all, they are both ‘mined’, don’t earn a yield, and sit outside the standard definition of a currency. But does bitcoin, aka “digital gold” share gold’s status as an inflation hedge?

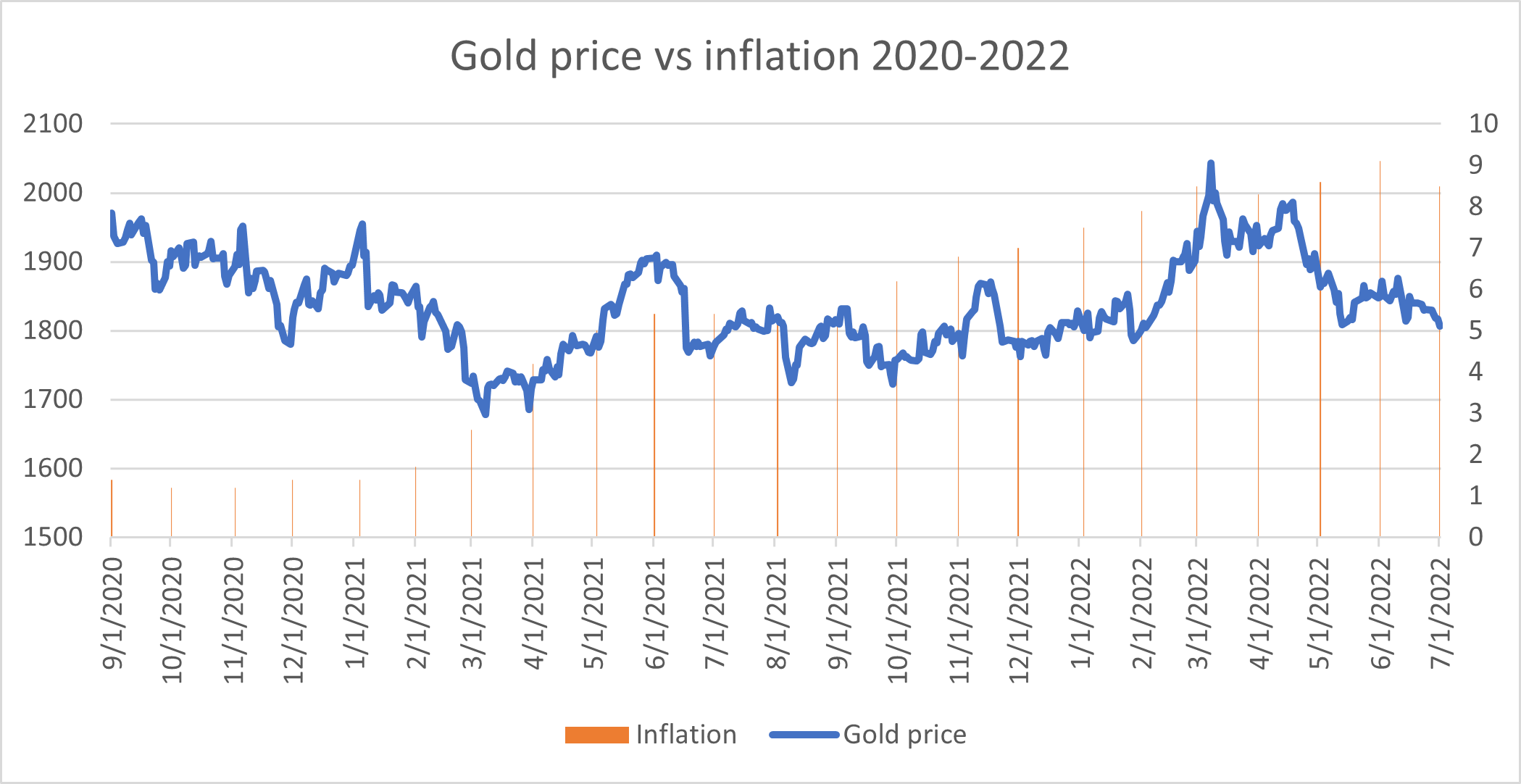

As US inflation spiked from 2020 through to 2022, gold didn’t perform as would be expected from a notorious inflation hedge, remaining flat. In September 2020, when inflation was at 1.4%, gold was worth $1,950. In June 2022, as inflation peaked at 9.1%, gold was worth $1,850.

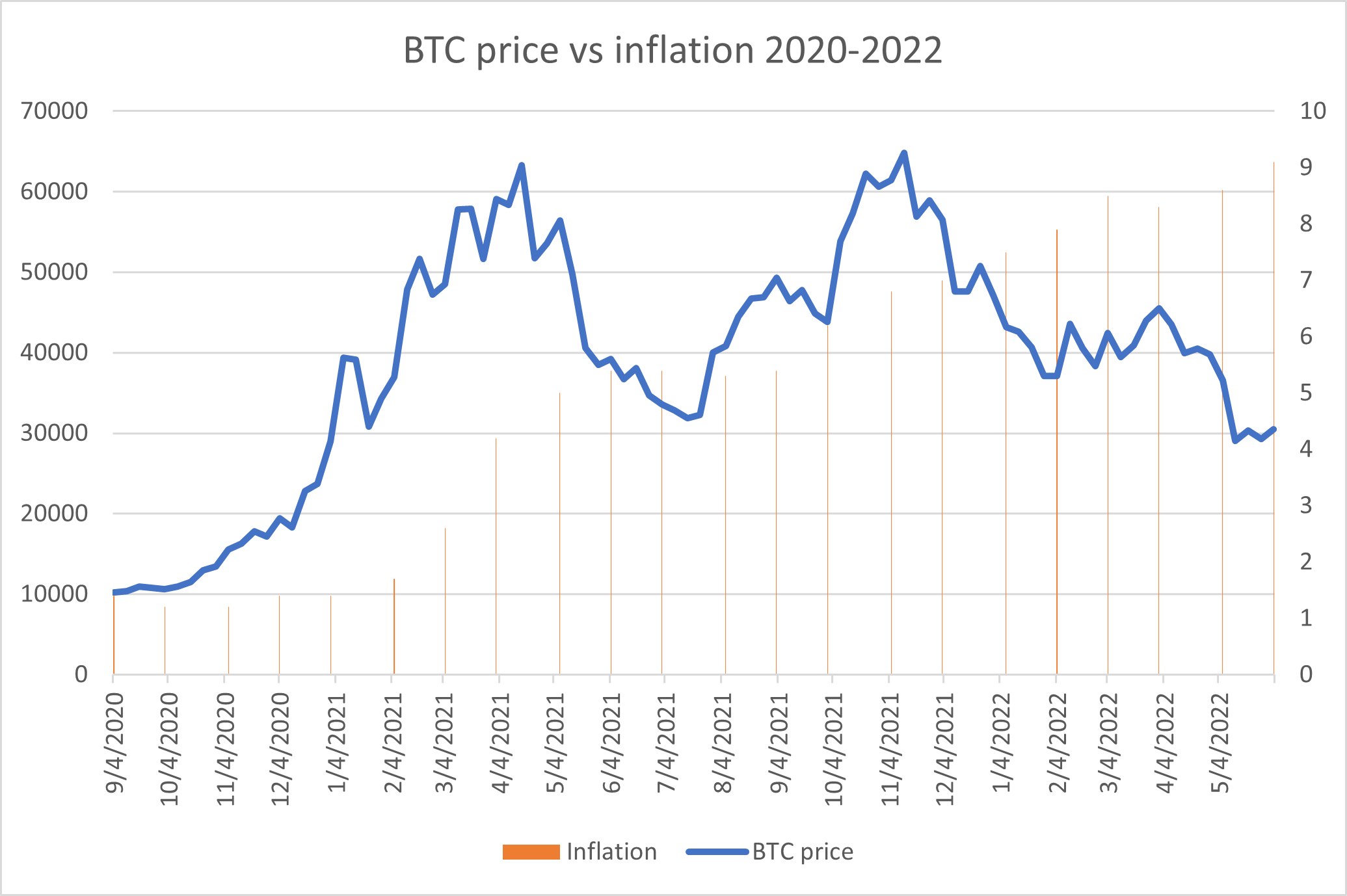

Bitcoin, on the other hand, rallied from $10,230 to $30,467 in the same period, hitting $69,000 at its peak. On recent evidence, the ‘new gold’ is the better hedge against inflation.

However, making such bold proclamations on a single piece of evidence may be premature. And taking a closer look at the bitcoin rally across the period, we can see that the cryptocurrency peaked well before inflation accelerated.

Additionally, bitcoin’s nascency and regulatory uncertainty could distort its reliability as a more ‘traditional’ inflation hedge, leading to periods of speculative existentialism.

Bitcoin’s price vs inflation, 2020-2022, BLS & StoneX data

However, show an outsider the chart below; they’d probably not pick gold as the reliable hedge against inflation. And over a longer period, the evidence doesn’t strengthen. Gold may hold its value over the extremely long term – say, decades or centuries – but that doesn’t necessarily make it a cast-iron inflation hedge for most traders and investors.

Gold price vs inflation, Bloomberg

Gold as a hedge against deflation?

Some even argue that gold’s purchasing power is more likely to increase in deflationary periods than inflationary ones. There has only been one period in recent US history in which the CPI rate has stayed negative, from March to October 2009 – and that coincided with a gold rally.

If we go further back in history, in each of the four deflationary periods since the 17th century in England, gold has increased its purchasing power by between 42% (1658-1669) and 251% (1920-1933). In the United States, there have been three recorded deflationary periods, and gold increased its purchasing power in each of them — by between 44% (1929-1933) and 100% (1814-1830).

So, is gold an inflation hedge?

Though there is significant historical data to work with, there are few prominent data points to base a hypothesis on. It may be premature to declare gold invalid as an inflation hedge due to its capacity as a deflation hedge.

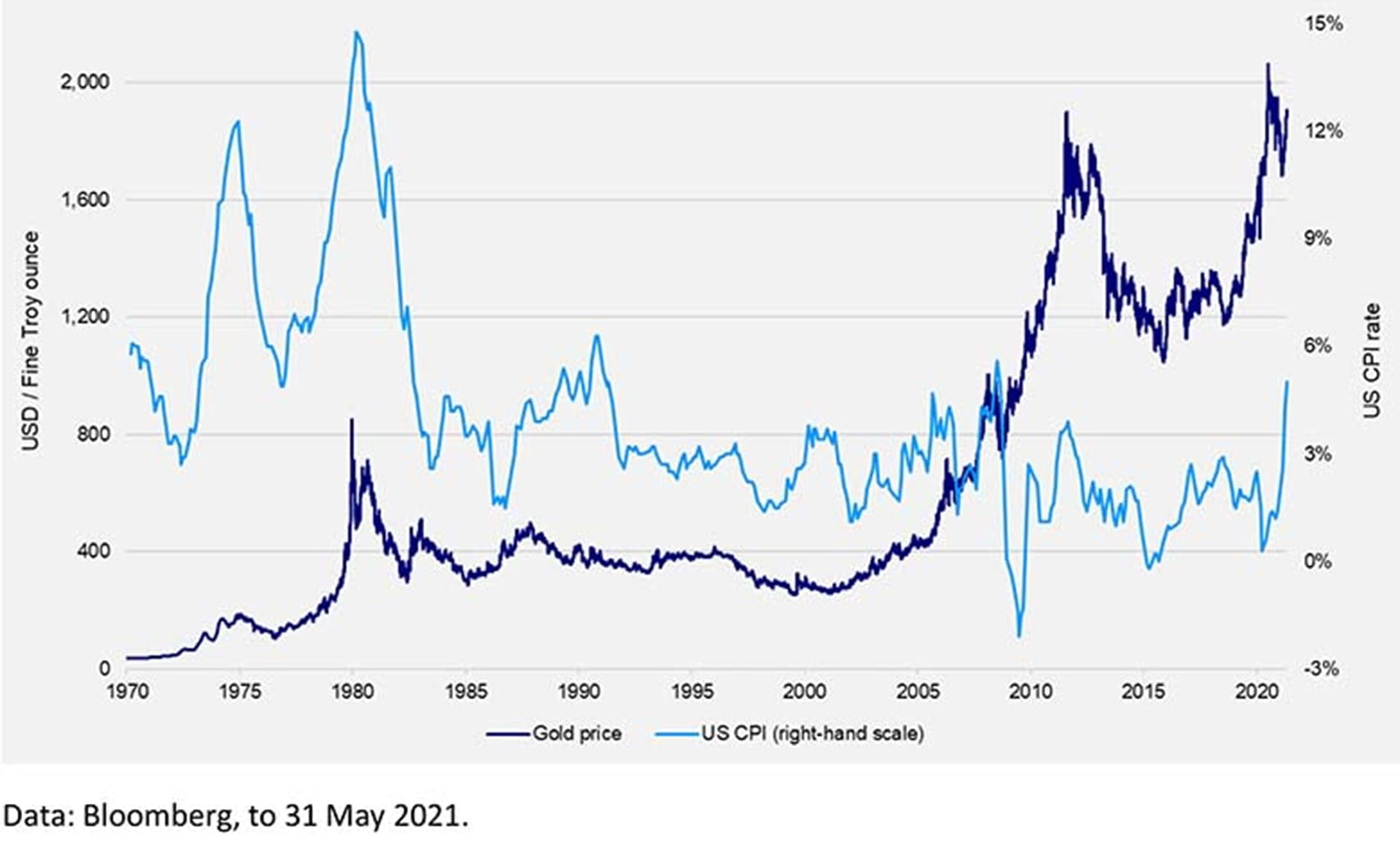

And at least over the long term, gold appears to perform better in inflationary environments. Research by the World Gold Council based upon data going back to 1971 found that in periods when US inflation was above 3% gold tended to rise 15% in the year — whereas when inflation was below 3%, it rose just 6%.

However, in recent years the relationship appears to have broken down somewhat. And while gold may still hold up as a long-term inflation hedge, over shorter periods – such as from 2020-2022 – it can struggle.

In truth, gold performance shows a much stronger relationship to real interest rates than inflation. This makes sense when considering that gold doesn’t return a yield, so when interest rates are low it can make for a much more compelling investment. In 2022, the seemingly never-ending period of low interest rates suddenly and dramatically came to an end. For the first time in multiple years, safe, cash-flow-producing assets were available again – which may explain gold’s failure to push on to new highs.

Part 3: Gold is a safe haven

Perhaps, then, gold is first and foremost a hedge against financial contagion: a safe haven. This was the second most popular reason given in our asset manager survey, and a recent World Gold Council survey of central banks found that protection against financial crises had risen rapidly to become the third most popular reason to hold gold.

Does mass market risk offer the clearest argument for holding gold in today’s market conditions?

To see why it might, we can take a closer look at one of the sharpest market crises to hit in recent times – the global market selloff instigated by the pandemic.

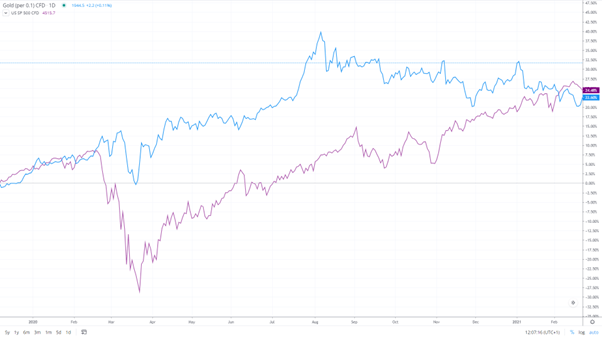

Gold vs the S&P 500, StoneX

Like other markets, gold initially saw a selloff as markets panicked over the fallout from mass lockdowns. While this would seem counterintuitive if it is used as a hedge against freefalling markets elsewhere, it is not unusual – gold is often sold when equities are in distress as it acts as an insurance policy, enabling investors to liquidate their gold positions and cover losses elsewhere.

However, once it has done that job, long positions are typically re-established. And, indeed, as demonstrated in the table below, gold’s fall was the shallowest and its recovery period was the shortest. This also colours gold’s failure to rally significantly as inflation spiked in 2021. Due to the Covid -19 pandemic, it was already close to its record high.

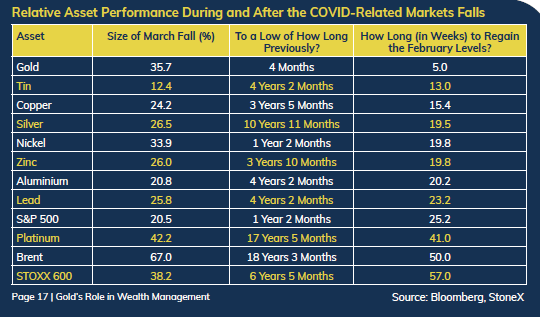

Asset performance over COVID falls, Bloomberg & StoneX

In our survey, among the respondents who had liquidated gold under duress, twice as many rebuilt positions as soon as feasible compared with those who preferred to wait for a strategic entry point.

See why StoneX is a partner of choice

Why is gold considered a safe haven?

Gold doesn’t necessarily seem like an obvious safe haven at first. It generates no yield, has fewer industrial uses compared to other assets and doesn’t guarantee a return. But, as we’ve seen, both asset managers and central banks see the precious metal as crucial to their risk management plans.

Many financial institutions even label gold as a ‘risk-free’ holding alongside cash and treasuries.

We’ve already covered much of why. Gold is highly liquid, with $180 billion of the metal traded daily (including futures and ETPs). It is believed to hold its value whatever the external market conditions and is largely uncorrelated to other major assets – making it an excellent tool for diversification.

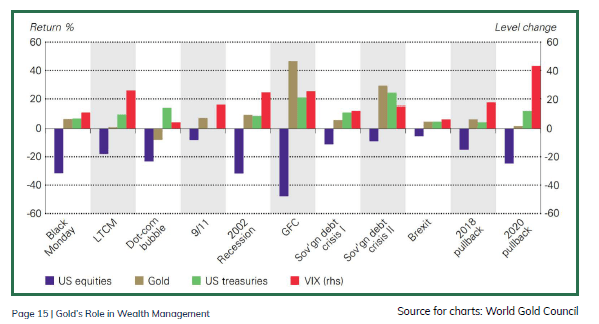

Asset performance over previous market events, World Gold Council

Perhaps most of all, though, gold appears to work as a safe haven. Above are 11 instances where the VIX spiked in the past 40 years, with price moves in equities, treasuries and gold measured over the duration of the spike in each case. Gold’s performance was positive in all except two cases. With the exception of the LTCM crisis, when there was a big flight to treasuries, it was the outperformer.

Safe havens in 2023

What about today? Gold’s safe-haven status can go a long way to explaining why the precious metal sits close to its all-time high in 2023, despite falling inflationary pressures and central bank policy generally still favouring high interest rates.

After all, there is much cause for market concern in 2023 – take your pick from lingering zombie banking concerns, political volatility, Russia’s continued war in Ukraine and natural disasters.

In the 1990s, the Bank of England’s Head of FX and Treasury summed up his attitude to buying gold as ‘First, the war chest argument – that gold is the ultimate store of value in an uncertain world’. Taking in the headlines in 30 years on, it doesn’t appear that much has changed.

How to buy gold

Gold’s elusive nature may, in truth, be the best reason to hold it. How many other assets can fulfil so many roles at once? As we’ve covered, you can utilize gold as a commodity, inflation hedge or safe haven – not to mention as a dollar hedge or diversification play.

The modern bullion market is broad and diverse – comprising multiple exchanges, products, and liquidity centres globally. At StoneX, we focus on providing clients with full access to both the financial and physical markets. Whether you want to hedge your physical position, take a directional view, or invest in physical metal, we can offer you easy access via our trading platforms and comprehensive network of physical supply chains.

Our experienced team offers trading services to the full spectrum of market participants, including, but not limited to, mining companies, wholesale traders, refineries, financial institutions, jewellery manufacturers and wealth managers. As a global operation, we ensure our clients get full coverage and universal access to the related financial markets through our offices in London, Singapore, Europe, Shanghai, Dubai, and the United States.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism. SAP is an “Approved International Trading Company” authorized to act as a “Spot Commodity Broker” under the Commodity Trading Act.

See why StoneX is a partner of choice